A deep look at Floor and Decor's moat and market.

A deep look at Floor and Decor's moat and market.

I’ve written about FND 0.00%↑ Floor and Decor before and it’s easily one of my favorite companies. I only own a small position but I’d like to scale it up at the right price.

Even though I’ve been a regular shopper at Floor and Decor for years, I had no idea that it was a public company until I saw that Buffet (or Todd Combs) had taken a position at Berkshire. Then it dawned on me, Floor and Decor immediately captured marketshare as soon as they opened up a location in my city. Contractors immediately made it a regular part of their operations.When you notice this kind of consumer behavior its important to pay attention because a great investment could be right under your nose.

In this letter I don’t want to give an overview of the business but rather I want to examine their competitors and their moat. But before we do that I want to go over some of the basics.

Market analysis

I want to start with some market analysis of the construction industry as a whole and then move into the flooring market in the United States. This will really give us an idea of how niche the hard surface flooring market is.

The Construction market

The US Construction market is about 2.1 trillion and expected to grow at roughly 4% annually until 2027. This is a massive market, which explains why there’s so much competition and fragmentation.

Aside from specialty construction and raw land development, generally a project will fit into 1 of 5 categories. Below is a break down of each individual category and its size.

Residential: roughly $879.9 billion. Expected to grow at 4.5%

Commercial: (retail stores, hotels, office buildings, and shopping centers) Roughly $251 billion. expected to grow at 3.5%

Civil: (highways, street, sewers) Market is only about $405 billion.

Industrial: (factories, processing facilities) Market size is roughly $198 billion.

Institutional: (hospitals, government buildings, schools) Roughly $176 billion

The only categories that are relevant to Floor and Decor are residential, commercial and institutional, and combined they are about $1.3 trillion.

Flooring market

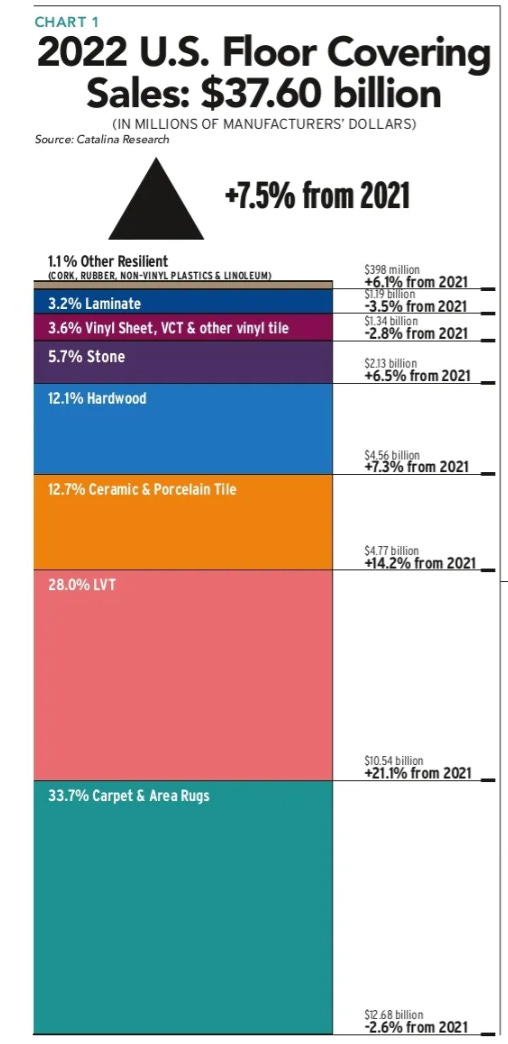

The size of the US flooring market is much smaller and depending on where you get your data, you’ll likely see estimates anywhere between $15-$70 billion. So this is a very small vertical market within the total construction market (2-3%), and I’ll explain later why I think this is an advantage for Floor and Decor.

Floor and Decors sells hard surface flooring products such as wood, stone, tiles, laminate, and vinyl flooring, as well as wall tile products. They also have another category called adjacent categories.

They estimate the hard surface flooring market alone to be $25 billion, but this is according to manufacturing dollars, which is before retail markup. I looked at a few different sources and found that most of them seem to confirm these estimates fairly accurately. According to Floor coverings weekly, which is a notable source for flooring data, the flooring market in 2022 (in manufacturing dollars) is $37.6 billion. They sourced their information from Catalina research, which is where many flooring companies, including Floor and Decor, get their TAM estimates from.

Floor and Decor doesn’t sell carpet and rugs (soft surface flooring) so if we remove them we get about $24.92 billion (in manufacturing dollars), which is basically what they estimated in their annual report.

Keep in mind, soft surface flooring is a shrinking market (-2.6%) and everything else that Floor and Decor sells is growing, which means Floor and Decor is actually digging into the soft surface market, so if we really wanted to we probably could keep soft surface flooring in our TAM calculation. But for the sake of simplicity and conservatism im going to stick with hard surface.

Ok so they’ve concluded that $31 billion is the appropriate figure after retail markup (19% markup). Below is a further break down of how they calculate this. They’ve also given us a figure for their adjacent categories.

Retail hard surface flooring market: $31 billion + $11 billion for installation materials and tools = $42 billion total.

$16 billion is their commercial opportunity

$26 billion is their residential remodel and repair opportunity

Adjacent categories: $8-13 billion

Combined, the total addressable market is $50-55 billion, not bad.

Floor and Decor estimates that they make up for 10% of the the hard surface flooring market, which is up from 8% a few years ago. LL flooring estimates that no single retail store makes up more than 15% or the market. This implies that Floor and Decor is one of the top retailers already and growing its share.

Market and share growth

Thinking about future growth for Floor and Decor we can only assume its going to come from one of the following

Market growth

Taking market share

Pricing power

Since Floor and Decor aims to be a low cost provider I think its safe to say that pricing power wont play a big role in future revenue growth.

Market growth and share taking

The flooring market will likely grow in line with total construction growth (3-5%) between 2022-2027. However, I would expect Floor and Decor will be taking a larger and larger share of that market as it grows. There’s somewhere between 15-20k flooring shops in the US, including small and big retailers, and Floor and Decor has been taking marketshare from all of them.

It’s hard to quantify how much they’re taking from small independent shops, however below is some data from marketwise that clearly implies that they’re winning over the bigger retailers. Floor and Decor’s share has doubled between 2018 and 2022 while almost every one else’s has declined.

This brings us to the reason why Floor and Decor is winning. As I’ve shared before in my write up on FND 0.00%↑

Why Floor and Decor wins

1. Low cost provider

The first reason Floor and Decor wins is because they’re able to price their products competitively because they have a direct sourcing model.

To get a better understanding of this, I want to do a few comparisons. Comparing prices between flooring products can be difficult considering the many different kinds and specifications. Floor and Decor isn’t always the lowest price on every single item, but if we compare products between Home Depot and Floor and Decor, we can see some differences begin to emerge fairly quickly. I chose Home Depot because they are probably Floor and Decor’s biggest rival because they have so many locations but they don’t source their flooring directly.

LVP (luxury vinyl plank) is one the most common product these days, it’s inexpensive, waterproof, very durable and has the look and feel of a luxury wood floor. It’s been in very high demand over the last few years.

Lifeproof is Home Depot’s in-house brand of LVP flooring and it can be compared to Floor and Decors Duralux and NucCore brands, which they sell exclusively.

Before we get started here are a few terms to know

Underlayment: A thin 1/8 inch layer that goes underneath flooring. Most new flooring comes with at least 1 layer of it attached to the back of the plank. Foam is the standard material used for this but a thin layer of cork is also often used and has been shown to be a better product with better durability, acoustics and insulation characteristics.

MIL rating: This is the thickness of the wear layer on top of the plank that gives the flooring durability and resistance to impact and scratches. This number ranges anywhere from 6 to 22 on most products and the higher number is better.

Im going to be shopping as if I’m on a budget trying to find the best floor for the price cheapest price.

Home Depot’s Lifeproof

Specifications

Price: $2.37 sq. ft.

MIL: 12

Underlayment: Foam

Price for 2000 sq. ft. home: $4,740

This is a decent product but certainly on the low end of flooring products. It has a thin layer of foam underlayment and the wear layer is only 12 MIL, which ultimately means it could be more prone to chipping and cracking under heavy loads and impacts. It could also scratch easier.

FND Duralux

Price: $1.49 sq. ft.

MIL rating: 12

Underlayment: foam

Price for 2,000 sq ft home: $2,980

Duralux is FND’s equivalent low quality product. It has the same characteristics and durability as the Home Depot’s but its almost 40% less.

FND NuCore

specifications

Price: $1.89

Wear rating: 22 MIL

Underlayment: Cork back

Price for 2,000 sq. ft. home: $3,960

NuCore is the next level up in quality from Floor and Decor. This is the cheapest NuCore product I could find for $1.98 and it’s the same waterproof product except with a 22 MIL wear layer (twice as much durability) and a cork back underlayment, all at 16% less that Lifeproof.

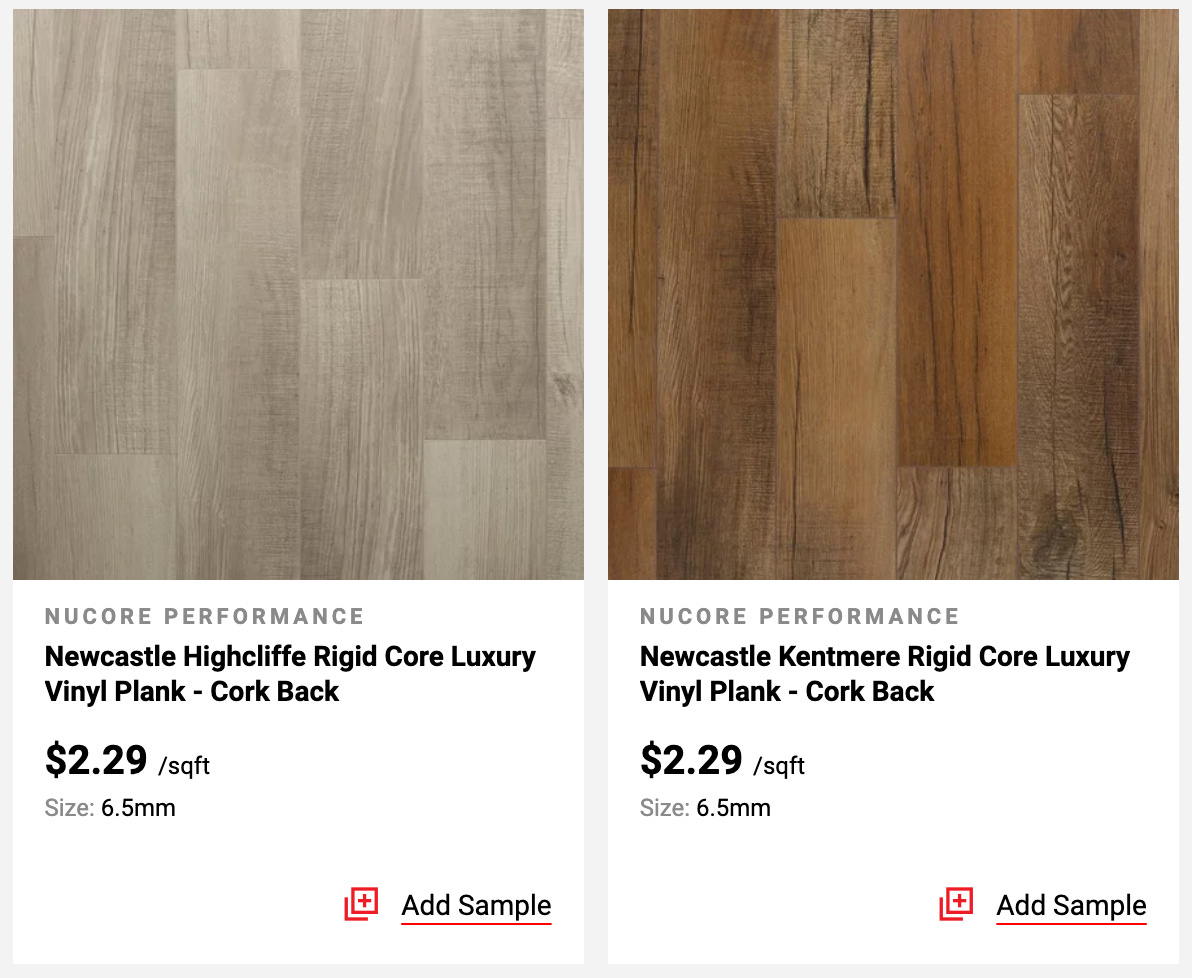

NuCore Performance

Specifications

Price: $2.29 sq. ft.

Wear rating: Techtanium Plus

Underlayment: Cork back

Price for 2,000 sq. ft. home: $4,580

NuCore performance is basically NuCore with an enhanced wear layer called Techtanium Plus which gives it extreme scratch, stain and impact resistance. Most NuCore performance products were over $3 but they had a handful that were $2.29 which is still less than Lifeproof. This is a smokin deal compared to Lifeproof.

Comparison conclusion

Now, some of these comparison may not be fair because people have different color preferences which will affect prices sometimes. Regardless, I browsed their product selections as if I was a typical customer on a tight budget looking for the best quality LVP for the price. You can get way better flooring for just around the same price, maybe a bit less than Home Depot.

2. Selection gravity

why contractors go to FND

The second reason that Floor and Decor is able to win over customers is because they carry almost every item one could possibly need in that specific niche, which creates a gravitational pull.

For example, suppose a contractor has a flooring shopping list consisting of tile, flooring, and various accessories, and Floor and Decor carries the tile and flooring, but doesn’t carry their favorite accessories and installation materials. Most contractors won’t make the trip across town to a mom and pop shop just to get installation materials, especially considering all of their other flooring needs are available at Floor and Decor. They’ll just buy everything at Floor and Decor for convenience.

In reality Floor and Decor has very good products so often times there’s no need to go across town anyways.

Why home owners go to FND

To be a good flooring and tile company you need to offer a very large selection of products because it’s one of the most important decision that people make in the build process. I say this all the time, theres hundreds, if not thousands of products built into a home, and yet flooring and tile are some of the owners biggest concerns because these items, along with cabinets and countertops, are the aspects of your home you’ll be looking at every day for the next 10-30 years. So naturally one would want a place that has the most selection and the best displays to make your decision easier. Floor and Decor provides a very home owner friendly environment with large displays and a very large selection.

Vertical market advantage

Vertical market retailers are niche and focus on a specific customer. AutoZone is probably a great example of this, they focus on one single customer, people who are trying to repair vehicles. Horizontal markets retailer are very broad and attempt to serve everyone. Amazon is the perfect example of this, their motto is “the everything store” and they literally try to serve everyone.

Floor and Decor operates in a vertical niche market. This affords them the privilege of only carrying 4,400 products and the ability to maintain a complex direct sourcing model that allows them to source much products much cheaper. This would be almost impossible for a company like Home Depot that carries 40,000 different products. Costco is the classic example of a company that has successfully implemented a direct sourcing model, they carry only 4,000 products and they’re able to carefully control their costs and pass those savings on to customers.

Since Floor and Decor is able to source flooring at lower prices than Low’s or Home Depot, it translates to either higher profit margins or lower customer prices. regardless, even if they decide to pass those savings on to customers, they still have a cost advantage in marketing campaigns because they’re only targeting a specific niche customer, rather than every kind of tradesman like Home Depot or Lowe’s which are broad markets. This means they have a lower customer acquisition cost.

Also, because Floor and Decor is able to remain focused on staying one step ahead of flooring trends they can continuously offer the most relevant product selection in each geographic area. Again, this creates a gravitational pull as customers know they can get the best selection and the lowest price, along with accessories, all in one place. They’re also able to focus on offering specialty services that other retailers won’t see as practical, such as design services and so forth. So yes, they may only be addressing a tiny portion of the overall construction market but they have some big advantages in doing so.

Potential customer base and demand

Trying to quantify the total customer base is difficult because its made up of designers, flooring contractors, general contractors, and DIY’ers. It’s fairly easy to figure out how many contractors home owners and contractors there are in general. Below is a break down.

Flooring contractors in the US: roughly 120,000 according to us labor statistics.

Construction managers including general contractors: about 500,000

Actual homes in the us: 144 million with an average age of 40 years old.

Since the average age of housing stock in the US is so old renovations are going to need to be done, which translates to more flooring demand. This, along with a housing shortage should provide steady demand for building products in general in the years to come.

Notes on Pro customers

Of all the above information I’m most concerned with the professional customers, who make up about 40% of Floor and Decors revenue. These are very high ticket customers and Floor and Decor seems to be growing a loyal base of them at a decent rate.

Competitors

If we examine some of Floor andDecors biggest competitors it only strengthens the FND 0.00%↑ bull thesis.

LL Flooring (formerly Lumber Liquidators) LL 0.00%↑

Market cap: $95 million

Store count: 450

Revenue $1.2 billion

Book value per share: 8$

Share price: $3.11

Yes, you saw that correctly, the company generated $1.2 billion in revenue, has a book value around $8 and only trades for $3 with a market cap of $95 million. Now, before you go sniffing around for a net net let me go over a few serious concerns with this company.

LL Flooring, formerly Lumber liquidators, is a flooring company that sells wood and various artificial wood flooring products. They have 450 small stores with an average store size of around 6,500-7,500 square feet which is a tenth of the size of the average Floor and Decor location. This inevitably means that they wont stock as many products in store. They technically sell some products that are cheaper than Floor and Decor but many of them are of questionable quality. I personally have never once thought about using LL as a contractor.

They have 400 + products, but they only have 10-20% of them in stock, and the rest have to be ordered. They also don’t have stone tiles, stone products or any of the adjacent categories or bathroom accessories, nor do they have a large selection of tools and installation materials like Floor and Decor.

They don’t provide a great experience for the customer because they don’t have large displays for their products like Floor and Decor. All in all they aren’t really a one stop shop for hard surface flooring needs.

They’ve been losing market share in recent years they’ve also been involved in some wild controversies.

In 2015 they were charged with environmental crimes and agreed to pay $13 million after they were found to be selling illegally logged wood that was sourced from a Russian timber company “Beryozoviy,” who appeared to be potentially involved in some sort of criminal network in far East Russia.

Here is an excerpt from the Department of Justice press release.

“Lumber Liquidators’ race to profit resulted in the plundering of forests and wildlife habitat that, if continued, could spell the end of the Siberian tiger,” said Assistant Attorney General John C. Cruden for the Justice Department’s Environment and Natural Resources Division. “Lumber Liquidators knew it had a duty to follow the law, and instead it flouted the letter and spirit of the Lacey Act, ignoring its own red flags that its products likely came from illegally harvested timber, all at the expense of law abiding competitor”

Not long after this incident they became involved in another scandal involving formaldehyde.

It all started in 2015 when an episode of 60 minutes was aired exposing Lumber Liquidators for importing Chinese made laminate flooring that was preserved in formaldehyde. They subsequently denied these allegations and assured investors this wasn’t true.

Then in 2019 they were charged by the SEC and agreed to pay $36 million in a lawsuit alleging that Lumber liquidators intentionally defrauded investors after making false claims,

“denying the allegations featured in a March 2015 episode of 60 Minutes, and affirming that the company complied with California Air Resources Board (CARB) regulations.”

The company’s gross margins, and most margins for that matter, have been under pressure from high material and transportations costs, and more recently higher antidumping duty rates ($10.6 million) and $1.6 million in product detentions from The Uyghur Forced Labor Production Act, which is essentially and act passed in 2021 that aims to confiscate certain products, in this case PVC products, that are suspected to come from China’sXinjiang region where there is forced labor.

To top it all off their EPS have been decreasing for two years in a row, and their revenue has been stagnant in one of the best construction markets in many years. You didn’t have to be special to make money in construction the last few years, you just had to be alive and in business, but somehow they managed to only grow revenue 5% when everyone else was enjoying the remodeling boom.

They’ve been increasing capex spending since 2017 and trying to rebrand the company but its probably not going to save the company in the long term.

In my opinion LL’s days are numbered, they can’t compete with Floor and Decor unless they expand their store count significantly and change to a larger floor model but even then, their reputation is tarnished severely.

LL 0.00%↑ may prove to be an ok merger arbitrage investment if they were to be acquired at $5-$8 per share, but in no way would I consider investing in this company for the long term.

The Tile Shop

Market cap: $280 million

Share price: $6.30

Revenue: $397

The Tile Shop is a small tile retailer with only 142 locations that average only 20,000 square feet, which is bigger than LL flooring but very small compared to almost 79,000 at the average Floor and Decor store. They sell many types of tile products but many products aren’t in stock and sell cost a lot more than Floor and Decor.

If you browse both websites you can find identical tiles that are priced much differently. For example, below is a popular porcelain ceramic 10 inch hexagon tile. Its available at the tile shop for $9.19 per sq. ft

Here is the same tile at floor and decor for $3.19 per sq ft.

I found various other example with the same outcome. Floor and Decor is able to win on price without sacrificing much quality.

Controversies

This company has also been involved in some controversies. In 2014 they were accused of various accounting missteps and financial misrepresentations along with various reports showing that their products had led contaminations.

"dangerous lead contaminations, up to 13,900 percent greater than the U.S. Consumer Product Safety Commission limits for products that come in contact with children."

There was also class action lawsuit stemming from a report from Gotham research that showed they had overstated their earnings by over 200% and that their largest Chinese supplier was secretly owned by the CEO’s brother in law. The company affirmed that their largest supplier was owned by the CEO’s brother in law, an employee at the time, but they denied the financial allegations.

Prior to these revelations the company did two large public offerings and company insiders dumped over $100 million in stock while the companies shares were trading higher. The company has since continued to destroy shareholder value as the stock has declined. They were also sued by a shareholder in 2019 who accused the CEO of tanking the shares so that he could gain control of the company again.

Ok, so in summary, just like lumber liquidators, this company seems to have bad management and a lack of competitive drive.

Home Depot and Lowe’s

Floor and Decor undoubtedly competes with these two companies, and by volume they sell more flooring and tile products. Although, Floor and Decor does have a clear advantage with its size, which is key in taking market share away from Home Depot and Lowe’s, which is actually a huge opportunity.

Large home improvement centers only allocate 3,000-5,000 sq. feet of floor space to flooring, carrying roughly 400-600 sku’s, which is still dwarfed by Floor and Decor who carries about 1,500 sku’s in stock.

Home improvement retailers only allocate 2-3 isles at the most to flooring. Theoretically they could begin allocating more floor space to flooring but then they’d be taking away from another category such as electrical or appliances. Remember, Home Depot and Lowe’s have to please everyone in construction, and therefor have to consider the opportunity cost of what they allocate floor space to. Floor and Decor on the other hand only has to please one customer in a specific vertical.

Even if Home Depot and Lowe’s added one or two more isles, it wouldn’t even come close to the experience you get when you go to Floor and Decor.

Independent shops (mom and pop)

Theres somewhere around 30k floor covering retailers in the US and about 13k-15k small independent hard surface flooring retailers in the United States. They make up about 33% of Floor and Decor’s addressable market and Floor and Decor shouldn’t have a difficult time taking share from them as they provide a superior customer experience and better prices.

Many of these smaller shops have an advantage because they create personal relationships with contractors, but they struggle to keep things in stock and they’re incapable of competing with Floor and Decor on price. Floor and Decor offers good enough customer service and has everything in stock at a lower price.

Together Home Improvement centers and mom and pop shops make up over 60% of the addressable market, and I think Floor and Decor is positioned nicely to keep taking it away from them.

Moat overview

Brand

Floor and Decor does have a strong brand but I believe this hasn’t quite matured yet. In the same way Home Depot has become known as the one stop shop for home improvement supplies, I believe Floor and Decor will eventually be known as the low cost, one stop shop for flooring and accessories.

They also work with suppliers to create higher margin, in house products (NuCore, Duralux, Optimax) which have some brand recognition for being low priced and durable products.

Scale economics

One of the big advantages of being a large retailer is scale economics. As they buy in larger quantities they’re able to bargain with suppliers for lower prices, while simultaneously spreading marketing and administration costs over a growing base of stores, resulting in a lower costs per unit and a lower customer acquisition cost.

They’ve dumped almost $2 billion dollars into building their footprint of enormous retail locations since 2014. Sure, theoretically someone could come along and do the same thing but it would take billions in capital and many years of building to do it.

Final thoughts

Ok, I know this has been unnecessarily long and exhaustive but this is of the more interesting companies in my portfolio especially since its so early in its growth phase and its such a simple proven business model.

The recent earning report was not very positive at all but this is expected in a high interest rate environment but I expect good things from Floor and Decor over the long term.

Than’s it for this week thanks for reading!