Aimia. Allocator Takeover, Trading Below Book Value. A war-chest of cash ready to deploy

Key information

Ticker: $AIM.TO

Share Price: C$2.75

P/B: 0.75

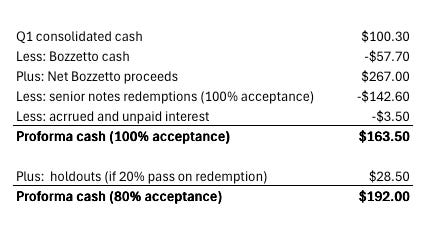

Net cash: (post Bozzetto sale) $163.5m - $192.0m

Brief Overview

Aimia is a Canadian company listed on the Toronto Exchange. Previously an airline rewards business that unraveled and is now converting into a permanent capital vehicle.

Activist Rhys Summerton is leading the transformation and he has a track record (45% CAGR) that should be taken seriously.

Aimia trades at C$2.75, with a pro forma book value per share of $3.66 once the Bozzetto sale closes. Tax losses are also worth an additional $1-2 per share, depending on utilization.

I estimate shares are worth ~$5.25+ (90% + upside) based on book value and NOL’s as of today. This could be higher if more NOL’s are utilized. This gives to credit to its future as an acquisition platform.

At $2.75, you get the cash, an operating company (Cortland) and pay nothing for the tax losses, the capital allocation optionality, or the Summerton premium. You are buying the shell at a discount and waiting for it to become a permanent capital vehicle.

After redeeming up to $142.6m of 2030 notes, pro forma cash is ~$163m-$192m, and can be deployed.

The gap between the share price and the book value is likely to close after Rhys Summerton makes progress on an acquisition.

Aeroplan To Summerton

Aimia shareholders have been kicked in the teeth, as you will see in a minute. I’m guessing most investors exited at a loss and will never return no matter how much progress is made in the future. Herein lies the opportunity; sentiment has seen a complete blowout but a little known activist with a credible track record is finally involved.

Aimia is what’s left of Aeroplan, the Air Canada loyalty program that was spun out in 2005. The great unraveling began in 2017 when Air Canada announced it would not renew its commercial agreement with Aimia and so the stock dropped 65% in a single session. The CEO was on medical leave at the time and his replacement, David Johnston, lasted less than a year.

What followed was basically a fire sale. Nectar, one of Aimia’s UK brands, was sold in 2018 for $105m, along with Air Miles for $159m against the $715m paid. Yikes.

Aeroplan was then sold back to Air Canada in 2019 and what remained was a Canadian holding company with cash and tax losses. In 2020, the Mittleman brothers (Phil and Chris) took operational control and pivoted Aimia from loyalty operator to holding company, which also went horrendously.

The capital destruction under their watch and the subsequent Finke era was disastrous:

Kognitiv (49% stake, initially valued at $525m) wound down in 2025 returning ~$3.3m.

Trade X ($75.6m invested) went into receivership in 2023.

Clear Media, a stake in China’s largest outdoor advertising company, was acquired for $76m and is marked down 84% at $12m today.

The company also spent $28m on shareholder activism, fought off two takeover attempts, and cycled through five CEOs/Executive Chairmen in eight years.

Enter Rhys Summerton

Rhys Summerton began building a position in Aimia in 2023 and is now the executive chairman. Before we move on, I will give a brief introduction to Rhys.

He founded Milkwood Capital in 2014 after running Citi’s global EM equity research desk (top ranked during his tenure). Milkwood is a UK based value and activism shop focused on small and mid caps. Per Hedgeweek 1, the fund has delivered over 500% cumulative returns over five years, and was up 25% through October 2025. Alternatives Watch 2 reported 45% annualized over five years.

However, his returns weren’t always this exceptional. For the first five years, Milkwood employed a passive deep-value strategy, waiting for the market to re-rate their cheap stocks but saw little success. The Milkwood Fund’s net annualized return was sitting right at 8.3%, as it was a time when passive value investing faced macro headwinds globally.

“The first five or six years, we were bashing our heads against the wall. We were buying cheap things, but no one cared. It was a value trap.” - Milkwood’s analyst, André Tonkin

While Milkwood strategy has always included some activist and advisory, the big turning point came in 2018-2019 when Milkwood shifted roughly half its portfolio into highly concentrated activist stakes.

Strategy and Track Record

Summerton’s strategy is essentially private equity for deep value small caps. He looks for deeply discounted businesses with low debt and a pile of cash on the balance sheet. Once a stake is built, Summerton employee a hard-nosed activist strategy by aggressively controlling how capital is deployed. His favorite levers include slashing bloated corporate overhead, selling off underperforming or non-core assets to simplify into a pure-play asset, and pushing boards to deploy heavy cash reserves into aggressive share buybacks.

He’s hit several home runs over the last 8 years. He also had a few failures but they were not operational failures, they were campaign defeats where Milkwood wasn’t able to win the proxy vote.

I’ll go over the wins first.

1. Menzies Aviation

One of Rhys signature deals was Menzies Aviation. Milkwood helped split the aviation business from newspaper distribution, then blocked dilutive capital raises when COVID crashed the stock ~90%. Rhys then brought in co-investors at ~£1 per share, and the business was sold to Agility at 608 pence per share in 2022, a ~500% return over 18 months for Milkwood’s co funders3.

2. Argent Industrial

Argent is another success story. Milkwood’s activist engagements began in 2018-2019. Milkwood pushed aggressively to Argent’s low-return, cyclical, and loss-making South African assets. Capital was recycled away from domestic steel operations and into higher-margin, offshore manufacturing businesses in developed markets. Milkwood also pushed the company to use its excess cash conversion aggressively to buy back shares at a deep discount.

3. IOCO Ltd.

Milkwood Capital became involved with iOCO (then known as EOH Holdings) in May 2024, when he joined the company's board of director. He stepped in directly as Joint Group CEO in 2024 to restructure debt, rebrand the legacy IT firm, and drive profitability. The stock is up 250% + since.

Unsuccessful Activist Campaigns

Nanoco: The board painted Summerton as an opportunistic asset stripper who wanted to liquidate their scientific R&D to fund his own investment vehicle. The narrative worked so the shareholder base panicked and voted 95%+ against him.

Triple Point (TENT): This was a failed attempt to intercept a liquidation. Sharholders’s simply preferred a clean, immediate cash exit via standard liquidation rather than backing Milkwood’s complex platform thesis. They voted 99% against Rhys.

Downing Strategic (DSM): While Rhys successfully blocked a specific share structure, shareholders ultimately rejected his hostile board coup. The reason was because the board offered a simpler alternative, namely, distributing the cash via massive special dividends instead of letting Milkwood manage it.

Enter Aimia

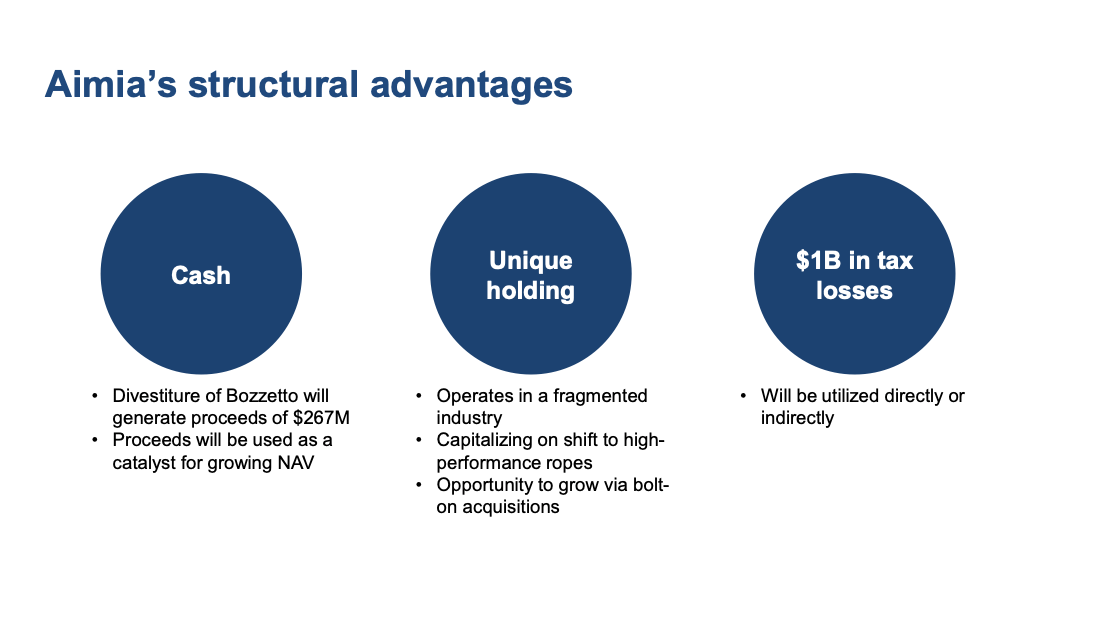

Aimia is converting into a permanent capital vehicle and has a balance sheet that just received ~$267m net from the sale of their specialty chemicals business Giovanni Bozzetto.

Milkwood began buying Aimia in 2022-2023 and won a special shareholder meeting in January 2025. Rhys has been Executive Chairman since March 2025 and Milkwood now owns ~12% (~10.7m shares). Rhys takes zero cash salary and his only return comes from the share price.

Milkwood is also cooperating with Mithaq Capital, a Saudi-based family office run by Turki AlRajhi, and it is an interesting dynamic so far. Mithaq is the largest Aimia shareholder with 30% and has board representation alongside Summerton via Muhammad Asif Seemab (Managing Director of Mithaq). Mithaq and Milkwood have also worked together on other activist campaigns as well.

The new 5 person board collectively owns 42.6% of the stock, which is dominated by two activist appointed board members.

The Plan for Aimia

Their plan is ultimately to increase book value over time through buy back accretion, growing retained earnings from portfolio companies, and utilizing the NOL’s.

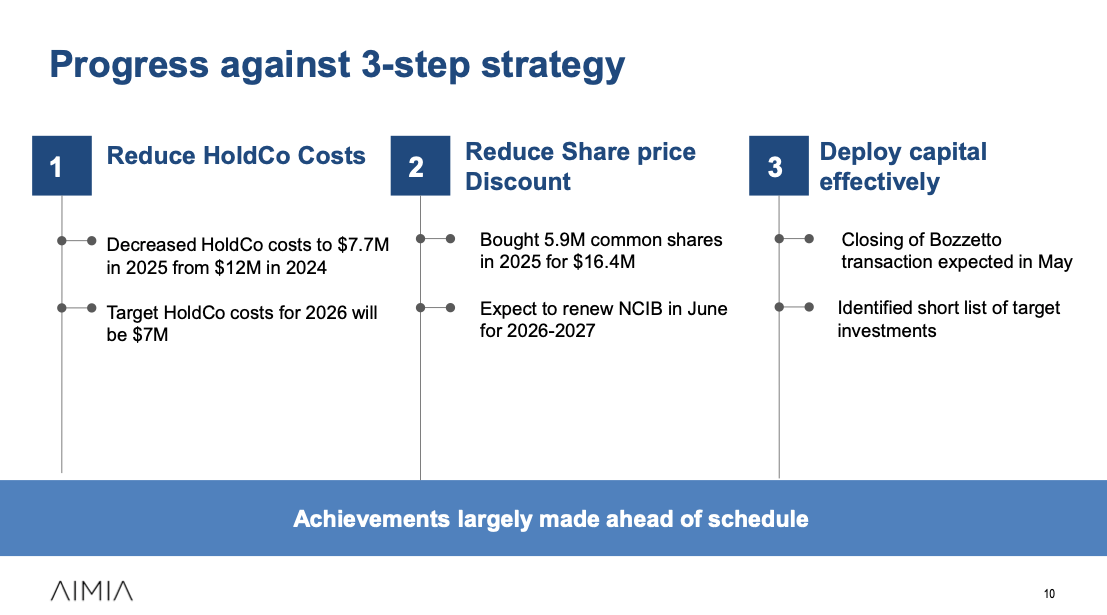

They have laid out a three step plan:

Cut HoldCo costs below 1.5% of NAV (largely done, $12m to $7.7m & now targeting $7m)

Narrow the discount to intrinsic value (buybacks, UK AIM listing, transparency). They have already bought back ~6.7m shares worth ~$18.7m since Summerton has been involved.

Deploy ~$164m to $192m of cash into controlling stakes in undervalued companies, focusing on orphaned UK small caps left behind by the passive investing shift and corporate carve-outs where businesses are trapped in the wrong structure.

Acquisition strategy

Aimia is looking to take controlling positions in companies with strong FCF, net cash balance sheets, and management that thinks long-term. Summerton has identified 50+ companies meeting these criteria.

Cortland (Aimias operating company) is also likely to be used as a bolt-on m&a platform in ropes and netting under new CEO Wolfgang Wandl. It’s a large growing fragmented market.

3 pools of capital

Aimia has three pools of capital for deployment

Post-Bozzetto cash (~$163m to $192m)

Cortland’s own cash generation (expected to upstream more to HoldCo in H2 2026)

Tax losses ($1.1b) used to shelter income from acquired businesses

Post Bozzetto cash

This is the war chest of cash sitting at the HoldCo after the close of the sale of Bozzetto. After redeeming up to $142.6m of their 2030 notes, pro forma cash will land between $163m to $192m depending on noteholder take up. If only 80% accept redemption, cash lands a bit higher at $192m.

Cortland cash

Cortland International is a potentially reliable source of cash. It makes high performance synthetic fiber ropes, slings, netting and tethers, with 6 manufacturing sites across the US and India. End markets span fishing and aquaculture, marine and shipping, offshore energy, aerospace and defense, and industrial safety. It a boring cash generative business in a growing market and does ~$18m in EBITDA.

When Aimia originally set up Cortland, it structured part of the deal as a loan from parent to subsidiary. Cortland pays ~7.5% interest on that loan, which comes to ~$8.8m per year in cash flowing from Cortland up to HoldCo. On top of that, Cortland repays ~$5m per year in principal. So total cash moving upstream is ~$13.8m annually. The cool part is that the ~$8.8m in inter-company interest is not only a deductible expense for Cortland, but it also tax free as the NOL’s are monetized against it.

The problem is that between overhead and preferred dividends, the HoldCo eats that ~$13.8m with nothing to spare. So the new Cortland CEO, Wandl, is tasked with growing free cash flow and growing the Cortland’s footprint, while Summerton and the team reduce HoldCo costs. If Cortland can generate, say, $22m to $25m in adjusted EBITDA (from $19.9m in 2025) through cost discipline and a sales turnaround, and Aimia bolts on a few small acquisitions, Cortland’s upstream to HoldCo could grow from ~$13.8m/year to $18m to $20m/year within 2 to 3 years, and Aimia can start using that surplus of cash for reinvestment or further buybacks.

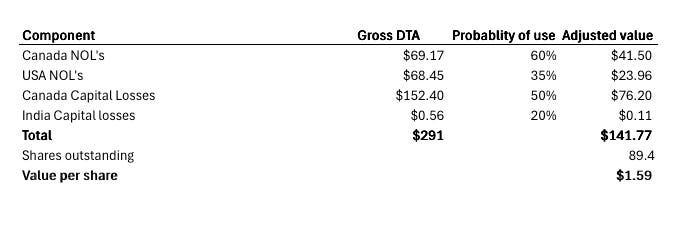

Tax Assets

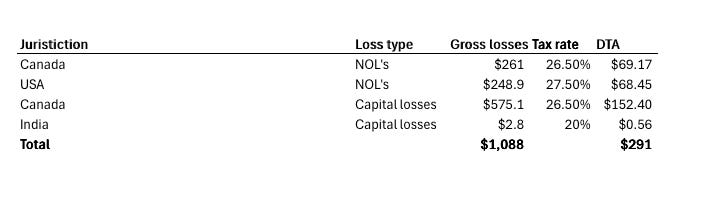

Aimia also has ~$1.1b of tax loss carry forwards, or $291m in tax assets, none of which Aimia carries as a recognized asset on the balance sheet today. The 291 figure is stated directly by management in the presentation.

It is a mixture of NOL’s and capital losses. The former can be used to shelter operating income and the latter can be used to offset capital gains.

I have trouble believing they will be able to actually realize the full value because a good portion ($248m) requires US-source taxable income because that’s where the losses occurred, and Summerton has signaled that the UK as the primary target market. Maybe if they ramp up Cortlands operations in the US they will be able to maximize the US NOL’s, but they have a long ways to go to consume ~$248m.

There is also $575m in Canadian capital losses that can only be used to shelter capital gains or “the repatriation of cash from subsidiaries.” This means Aimia needs future capital dispositions or dividend repatriations to monetize them, which is more lumpy and unpredictable.

So my best estimate is $141m in DTA’s, or $1.58 per share after adjusting for estimated usage. I’m just guessing with the utilization. In reality it could be more or less, and out certainly could be more because management has said that they have “every intention for our acquisition strategy to make use of them, directly and indirectly." Regardless, I’m not giving them full credit for monetizing them at this point.

The more important thing is that for $2.75, you get the cash, Cortland and pay basically nothing for the tax losses, the capital allocation optionality, or the Summerton premium. If a single acquisition closes in a Canadian or US jurisdiction that starts generating sheltered earnings, the DTA’s likely reprice on the balance sheet from zero to something meaningful and actual book value per share grows.

Risks

1. Execution: At this point, the only big risk I see is execution risk. Rhys has a good track record, but it is not a very long track record. It’s understandable that the market isn’t pricing this like he has a multi-decade record of transforming businesses.

Valuation

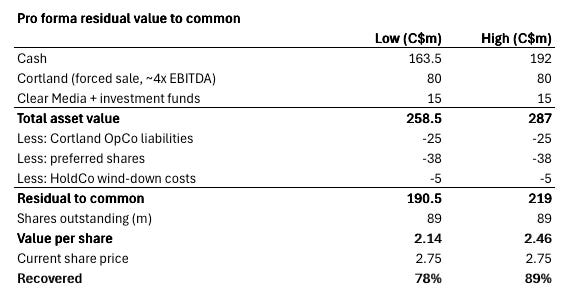

This company is very cheap. If for some reason Aimia were to liquidate today, in my estimate, investors would likely recoup 75-90% of their money.

The OpCo liability and wind down costs are my own estimates and are not derived from the investor materials4.

According to management, book value best represents the true value of the business, but I would suggest that the current value is best represented by both the book value per share of 3.66 plus the $1.59 per share in tax assets which aren’t accounted for on the balance sheet, so the shares are worth ~$5.25 today, implying 90% upside. This doesn’t give any credit to Rhys or the future of the business as a permanent capital vehicle.

Final thoughts

I exited a few speculative and tracking positions and bought some Aimia. I like the set-up because the downside is protected and the upside is not currently priced in. That being said, I would note two things;

The story is almost entirely forward looking and the thesis could take 1-2 years to unfold. Today, the only active channel is the buyback and the modest Cortland cash flow upstream. The core of the bull thesis is the tax shield and acquisition driven compounding, which require execution that hasn't happened yet. So you are buying a shell company with a small operating asset at a discount, hoping management will execute well. This brings me to the second thing to note.

Rhys doesn’t have a long track record. Although he has been investing for along time, his career as an activist, however successful, has not even spanned a full decade yet. Plus, he has never built an acquisition platform like this before.

I say all this to say that I’m moving forward with some caution and you should too.

Disclaimer: All my content is solely for educational purposes only. Nothing I say should be interpreted as financial advice. None of my financial models should be taken as buy or sell signals. Please consult a financial advisor before buying or selling any securities.

Full Disclosure: I do own $AIM.TO shares at the time this was written.

My ~$25m was an approximation, attributing most of the $16.6m AP, the $5.2m leases, and a portion of the $10.8m other non-current liabilities to Cortland. HoldCo wind-down costs of $5m, which is entirely my estimate.