Atkore

A serial acquirer with secular tailwinds

The business

Atkore was founded in 1959 as a small conduit and tube company called Allied Tube & Conduit. They have essentially grown their way through acquisition and organic growth into the company you see today.

Atkore describes itself like this:

“leading manufacturer of Electrical products primarily for the non-residential construction and renovation markets, as well as residential markets, and Safety & Infrastructure products for the construction and industrial markets”

It breaks it segments down into two categories

Electrical

Electrical products include electrical conduits, cables and installation accessories. These products are built into the building systems of commercial buildings, homes and infrastructure. They are found on, in and around virtually all commercial and residential buildings, everywhere from underneath the foundation to the solar system on the roof. These are also found in most data center and renewable energy applications which will likely create demand for the foreseeable future In those areas. They are usually required by the International building code.

Safety and infrastructure

The safety and infrastructure products are more along the lines of mechanical pipe, sign posts and safety bollards in front of commercial buildings and so forth. These products are also required by the International building code.

Both product segments are generally sold to contractors, electrical distribution companies, big box retailers, and electrical supply stores.

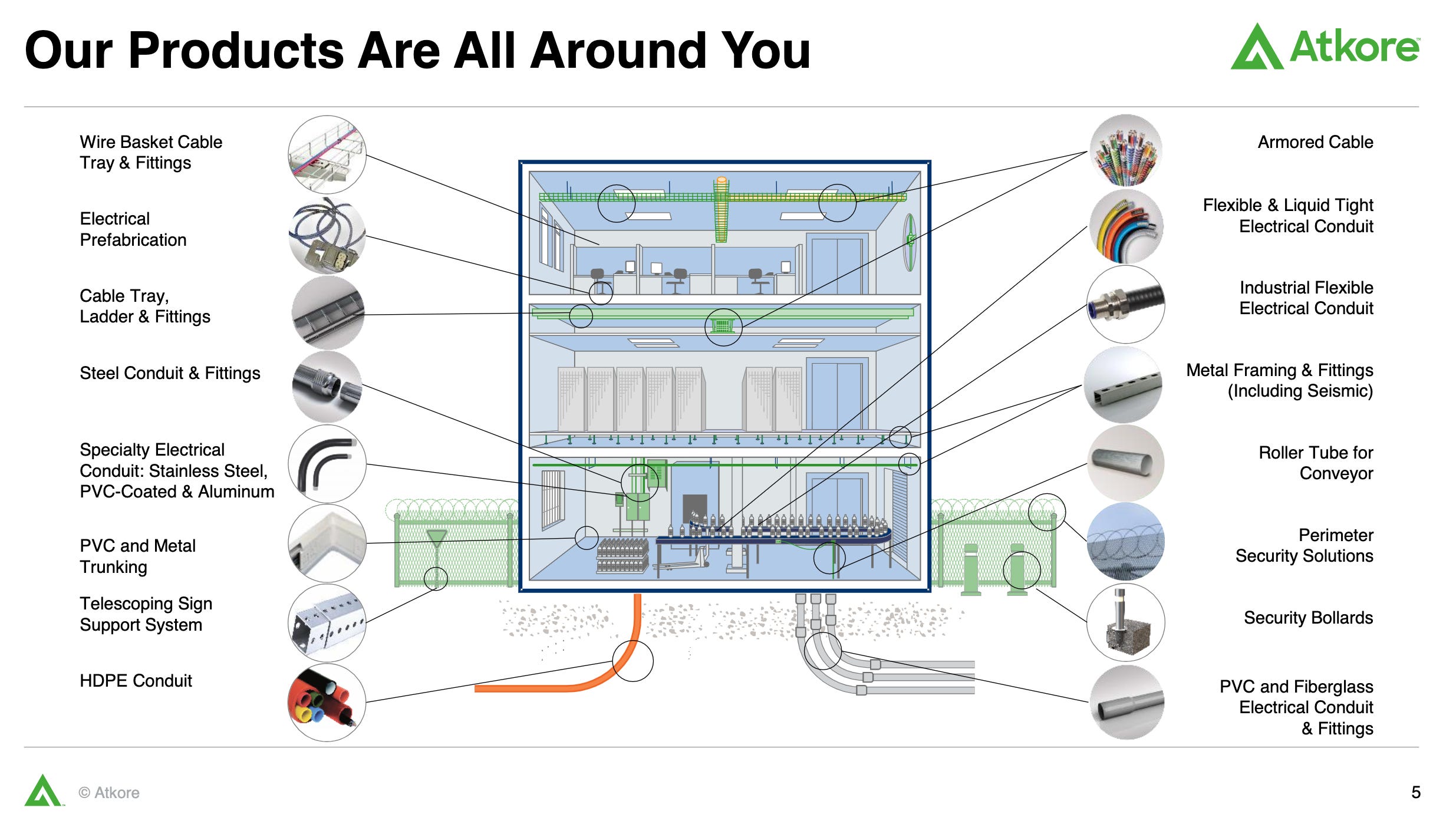

Here’s an info graph of their product selection

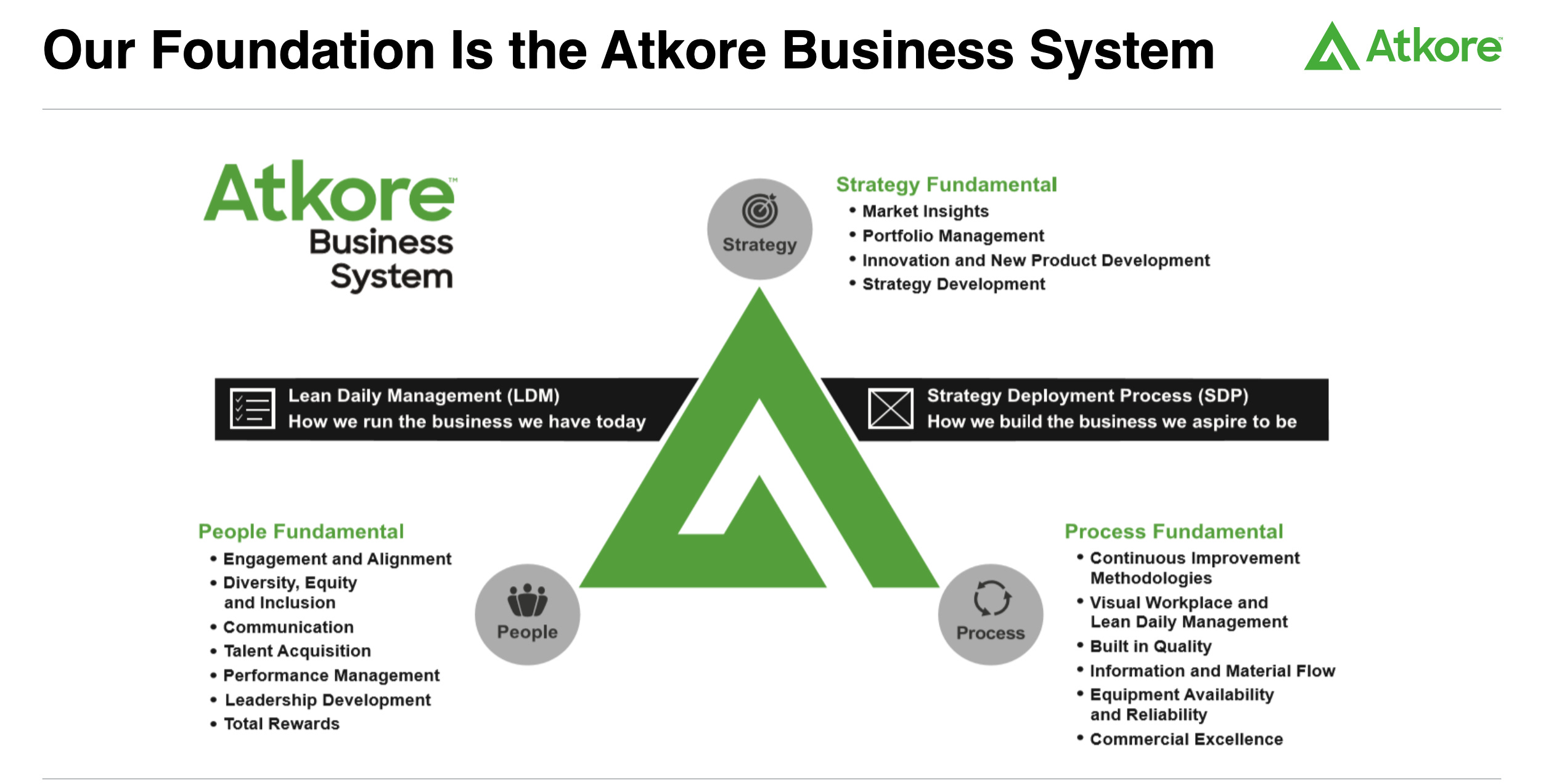

Atkore business system

For the sake of time I’m going to attempt to summarize the Atkore business system which is really just a copy cat of the Danaher business system.

At first glance the the phrase “Atkore business system” or “danaher business system” just seems like another boring fluffy way to present their business in an investor presentation. But in reality the business system is the actual source of Danaher’s success and hopefully Atkore’s as well.

This business systems haas its roots in Japanese lean manufacturing methodologies such as kaizen. They have basically taken these methodologies and created their own 3 part system. The basic idea is to have the entire company at all levels working together to make perpetual, small, incremental improvements. The difference between this method and other manufacturing methods is that there is no end goal, it’s perpetual, as soon as you’ve improved by 5% you’re incentivized to turn around and improve another 5%. There is no goal or finish line.

It’s more of a company philosophy that incentivizes everyone to solve problems, hire the best employees, make improvements, reduce waste and work in an every increasing efficient way. This can be an exhausting work environment with large employee turn over so retaining good talent is also very important.

If Atkore is truly following the path and strategy of Danaher, I would sum up their strategy like this. They are essentially acquiring new businesses and folding them into a unified business system where they are subject to constant incremental improvement.

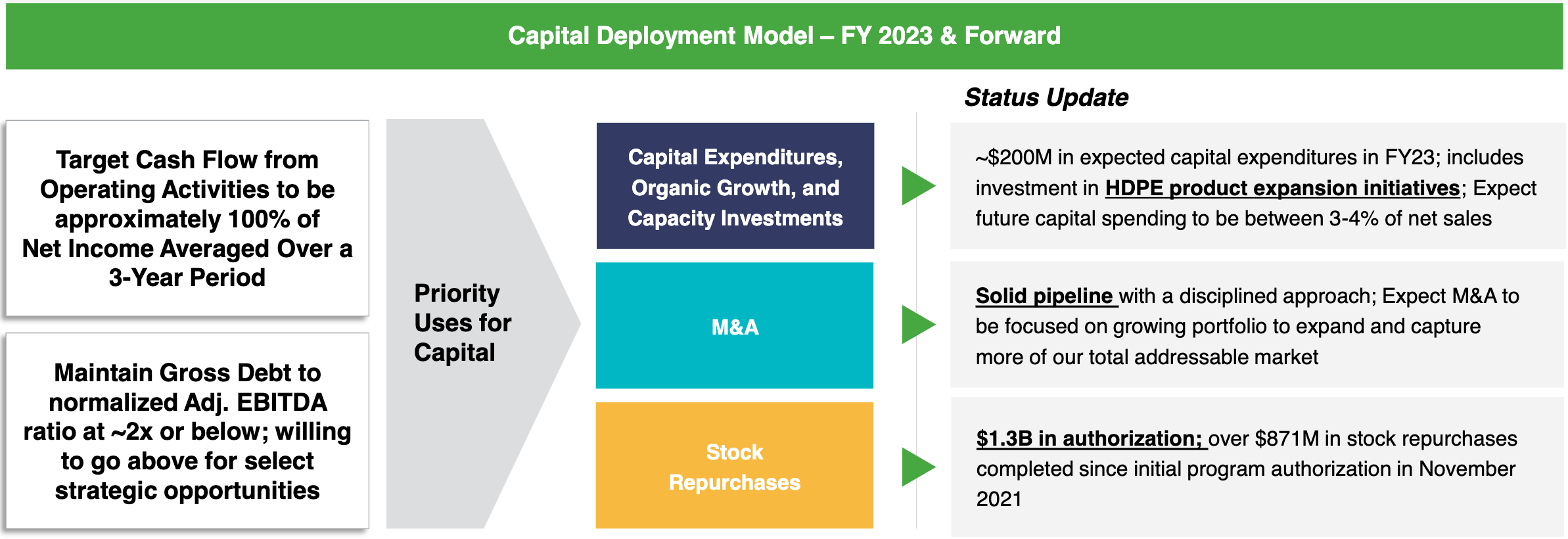

Capital allocation

Below is their capital allocation plans

Im happy to see their priorities in line. The investment in organic growth is largely upgrading machinery and improving manufacturing so they can improve the manufacturing process for the companies they own.

As far as M&A, they essentially do smaller tuck in acquisitions where their subsidiaries absorb the acquired companies into their platform and into the larger Atkore business system. Every now and then they will make and acquisition that will give them a foot into a new market or product category which will expand their total addressable market. They they can begin acquiring smaller companies into those categories. They claim to have doubled their addressable market since they went public.

Atkore operates in an advantageous market for an acquisitive strategy. The electrical supplies market is a large pond with lots of fish which gives them a long runway for potential acquisitions. Especially if they can expand into new product categories and expand their total addressable market.

Financials

This is a company with minimal debt, roughly $760 million against $1.3 billion in equity. Their revenue has grown quite nicely the last few years which they’ve mainly attributed to increased average selling prices. This increase has outpaced operating expenses and resulted in outsized operating income and increased margins. Below you can see their margins between 2016 (left) and 2022 (right)

This is a little worrisome because if the price of raw materials were to drop their sales and earnings would likely follow suit.

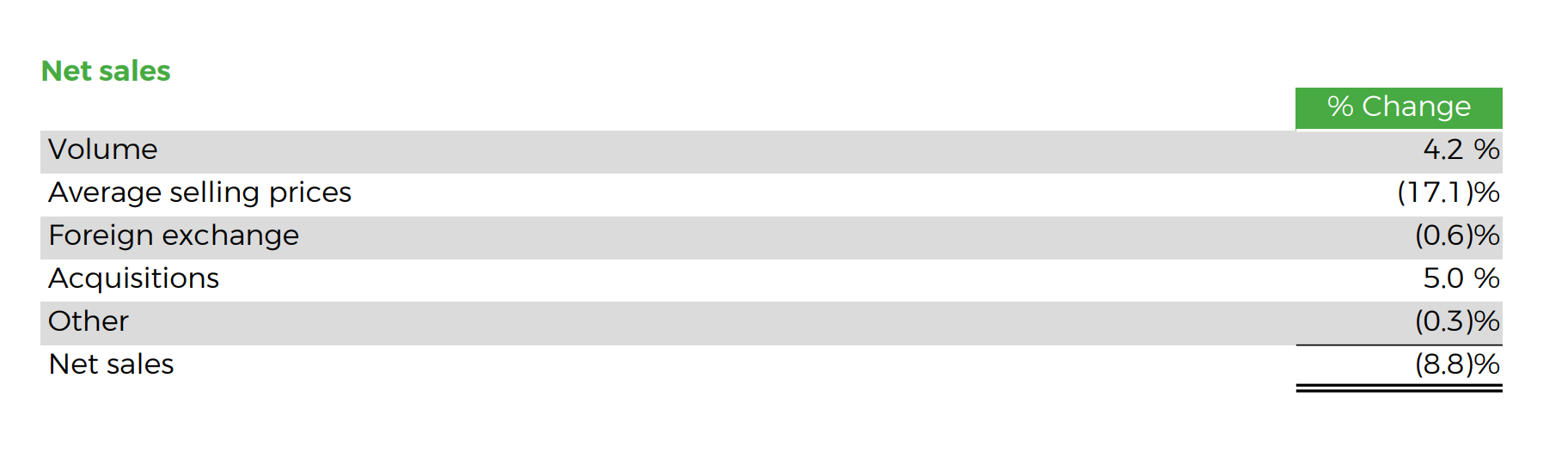

According to their 2022 annual report they had a 34% increase in average selling prices in 2022, which basically accounts for the 33% increase in sales. But volume had already begun to slip.

But then last few quarters the story has flipped, prices have decreased while volume has picked up again. Here’s a snap from their 2023 Q2 results

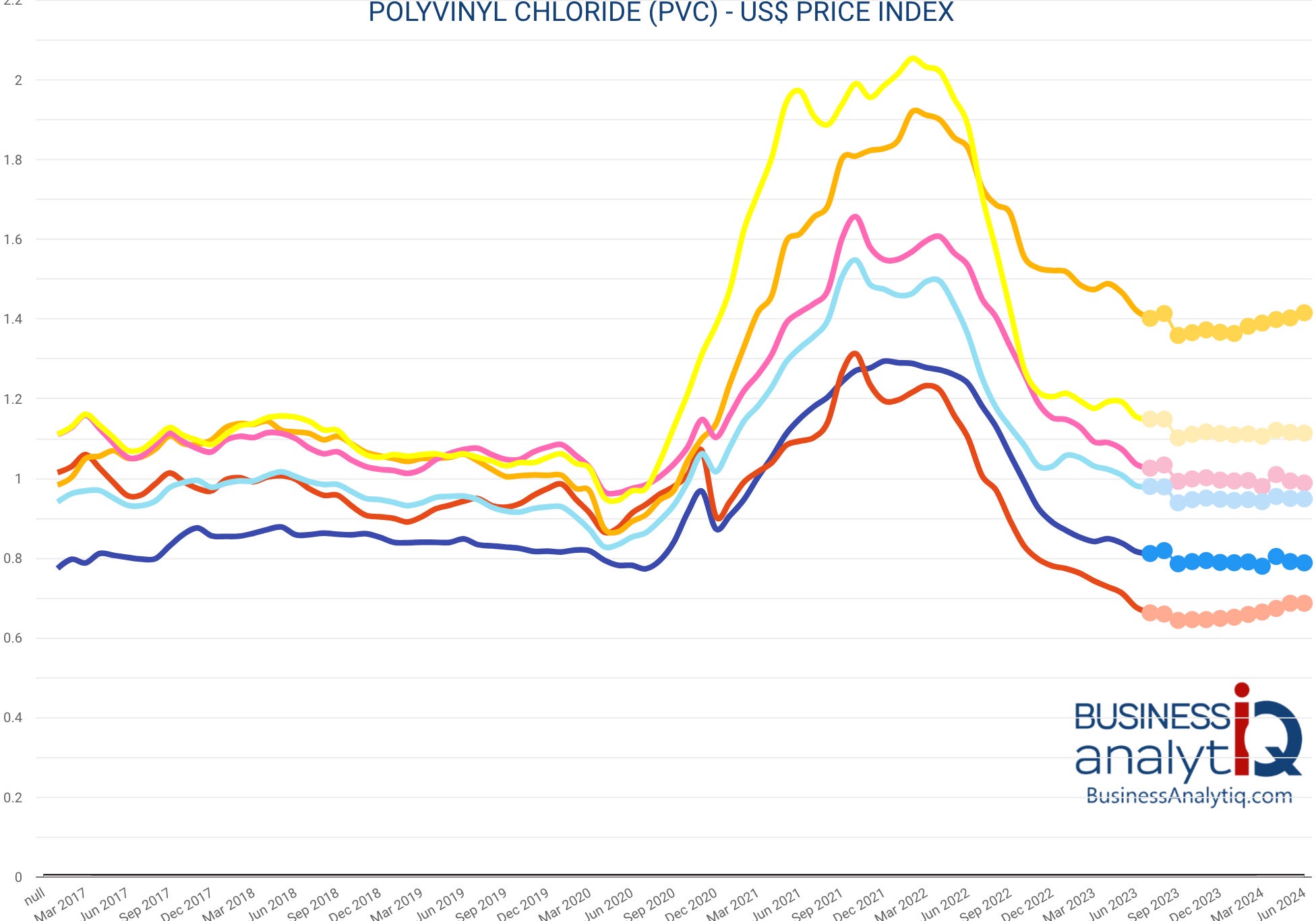

All in all this a sign of a normalizing business, commodity prices are coming down, and yet sales are still coming in. The question is where do operating margins fall to? How much will prices decline? It’s hard to say, HDPE (High density polyethylene) and PVC (Polyvinyl) are two big contributors to their average selling prices and it seems at least PVC has come down quite a bit.

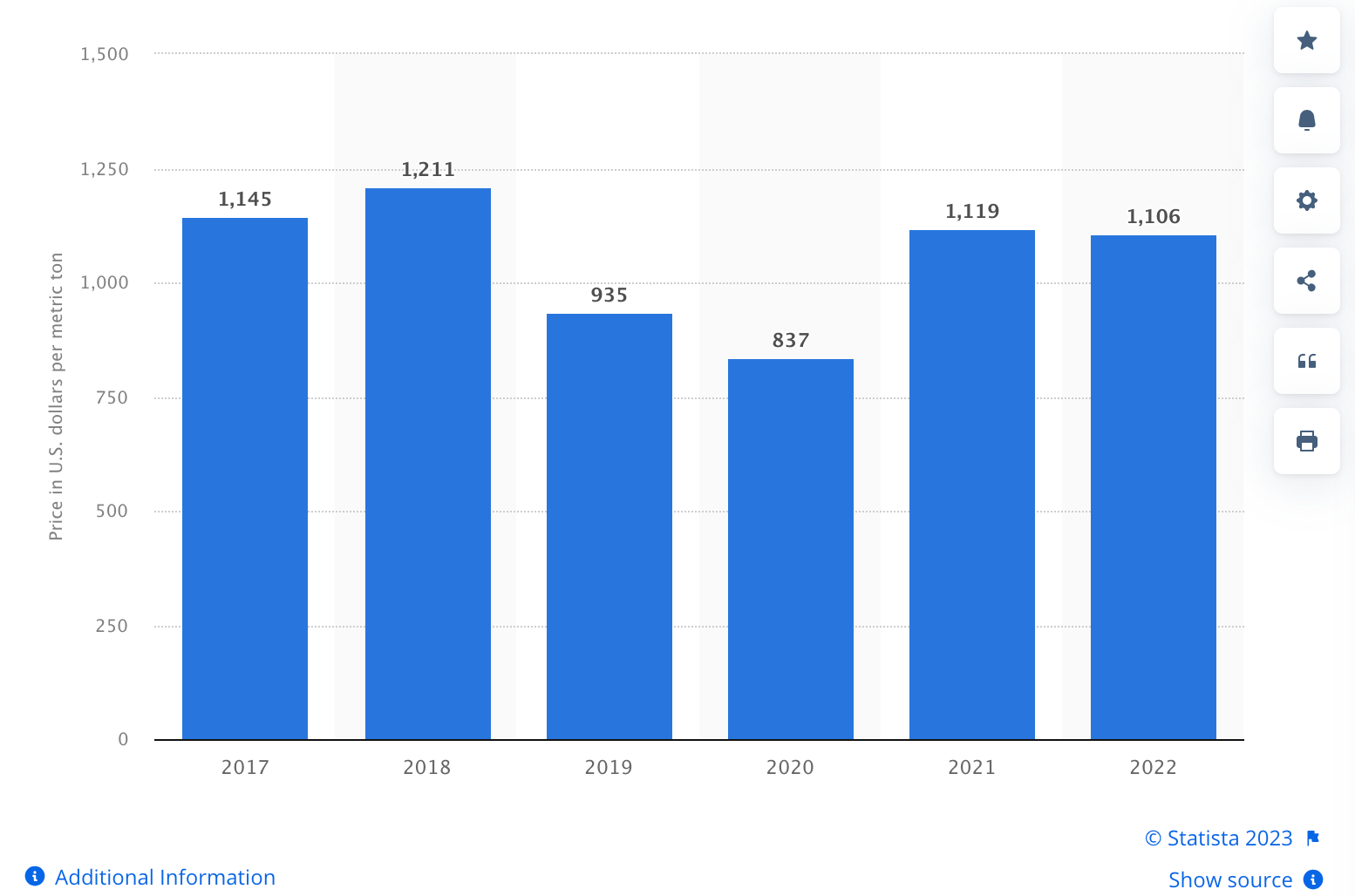

But some materials such as HDPE saw price increases globally after 2020 and seem to have remained elevated. Below is the global price per metric ton of HDPE.

All in all I think the general trend will continue downward and this seems to be what management is indicating as well. Below is a snap from their 2023 Q3 quarterly results. They again emphasized the impact of decreasing average selling prices.

Whether or not margins will fall back to pre-pandemic levels remains to be seen. If they do I don’t think it will be a sudden collapse in prices and margins, although it certainly could happen if the economy takes a dramatic turn for the worst. Instead I expect materials to slowly decline in price, which they have so far, and if they are able to cut costs, they may be able to maintain higher margins than before. But again this remains to be seen.

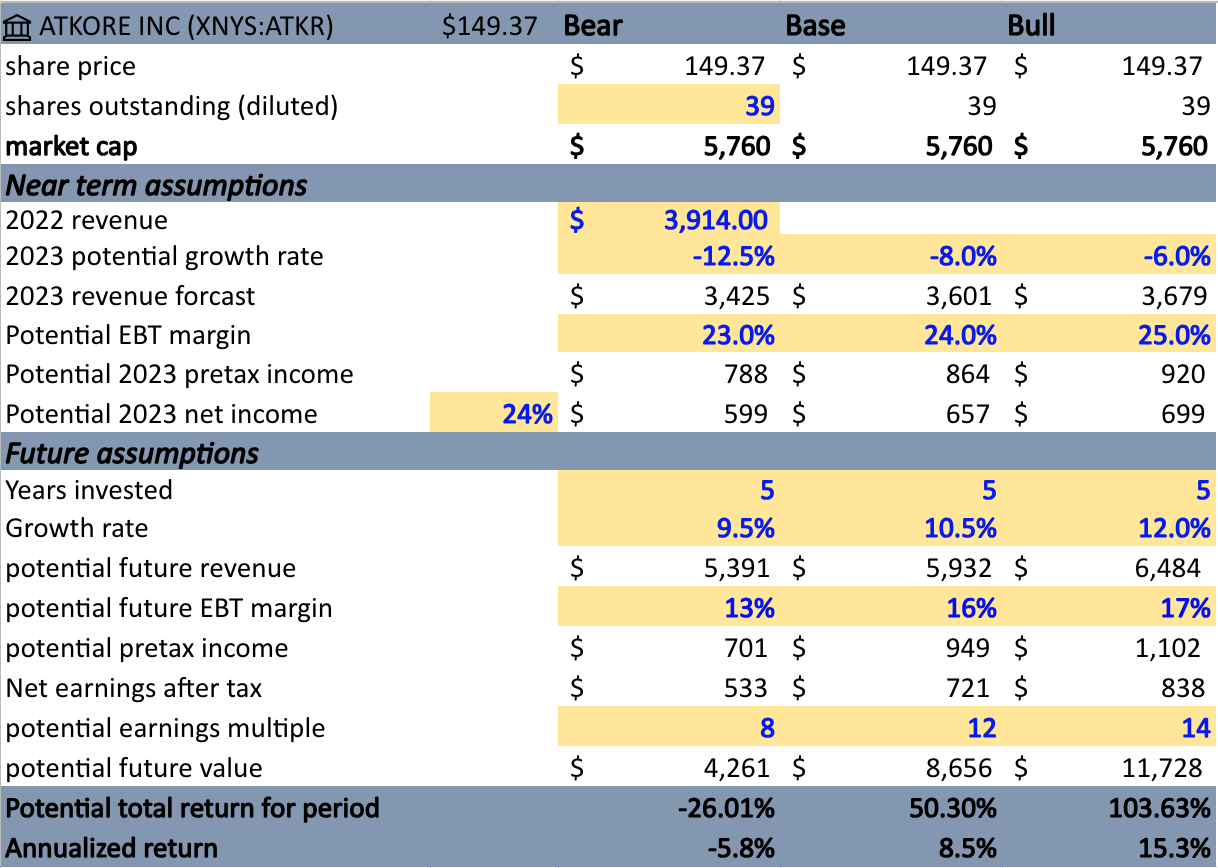

Valuation

I want to be careful not to assume anything too optimistic. They’ve pointed to just over a billion in EBITDA for 2023. They’ve had about a 31% EBITDA margin so I’m going to assume they do about 3.4-3.6 billion in revenue for the full year 2023 which is about in line with analyst estimates. Im assuming their margins shrink a bit in 2023 and revert closer to historical levels over the next 5 years and I’m assuming future multiples ranging from 8-14x.

Conclusion

Now, I’ll be the first to admit, I could be missing something. But if my assumptions are correct, this isn’t a super attractive price. I would be more excited near $120 a share or even less.

Don’t get me wrong, I really think this is a great business and I admire their commitment to creating shareholder value. But at the end of the day, for me, investing is not about buying admirable businesses just because I admire them. It’s about buying admirable businesses at a reasonable price, but first weighing that investment decision against the other opportunities within my circle of competence.

So for now I’m going to wait on the sidelines to see what their margins do and see if there may be a better opportunity to get in later.

Thanks for reading!