11/9/2023

Company Information

Market cap: $43.7 billion

Share price: $204

P/FCF: 21.5

P/E: 50

Ticker: ADSK 0.00%↑

1. Intro and overview

Over the years, as a building contractor, I’ve come to realize that engineers and architects tend to use the same products over and over again. This is because their job job requires the careful calculation of many variables in order to design a dwelling according to the international building code. When they find trustworthy products that work well, they tend to stick with them and those products tend to become the trusted industry standards.

Autodesk has one of those products that has become the industry standard because they provide a superior product that reaches almost every area of the modeling, design, engineering and collaboration process.

AutoDesk is the leading computer aided design software company in the world. They provide design, engineering and entertainment software solutions worldwide. Their customers include builders, engineers, manufacturers, designers, and 3D artists. They’re most widely used in the vertical construction industry (residential homes, commercial buildings), but in reality they serve customers who design and build just about everything.

AutoCAD and Revit are their flagship products, and they have one of the deepest moats in the vertical building industry. This moat comes in the form of high switching costs and an unusual expertise network effect that has entrenched itself deep within both the demand side (employers, engineering firms, hiring companies) and supply side (engineers, experts and professionals) creating a standardized product that has become the foundation of the design, modeling and engineering industry. I will explain more about this in a bit later.

2. History

Autodesk’s history can be summed up into a few distinct era’s.

The inception with John Walker

The refinement era with Carol Bartz.

The product expansion era with Carl Bass.

The return to priorities era with Andrew Anagnost.

John Walker

Autodesk was founded on January 30, 1982 by a computer programmer named John Walker. Walker actually acquired the AutoCad software from an inventor named Michael Riddle and then brought it to market the following year. Walker was particular about management at AutoDesk being tech savvy rather than business savvy and Walker himself is a very intelligent programmer, but with a sort of quirky personality.

Autodesk went public in 1985 and shortly after Walker resigned from president and CEO to focus on programming. AutoCAD went on to become a widely used non specific computer aided design program and the company was doing $100 million in revenue by the end of the 1980’s.

Carol Bartz

In 1992 Autodesk brought on Carol Bartz as the new CEO which marked a shift in the companies trajectory with the acquisition of Softdesk. The acquisition helped transform Autodesk from a design software business into a one that designs CAD software specifically for engineers, architects and builders. This was really the beginning of Autodesk’s journey into the building industry. Several acquisitions after that were aimed at deepening its reach within the industry. Carol remained with the company until 2006 when she was replaced by Carl Bass.

Carl Bass

Carl Bass was the CEO from 2006-2017 and he, like Carol before him, marked yet another turning point in Autodesk’s trajectory, as he began a relentless strategy of acquisition and product innovation. Acquiring 36 companies in his 11 year tenure, 13 of which were between 2007-2008, Bass essentially expanded the companies product offering into areas such as Building information modeling, model-based design, 3d animations, project lifecycle management, product design, and simulation. The company began to serve other professional fields such as administration, estimation, 3d printing, product design, manufacturing, robotics, and various other industries, but the question began to arise as to whether Bass was focusing too much attention and capital in the wrong areas.

The company eventually became embroiled in a battle with activist investors as Autodesk struggled find direction and control costs. The company ultimately became unprofitable again (2016-2019) but was partially due to the transition to a cloud based subscription model which I’ll discuss later. Bass was eventually replaced by Andrew Anagnost in 2017.

Andrew Anagnost

Anagnost was the architect of the Autodesks transition to a subscription based saas model. As CEO his plan was to circle back around and re-focus on the products and industry that originally drove Autodesk’s success, software for the construction, engineering and architectural design industry. Since 2017 Anagnost has made 8 acquisitions that are all construction related and he looks to be focusing on Autodesk’s core market, software for the building trades.

3. Product breakdown

I’m not going to go through all 100+ products they have but I want to talk about their flagship products.

The vast majority of revenue comes from their core AEC and (architectural, engineering, construction) and AutoCAD products which consists of Revit, Civil 3D, AutoCAD and all the different plug ins that are sold along side those. Their manufacturing platform is really just AutoCad and Fusion 360.

Revit

Revit is the single best Building information modeling software on the market for vertical construction (buildings, homes, dwellings) although its also used for civil and commercial work such as bridges, roads, parking garages.

Building information modeling is a process that uses 3d models to give engineering, architecture, and construction professionals insight and interactive tools to plan, manage, design, and construct buildings and infrastructure. Revit allows for collaboration between different professionals and stakeholders during the construction process. BIM allows for data sharing that simply isn’t possible with CAD models. It essentially captures every aspect of the construction process and centralizes it into one interactive 3d model.

AutoCAD

AutoCAD is a 2d and 3d computer aided design drafting software. Although It doesn’t offer the interactive 3d experience that Revit does, AutoCAD is still a very important for drafting different different things and generating blueprints for construction projects. BIM in general is steadily replacing CAD in some sense, but CAD will still be around for a very long time.

If you go to almost any university to become an engineer or architect, you’ll be learning AutoCAD, and then looking for a job at a firm that hires AutoCAD experts. It’s the industry standard for drafting and design.

4. Management

Anagnost holds a doctorate degree from Stanford University and worked at NASA Ames Research Center as a post-doctoral fellow. He’s 54 and has been with AutoDesk since 1997, 26 years, which means the majority of his adult life and been spent working at AutoDesk in various leadership roles such as Senior Vice President, Business Strategy & Marketing.

Ownership

Anagnost owns 58,200 shares of ADSK 0.00%↑ which only equates to roughly $12 million. This hardly anything considering his compensation which is around $17 million.

Im a little disappointed to see that Anagnost also recently sold 22,318 shares of ADSK 0.00%↑ worth $4,952,364 in September. He also sold 43,735 units of Autodesk stock in March 2021 worth over $11,549,101. He’s not the only one, there’s been other insiders selling over the last year or two. This is obviously not what we want to see from management.

The selling could indicate many things, but most likely that the stock was over valued or management wanted to cash out some stock before the crash. This could also indicate there are tough times ahead.

Concerning the low insider ownership, it presents the small risk that management isn’t completely aligned with shareholders in the long term. I prefer founder led companies with high insider ownership, but in reality many companies have low insider ownership and do extremely well with the right compensation and incentives put in place.

compensation

Below you can see that his total pay is around $17.7 million, of which only $1 million is base salary. That means 95% of Anagnost’s pay comes in the form of incentive based pay which is at risk if the company doesn’t perform. The rest of management has a similar compensation structure which creates a strong incentive for them to perform.

5. Capital allocation

AutoDesk has largely dedicated its operating cash flow to acquisitions and buybacks.

Buybacks

Over the last 3 years, they’ve generated about $6.5 billion in free cash flow and they’ve spent $3.2 billion on buybacks. This is good except they bought back stock at very high valuations. On a good note, they’ve continued to repurchase stock now that the it has sold off and the valuation has compressed a bit.

Acquisitions

It would be impossible for me to cover all of the 60 acquisitions made by Autodesk over the years but there are some recent acquisitions that were made by Andrew Anagnost that may be worth examining.

Spacemaker

Spacemaker is an urban planning and design cloud platform that uses generative design and artificial intelligence to help architects and urban designers make more informative early stage decisions. It has features like design automations and fluid connectivity with Revit, one of their top products. They acquired the company for $240 million and it had sales of approximately $5 million. Do the math, thats an expensive deal, around 40x sales.

However it’s a step in the right direction, and they need to stay on top of the ball when it comes to generative ai applications because I think there could be huge productivity gains from ai in the future, especially in this area. Although we aren’t at the point where we can have computers do load calculations or automate mathematical engineering, but this could be possible within our lifetime, and it would be a massive opportunity for Autodesk.

PlanGrid

PlanGrid provides construction productivity software for the construction industry. It essentially allows contractors and developers to manage projects more efficiently as it organizes punch lists, plans, and has certain task automation functions. They paid $875 million for this acquisition and PlanGrid was doing about $70 million in recurring revenue at the time, which is about 12-13x sales. Thats still certainly expensive, however the company was supposedly growing at 50% annualy, which means its probably doing $300-$500 million in revenue this year.

6. Competitor analysis

Autodesk has quite a few small competitors that are less important but they have a some bigger ones that we should keep our eye on.

Bentley systems BSY 0.00%↑

Bentley systems is an infrastructure engineering software company that provides similar products as AutoDesk except geared towards roads, bridges dams and other civil engineering and infrastructure applications.

Microstation is Bentleys flagship product which competes with a few of AutoDesk’s products such as AutoCAD, Civil 3d, and Revit. Microstation is a very popular product for civil engineers who design bridges, roads and dams and it’s sometimes preferred over Revit and AutoCAD.

I wouldn’t say Bentley is a really a threat to AutoCAD’s dominance in the vertical building space, nor in the horizontal space for that matter, but its certainly a competitor to keep in mind. I’ve spoken to many engineers about Autodesk’s dominance here in the US, and the fact of the matter is, AutoCAD and Revit are the industry standard and the main reason for this comes down to a self reinforcing relationship between professionals and employers that have built their entire lives and businesses around Autodesks products.

I’ll discuss this a bit more later. For now, all you need to know is that if its a bridge, roadway or some other infrastructure application, theres a chance its being designed with one of Bentleys products because they can sometimes be more useful in this niche.

Bentley BSY 0.00%↑ is also an interesting company that I may have to do a write up on as well.

Procore PCOR 0.00%↑

Procore is a construction management platform and that competes with “Autodesk Build” with their full suite of construction management soft ware products. Construction management is a complex and tedious aspect of the construction business and software has revolutionized how the entire process is coordinated.

On smaller construction projects you’ll have at least few parties involved such as a property owner, contractor, and various subcontractors (electrical, plumbing, and HVAC). On larger projects, such as commercial construction or civil work, you’ll additionally have investors, lenders, developers, and engineering firms, not to mention tons of employees. All of these parties need to interact, communicate, send and sign documents and agreements, manage project plans, budgets, timelines, payroll and so forth.

Procore is a unified solution that provides project management for builders (contractors). Autodesk build provides most of the same features but is slightly less customizable and limited in certain aspects. Procore is probably an important competitor but its doesn’t compete with AutoDesks core engineering, architectural and CAD products, which make up the vast majority of AutoDesk’s revenue.

7. Moat

Autodesk has done many things to carve out its position over the years. They’ve essentially given their software to educational institutions to train architects and engineers before they even enter the industry.

A while ago I was reading about different network affects on nfx.com and I came across something called an expertise network effect. I believe Autodesk’s primary moat comes in the form of an expertise network effect with a high switching cost. It looks something like the 2 side sided network effect below.

It essentially works like this

Supply = professionals, experts, architects, engineers that know and use Autodesk products

Demand = employers/firms the employ the professionals that use Autodesk products

The more professionals (supply) that use AutoDesk’s products, the more valuable the products become to employers (demand) because employers are able to hire and fire professionals (supply) much easier.

Likewise, as more employers demand Autodesk trained professionals, the more valuable Autodesk becomes to professionals because it’s easier for them to get a job.

Finally, as the network of trained professionals grows the product becomes more valuable to other professionals who are able to share with each other and gain from a standardized tool. For example, there may be many different engineers designing different aspects of a large construction site downtown, and they can all collaborate and communicate effectively because they all use AutoCAD, Revit or Civil 3D.

There are large switching cost for both employers and professionals when thinking about changing to a new platform. Employer’s who want to switch to Microstation need to either train all their engineers to use the Microstation or else go hire a bunch of professionals that already use it. Likewise, if an engineer wants to use Microstation, they would have to first learn the software then go find a company that uses it. In both scenarios it would be very difficult to switch because the software is difficult to learn and most people use Autodesk’s products already.

This is by no means a bullet proof moat, software in general is susceptible to disruption, and Autodesk isn’t immune to that by any stretch of the imagination. But it would certainly take a much better product to unseat AutoCAD and Revit from the throne. If there was only a slightly better alternative, people would probably not switch because of the hassle, which is why Autodesk’s core products (AutoCAD/Revit) go unchallenged in any serious sense.

8. Growth drivers and industry analysis

When thinking about growth drivers for a company I always ask a few questions.

Is it taking marketshare?

Is the market growing?

Is it raising prices?

Marketshare

Autodesk already has such a large share of the CAD (40% +) and BIM (39%) market that they may not grow significantly through taking share.

They could theoretically take share away from Microstation in the infrastructure market if they really innovate there. They could also take share in the media, entertainment and manufacturing markets if they really focused on them but I doubt they will because Anagnost has made it pretty clear that the priority is the construction and architectural market.

Market growth and pricing power

As far as the over all construction market, it’s expected to grow at about 3-5% CAGR until 2030. I expect that AutoDesk will grow at least at that rate.

Pricing power is one area where Autodesk shines. They offer such crucial software that they’re able to raise prices each year without a problem. They’ve been able to raise prices around 5.7% per year since 2019. If you really think about it, they almost levy a tax on the entire AEC industry, a tax that they raise every year. The reason I say almost is because technically some professionals do have the choice to use a different program, but many times they don’t, it just the industry standard. Regardless, this is a really good position to be in and it affords them some pricing power. Revit is currently $2,835 per year and I’m fairly confident it will be higher next year.

It’s yet to be seen if this will continue through the full economic cycle, but it general, as long as competition doesn’t put pressure on them, I expect Autodesk to continue raising prices without a problem, unless of course there’s a deep housing recession or something.

9. Financials

Notes on the income statement

Autodesk became unprofitable during a brief period (2016-2019).

The main reason for this has to do with how subscription revenues are initially recognized. Revenue can only be recorded when the product is delivered and according to the accounting rules, when a customer buys a 1-3 year subscription its not considered fully delivered until the entire period is up. Even though the whole amount is paid on day 1 the revenue is recorded incrementally over the period and temporarily held on the balance sheet under deferred revenue. This also explains why they have much more cash flow than earnings.

Their earnings have grown at over 13% per year over the last 10 years and they’ve had very high returns on invested capital aside from the few years where they transitioned.

Balance sheet

Current assets don’t cover current liabilities because of the deferred revenue recognition mentioned above, which is recorded as a large current liability. It’s been this way since 2018. I’m not really concerned because deferred revenue doesn’t represent a cash outflow like debt or something, unless of course a bunch of people cancel their subscriptions within 30 days of their purchase, in which case Autodesk would have to refund customers, which is highly unlikely.

All in all this is a capital light business requiring around just 3%-5% of operating cash flow to fund capex, having very little fixed assets on balance sheet. They have $2.4 billion in debt on the balance sheet and they generate $2 billion in operating cash flow which means they could pay their debt off fairly easily if they devoted cash flow to it.

Cash Flow statement

Autodesk is a cash machine but there are a few things to take into consideration before we get all excited about the cash flow. First, like we talked about above, some of this is due to deferred revenue and second, some of it’s also from stock based compensation which allows for more cash generation, but at the expense of diluting shareholders.

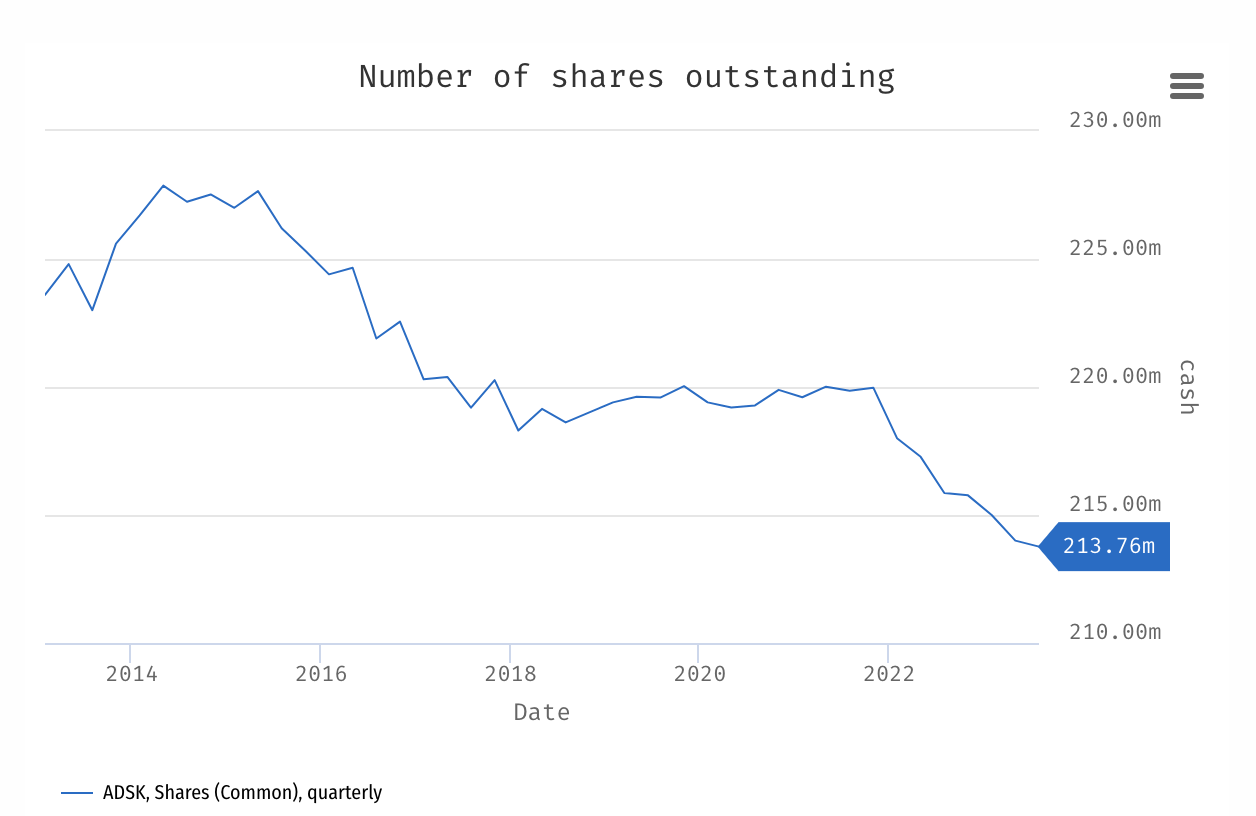

For a long time SBC dilution basically offset share repurchases until recently they began to buyback stock at a higher rate so the shares outstanding are actually being reduced. Regardless, SBC is still dilutive and while it allows for larger amounts of cash flow, its an actual expense to share holders.

10. Valuation

Its hard to use a historical growth to gauge future growth for this company because the saas transition (2016-2019) skewed the numbers a bit. But I’m going to assume the industry grows at 3.5% and they’re able to raise prices a bit each year over the next 5 years, that gives us 8% as a reference point. Even though the company is trading at roughly 22x FcF, its still 50x earnings. I’m going to assume the multiple shrinks or stays the same and the company grows between 5.5%-9% per year.

Final thoughts

I would like to own this business, it’s fairly understandable and stable, it has a moat and pricing power. But it’s a bit expensive for me now. Call me cheap, but I like a good deal and right now Im looking for something that can provide more upside than this. I really wish I could get it below $170 which would build in a bit more safety. We’ll see, for now I’m just watching this one.

Thats it for this week, thanks for reading!

Good and reflecting article! What about nemetschek?

Very good write-up! Not only is the business interesting, but the secular growth of engineering and simulation software is also quite promising, with multiple growth factors such as labor shortages, cost reduction, digitization, and automatization.

I recently took a deep dive into Mensch und Maschine Software, the biggest VAR (Value-Added Reseller) of Autodesk software in Europe, and was amazed by the vast opportunities ahead.

In my latest Friday Roundup, I included a link to your insightful analysis👇

https://open.substack.com/pub/rhinoinsight/p/the-friday-roundup-14c?r=2587ts&utm_medium=ios&utm_campaign=post