Crane Co.

An highly engineered components manufacturer

Key information

Ticker: CR 0.00%↑

Share price: $195

Investment type: Quality

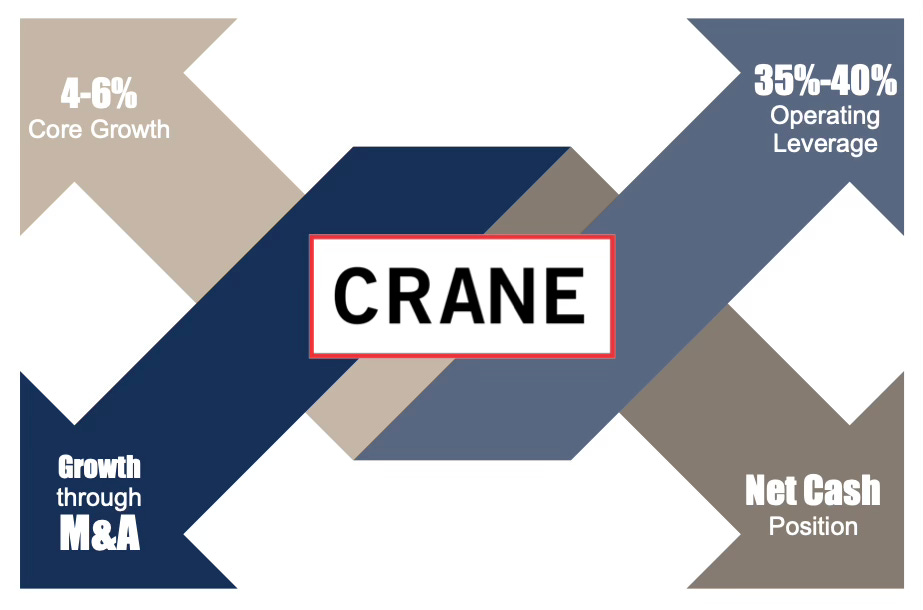

Key return drivers: Margin expansion, modest growth, small dividend.

Market cap: $11.2 billion

2025 EV/EBITDA: 20x

2025 EPS: $5.50 - $5.80

Intro and Overview

Crane Company CR 0.00%↑ is a manufacturer of engineered components that spun-off from Crane Holdings in 2023 ( subsequently renamed Crane NXT). The separation was the result of a longer term plan under CEO Max Mitchell to transform Crane’s portfolio and optimize capital allocation with in the company. The spin off created two companies; Crane NXT, a payment & merchandising technologies business, and Crane Company, a highly engineered industrial components manufacturer in the aerospace and process control industries. Today we will be talking about the latter, Crane Company.

The company produces highly engineered, mission critical components with a high cost of failure. These are specialized products such as anti-skid braking systems for commercial and military jets, power conversion solutions for spacecraft, lubrication systems, and industrial components such as process valves and cryogenic pipes, valves and fittings.

The Aerospace and electronics segment in particular positioned for growth and is established with key commercial aircraft platforms such as the Boeing 737 Max, Airbus A320 neo, Embraer E2, and COMAC C919, and also defense and space platforms like the Lockheed Martin F-35. Crane has almost 100% marketshare with a few products as they are the sole-source provider for those products. 40% of Cranes revenue comes from aftermarket parts, which is recurring in nature. Many products are highly regulated and engineered which creates customer stickiness.

History

Crane’s history goes back 170 years to Chicago, where it was founded by Richard Teller Crane on July 4, 1855. Teller produced custom valves and fittings for various industrial applications. His company grew rapidly with the second industrial revolution in America. Demand for fittings and valves increased dramatically for railroads, elevators, and steam engines—industries in which he served. In the 20th century the company became an innovative leader in industrial valve fitting manufacturing and also diversified its product mix to includes high-end bathroom fixtures.

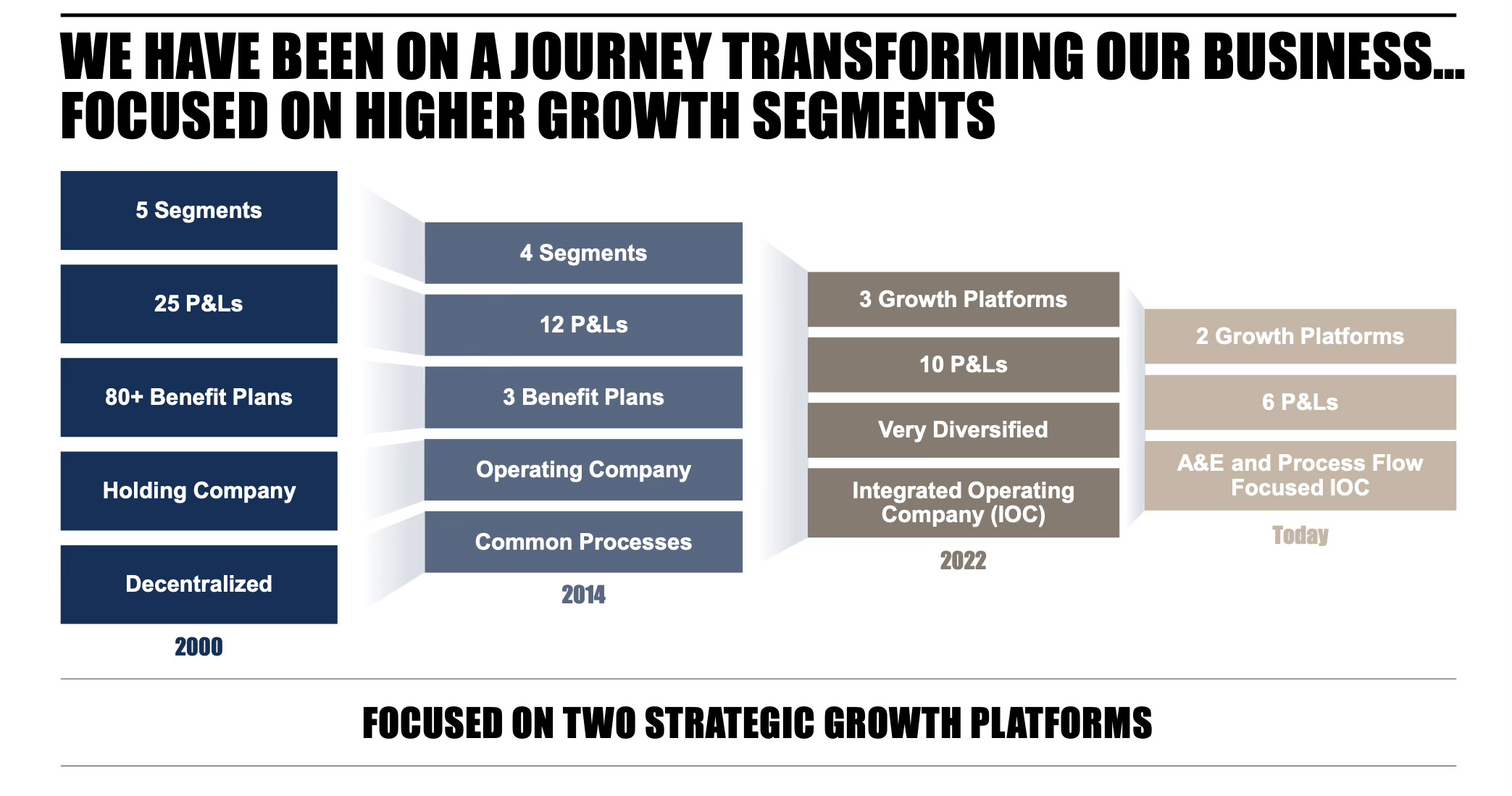

The post-War era saw a boom in conglomerates and Crane was no exception. Under new management, the company expanded into Aerospace, fluid and solution control, steel, payment and merchandising technologies, and building products. However, in the 1990’s and 2000’s, the company began divesting assets such as commodity plumbing and building materials in order to once again focus on higher margin, highly engineered and mission critical industrial components. It wasn’t until CEO Max Mitchell was promoted in 2014 that this process really accelerated.

Crane has since undergone a transformation where low performing segments have been divested, high growth segments have expanded, financials have become simplified, and the operation has become more streamlined. This multi-year process fundamentally reshaped the company's portfolio and financial profile. The spin-off was marketed as a strategic separation but practically, it was just one more step in streamlining the company, except this time entire segments were divesting into a standalone company.

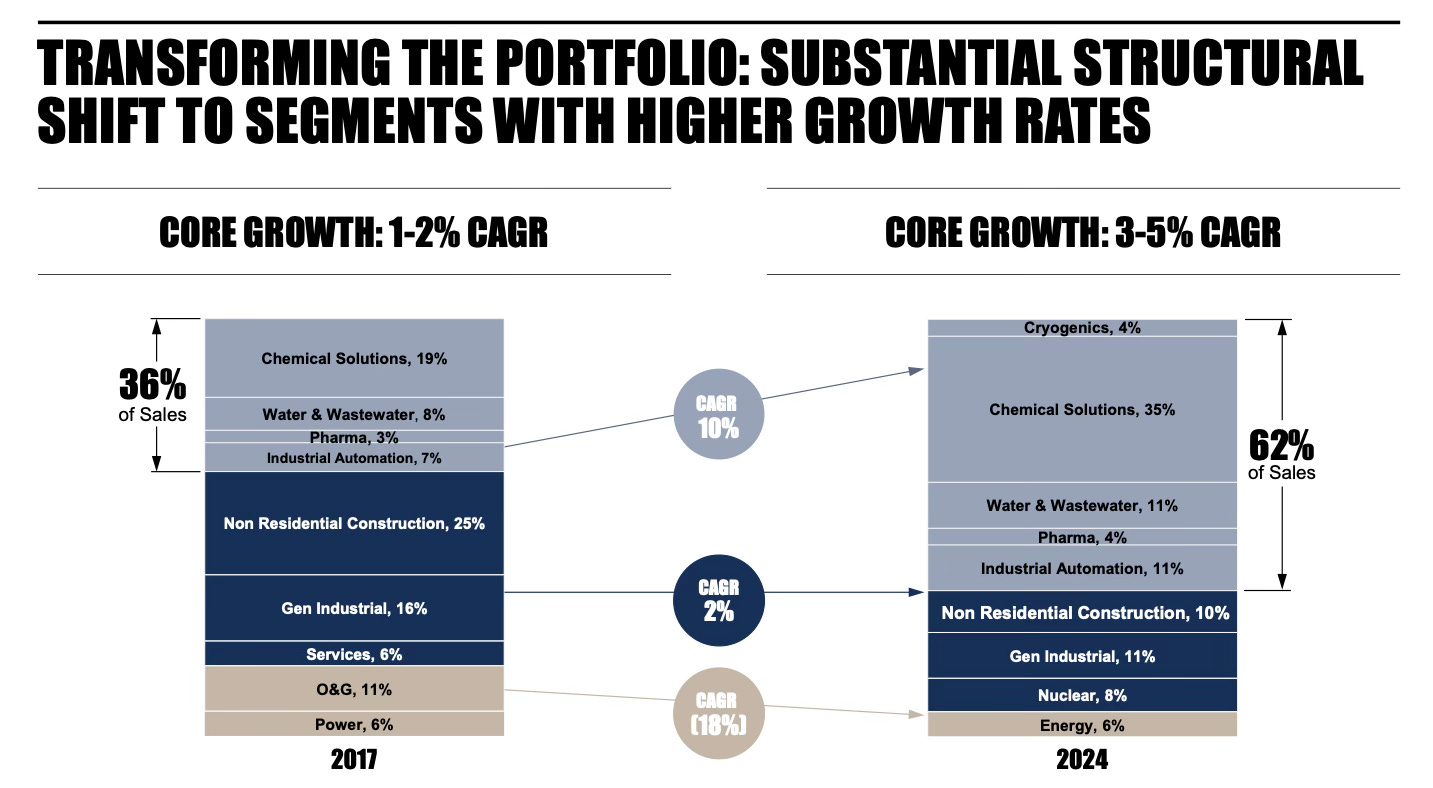

Today Crane has two growth platforms: Aerospace & Electronics and Process Flow Technologies. Below you can see how much Process Flow Tech has changed since 2017. Oil, gas and energy shrunk from 17% of revenue to just 6%,, and oil and gas has been diverted completely.

This transformation has already produced impressive shareholder value and margin gain. Between December 2020 and August 2025, the combined equity value of Crane Company and Crane NXT increased by 210%, which is about $9.7 billion in total equity value creation. The combined segment level adjusted operating margin has grown from 13.4% to 22% in that same time.

Crane Business System

CEO Mitchell and senior vice president of Process Flow technologies both came to Crane from Danaher. I assume most reading this know what Danaher is. If you don't , it’s a well-known, very successful life sciences serial acquirer that has outperformed the market by a wide margin since founding. Danaher is known for the “Danaher Business System” which is a systematized used of kaizen manufacturing, where everything is measured, monitored and incrementally improved into perpetuity. Danaher really pioneered and perfected the business system.

It’s not uncommon that managers leave Danaher and become involved in other companies with similar characteristics such as Idex, ITT Inc, Atkore, Esab, Ametek, and Roper, to name a few. These companies also deploy some version of a business system where everything is closely monitored for the purpose of small, constant, and incremental improvements.

The Crane Business System is no different. Often referred to as “The Machine”, it is a company-wide system that drives success and profitable growth. It does this by implementing process analysis and control, extreme accountability, and problem-solving. Collectively, these drive constant improvements in the company. As soon as a goal or target is achieved, a new one is set, and the process begins again. There is no substantial end to the improvements, and it enforces a “never good enough” mindset. This is very similar to Danaher’s system.

Crane typically acquires companies in high growth markets. Once acquired, the company is fully integrated within 100 days and the Crane Business System goes to work. A 10% ROIC is expected by year 5.

The business systems is applied in the following ways.

Identify leaders within the acquired company that can be trained in the Business System process, or share leaders from external sources such as Crane or new hires.

Deploy a value-pricing strategy. This is a fancy way of saying they attempt to raise prices according to the perceived value that their components provide to their customers. The logic behind this is that they have high-value products that are mission-critical and therefore should be valued based on their usefulness, rather than the cost of materials plus a mark-up.

Product Line Simplification. They eliminate low ROI products and reduce the complexity and number of products. They focus on core profitable products and the top customers.

Drive factory transformation, including reducing lead times, and using KPI’s and repeatable cadences to drive performance. All of this is carefully monitored, documented and workers are both held accountable for improvements and rewarded as well.

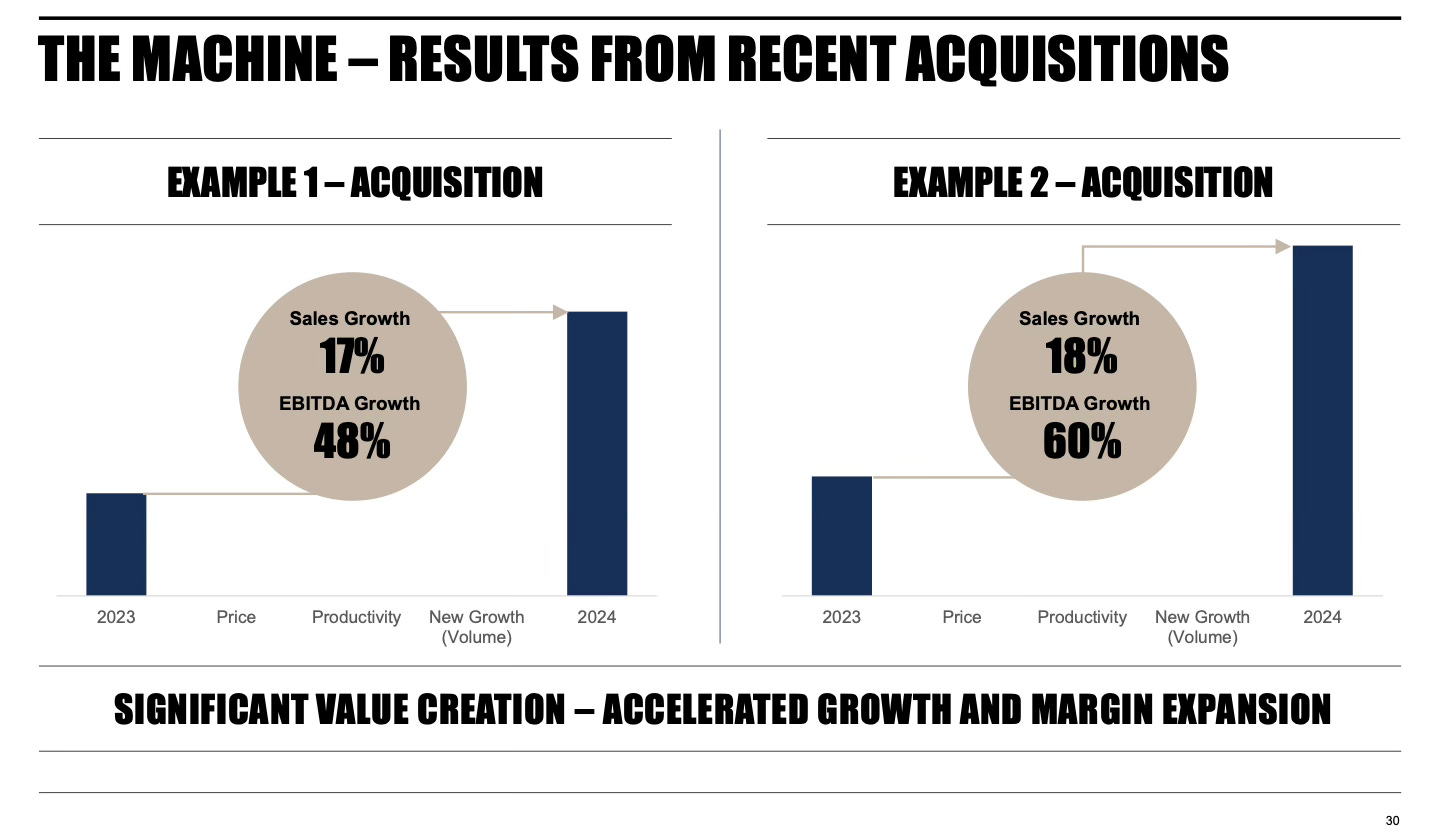

The results are impressive to say the least. Below are a few acquisitions examples showing their system in action.

Now, I’m almost certain these are cherry picked examples that are used to tout their business system. Regardless, 60% EBITDA growth on 18% revenue growth implies serious operating leverage from productivity gains.

Operating leverage

The Crane Business System has delivered overall operating leverage for the company as well. This is key to the thesis.

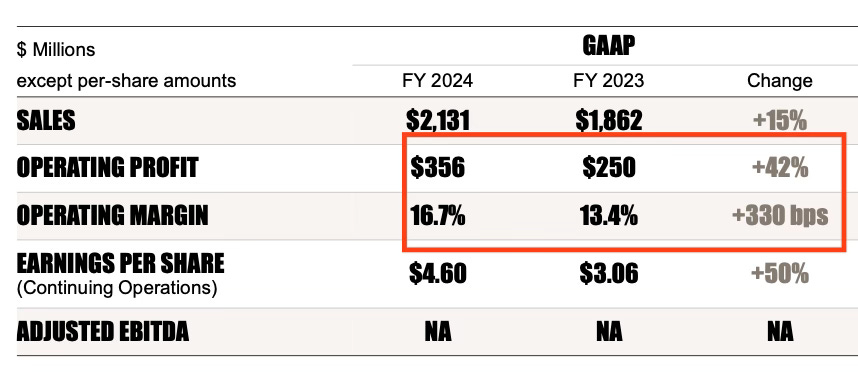

The company targets 35% - 40% operating leverage. Now, operating leverage is usually expressed as a ratio, but the company has chosen to divide the nominal change in sales and operating income, which gives you a percentage. However, the better way to think about this is just to divide the percentage change in operating income by the percentage change in sales, which gives us 2.8x. This means that for every 1% in revenue growth, operating income grows by 2.8%, which is good. Even more impressive, in 2023 operating income grew 4x the rate of sales.

Crane has a 16.7% GAAP operating margin, and 18% adjusted. Looking at the segment level which excludes certain corporate expenses, the operating margin jumps to 22% in 2024 and is expected to continue to expand going forward.

Moat

Switching costs/niche engineered products

Cranes position is so strong in some markets that it has 100% share in markets such as lube and scavenge pumps and fuel transmitters market for new engines. The company is also #1 many markets, including power conversion products, which have been used on every Aesa radar developed in the lat 10 years.

Crane benefits from the highly engineered nature of the products they sell. The customer isn’t primarily concerned about price, but instead about quality because there is a high cost of failure, sometimes even catastrophic. So, Crane aims to offer a differentiated product where the customer would have few other quality substitutes, and in some cases Crane is the sole-supplier. Given the critical nature of the products, customers are often hesitant to switch if Crane has been working with them for years and a product has been working well. In many cases, once Crane has an installed base, the company will continue to get aftermarket revenue for years to come.

While Crane aims to limit non-recurring engineering work, engineering activities are centered around developing and customizing existing products to meet the needs of their customers. For example, Crane identified a solution for their customers, and led a full brake control system redesign and retrofit for C-130’s and B52’s military aircrafts, which are old aircrafts. Crane is able to identify unique opportunities like that to provide upgrades and modernizations efforts for their customers, which can help lock-in customers.

I would give this moat a 7 out of 10 since there’re are some barriers to entry, and some switching costs, but also some products have less advantage than others.

Growth and opportunity

Process Flow Technologies (PFT)

Process Flow technologies is led by Shangaza Dasent, who recently joined from Danaher. The segment produces a variety of engineered valves, pumps, fittings and other fluid and gas control components that are used in industrial settings. The simplest example would be a bellows seal valve, which is designed to provide a hermetic, leak-proof seal. This type of valve is indispensable in certain applications where any leakage of the contained fluid or gas would be extremely dangerous, costly, or harmful.

50% of PFT revenue is derived from the sale of different valves similar to this, 33% from pumps and sensing instruments, and the remaining 18% is services and pipe fittings.

The core target markets in PFT are chemical, water and wastewater, pharmaceutical, industrial automation, and cryogenics. Management has shifted the sales mix to emphasize these target markets, and they have grown them by 72% since 2017—now making up 62% of total sales for the segment. This shift has driven the segment’s adjusted operating margins from 10.9% to 21% between 2016 - 2024. Overall margin gains for the whole company have largely been driven by this segment.

PFT does $1.2 billion in revenue and operates in a $18 billion addressable market with 50% of sales flowing from aftermarket, implying healthy recurring revenue potential. PFT is set to grow at a 3% - 5% CAGR over the coming years. Although this is the slower growth segment compared to Aerospace, management expects to reach mid-20% adjusted operating margins over the next few years. Hypothetically, with 5% revenue growth and a 24% margin, the segment could be doing around $330 million in operating income in 2028, implying a 33% increase.

Aerospace and electronics (A&E)

Aerospace and electronics provide niche components for both commercial and military aircrafts, with a split of 60% commercial and 40% defense. The total addressable market for A&E is about $8.9 billion.

A&E revenue grew 18% in 2024—reaching $932 million and is expected to have slightly higher long term growth at 7% - 9%. Management also believes adjusted operating margin can reach mid-upper 20%’s over the coming years. Assuming 7% growth and a 25% margin, A&E could be doing $300 million in adjusted operating income in 2028, putting potential total adjusted operating income for both segments over $600 million.

Most of Cranes products in this segment have the #1, #2, or #3 market position in their respective markets and as previously noted, some markets they are the sole provider. Aftermarket in A&E is only 35% but this figure is growing.

Management

Max Mitchell is a large shareholder with a stake in Crane worth $147 million, which is 122x his base salary and 15x his total compensation after awards and incentives. This suggests plenty of proper incentive. 85% of of his total compensation is tied to performance based metrics such as share performance and EPS and free cash flow targets.

The rest of management are not notably large shareholders with total insider ownership sitting at around 2%.

Risks

I wouldn’t say this is a very risky company overall, but there are a few things to keep in mind.

M&A risk: Organic growth will be sluggish so Crane will be dependent on identifying acquisition targets and continuing the disciplined process of integration and optimization of acquired companies. Without this, growth is likely to hang around the low single digits and margins will have trouble expanding.

Government defense spending: Military accounts for 39% of A&E segment, if there were to be a significant cut to military spending, it would have a dramatic effect on sales.

Financials

Crane has an excellent balance sheet with a net cash position of $285 million and $800 million in potential borrowing capacity for future acquisitions. Most of the company is financed through operating cash flow, with the exception of acquisitions which occasionally require debt. Crane also has no long-term debt, and the current portion of debt can be paid off in less than 1 year if necessary. After the closing of an upcoming acquisition, Precision Sensors & Instrumentation (PSI), Crane should have net leverage of 1x EBITDA, which is below their long-term target of 2x -3x. Free cash flow conversion is also incredibly high between 90% - 100%, suggesting that the company is efficiently converting profits into cash.

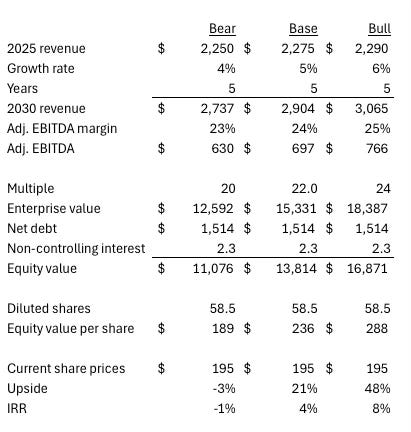

Valuation

Valuation is a less appealing part of this story at 37x earnings. The stock is up 160% since going public, and investors are already anticipating that the company will continue to improve margins and drive modest growth through organic + m&a. it should be obvious by now that this is not a growth story, but instead this is a margin story with potential buybacks in the future.

Below are a few assumtions for the valuation.

Growth between 4%- 6%. I take management at their word because they don’t operate in fast growing industry and m&a only contributes about 1% - 2% of growth.

Adjusted EBITDA margin of 23% - 25%. Current margin is around 20% and growth is expected. It is possible I am underestimating margin expansion here, but this is a similar range to peers.

Multiple of 20x - 24x EBITDA. This is a high multiple, and represents a slight expansion in the base and bull case. Crane deserves a high multiple considering its market position and relatively low risk. It trades at a similar multiple to top-notch industrial manufacturer rolls-up such as Ametek, Transdigm, and Parker-Hannifin and Woodward Inc.

Net-Debt in 2x - 3x range, per long term target.

Final thoughts

This is a really interesting company but an easy pass for me. Although I really like Crane’s enormous market share in key aerospace markets, the company is a bit richly valued for me. Investors seem to be pricing in ever-expanding margins and multiples, or pricing it as if it’s the next Danaher or Heico, which I would put into question. Crane definitely fits the profile of a typical industrial compounder. Sometimes these types of companies can be richly valued for many years, and in some cases they even expand their multiples even more. But one has to have a ton of conviction in order to enter at 45x free cash flow, conviction that I just don’t have. Nevertheless, this is a good company to put on my watch list and that’s exactly what I’ll do.

Thanks for reading, that’s it for this week.