Crocs. Cultish, casual and cheap

Crocs. Cultish, casual and cheap

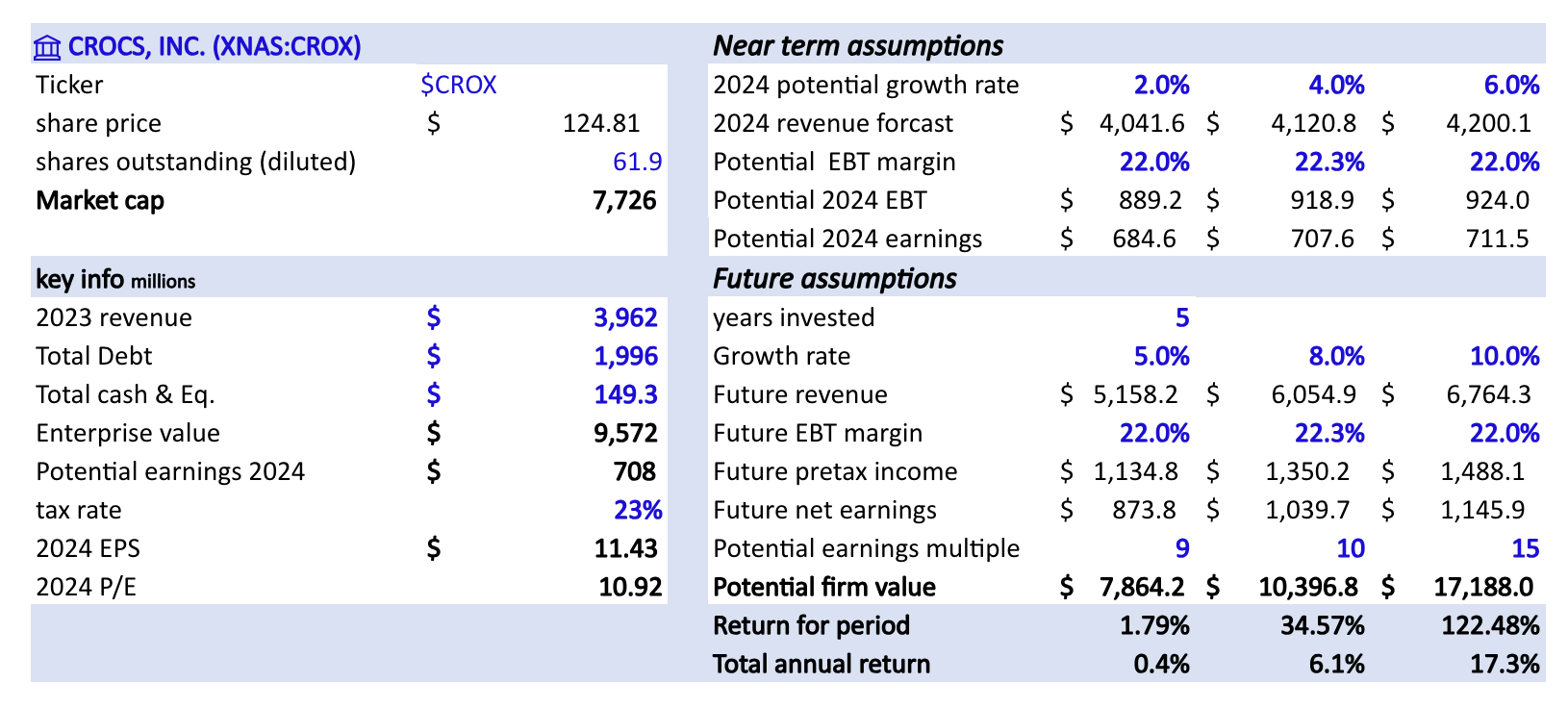

$CROX

Key company information

Market cap: $7.45 billion

Sales: $4 billion

Earnings 2023: $792 million

P/E: 9.6

Share price: $123

Overview

Croc’s is a global casual footwear company. They engage in “design, development, worldwide marketing, distribution, and sale of casual lifestyle footwear and accessories.” They’ve become popular and have developed a cult like following. They sell 150 million shoes annually in over 85 countries and they’re one of the top ten “non-athletic” shoe brands in the world.

Crocs Inc. actually owns two different casual shoe companies/brands.

Crocs: about 76% of revenue.

HEYDUDE: 24% of revenue.

Both of these brands have become very popular casual shoe brands that have simple, light weight, washable designs and they’re easy to slip on and off.

Crocs

Crocs are very difficult to describe, they’re not quite a shoe but not quite a sandal. I don’t know if you ever heard of clogs but they’re essentially open ended wooden shoes that are popular in Scandinavia. So Crocs are basically a ver comfortable, soft resin version of clogs that have become wildly popular, particularly among younger generations, health care workers and middle aged parents. They make a hundreds of variations of these clogs and that also have hundreds of variations of Jibbitz—clip on charms— that allow people to customize their Crocs endlessly. Below is the basic black version of their clog.

The main value proposition is their comfort, ease of use, price and ability to be cleaned easily, oh and of course there’s hundreds of combinations of clogs and Jibbitz for just about anyone’s taste. You can have everything from your favorite university or NBA team to Mcdonalds Hamburglar edition clogs. They also make various other slip on shoes and sandals.

It seems the Jibbitz are far more popular with younger kids rather than adults and hospital workers who prefer more simple variations of the shoe. I imagine kids at school probably share and compare their different clogs and Jibbitzs with each other, similar to how collectable cards were shared and compared when I was a kid.

Each season they employ digital marketing programs with famous celebrities and they launch new variation of their products.

On a side note before we move on to HEYDUDE’s, Crocs are somewhat high margin products considering the majority of their shoes are essentially a piece of glorified plastic polymer sold for $50 or more. Because of this, they’re afforded higher margins (56% gross and 20% net) compared to competitors such as Nike (43% gross and 10% net) and Deckers outdoor (50% gross and 14% net).

HEYDUDE

The other brand they acquired a few years ago is HEYDUDE.

HEYDUDE’s are far more fashionable for older men and women, and yet they have a similar value proposition. They’re comfortable, easy to slip on and easy to clean. As a matter of fact they can be cleaned in a washer without destroying the shoe.

Similar to Crocs they only have a few different kinds of shoes for men and women, but they release endless variations of them. They’ve begun releasing various sports team editions such as LSU (pictured above, top right)

In my opinion HEYDUDE was a good acquisition from a brand standpoint because it fits well with their over all casual footwear strategy, but integration of two brands is not always a simple task.

Management

The current CEO has been with the company since 2014, working his way up to CEO in 2017. He owns about 1.6% of the company (worth $750 million as of march 2023) and he has a total of 25 years in the footware and retail industry. For a CEO who isn’t the founder he has a decent sized position in the company— showing his commitment to shareholders. His total compensation is about $10 million (2023), which is a fraction of the value of his equity stake in the business. Most of his compensation is performance based and at risk if he doesn’t perform, as you can see below.

Under Rees, Crocs acquired HEYDUDE in 2022 for $2.5 billion which was about 3.5x sales and somewhere around 20x earnings—assuming HEYDUDE has a similar net margin to Crocs. My first thought was that they overpaid a bit especially considering it was a private company, however, HEYDUDE did grow 26% last year which may justify the price a bit. The acquisition was paid for with about $2 billion in debt and $450 million is stock.

To be honest, I see why the stock sold off so dramatically, this was a big risky bet funded mostly by debt. Sometimes big acquisitions can be difficult to integrate and they up destroying shareholder capital.

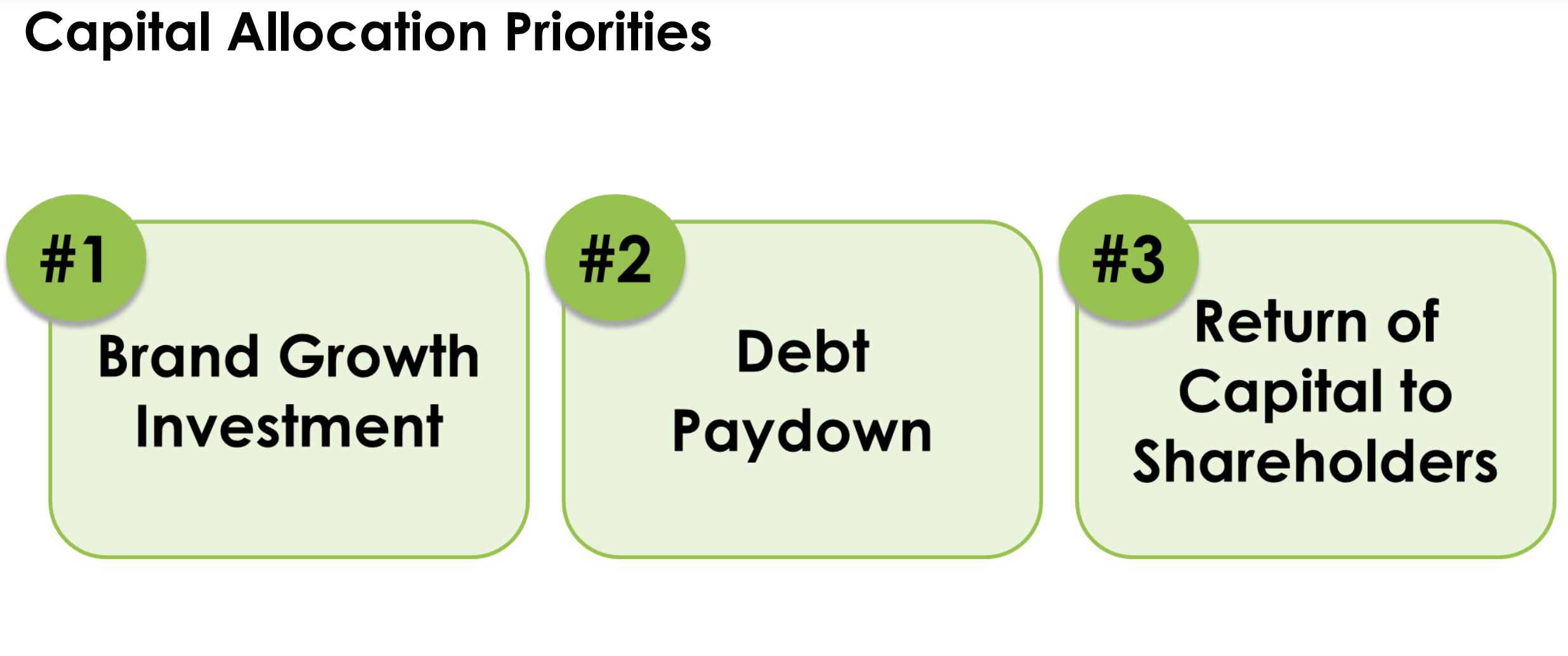

On a brighter note, they’ve paid down almost $1.2 billion in debt since the acquisition and they’ve been consistent in buying back shares— retiring about 33% of shares outstanding since 2011, which is great.

I’d love to see them continue paying down debt, buying back shares and quit the huge acquisitions. They currently generate about $800 million in free cash flow which is around a 10% FCF yield.

Risks

Passing trend

The obvious risk with a company like this is that they could simply be a passing trend or fad. Some people have pointed out that the Crocs brand has been around for a long time and has only grown the strength of their brand over time, indication staying power. While this may seem like a valid point, it’s possible that casual footwear only recently became popular, therefore swinging the trend into Crocs favor.

In order for Crocs and HEYDUDE to succeed they must continue to produce shoes that are appealing to the culture, and in my opinion this means venturing outside the casual footwear market if demand moves in that direction. This is often the nature of shoes and apparel in general. Some shoes such as Converse Chuck Taylors and Vans old schools have managed to maintain timeless style through the ages, but in general, most shoe companies must keep up with the fashion trends.

There is a chance that Crocs and HEYDUDE shoes eventually turn into collectables seeing as how they constantly release new and special addition shoes, but this is just speculation at this point.

They also depend on celebrities to endorse them which could end up being a liability if styles change and they aren’t able to continue having celebrities endorse them.

Financials

Overall I like what I see with Crocs financials, they seem like a somewhat financially sound company.

Although they took on a lot of debt for the HEYDUDE acquisition, its really isn’t an extraordinary pile of debt now after they paid down $1.2 billion last year. They’ve made it a priority to continue deleveraging which makes me feel a little bit better about the company. To put it into perspective, they have about $1.8 billion in net debt and they generate about $930 million in cash from operations as of 2023, this means they could theoretically pay it down over a few years if they continue to grow their cash flows.

All of their margins have improved over time, especially their net margins which exploded after turning profitable in 2017. Although they did have a pandemic boom, their sales have come back down to pre-pandemic levels— growing at about 13%.

Valuation

This company is bit hard for me to value simply because it’s unclear how much they will grow going forward. The million dollar question with this company is whether they are just a temporary trend or a long term brand. I do believe they benefitted from the casual “stay at home” fashion trend that we saw during covid, but I’m just not sure how sticky it will prove to be.

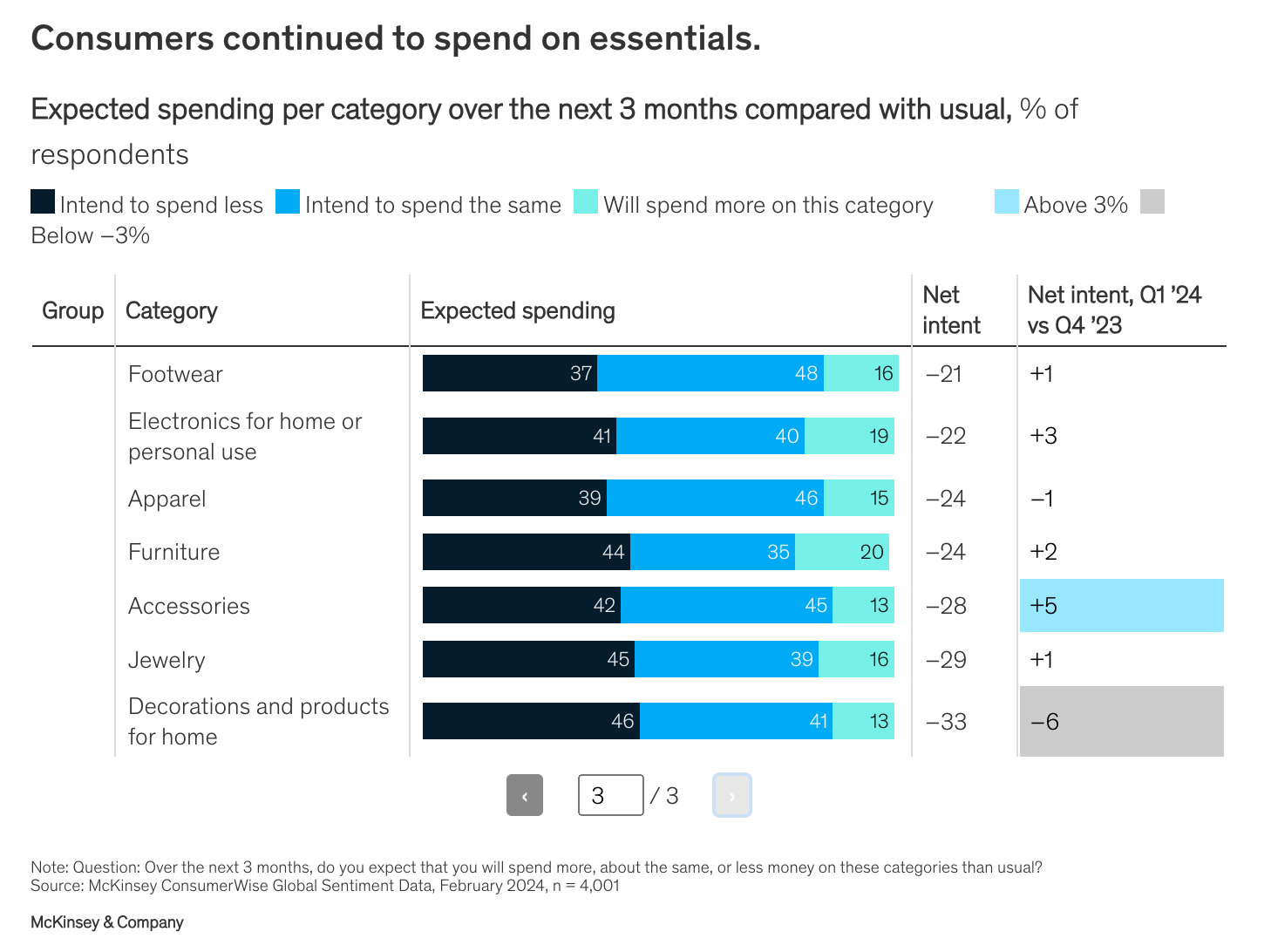

I’m assuming growth will slow down a lot in 2024 because they had such explosive run up over the last few years it’ll be hard to grow meaningfully from that base. Also some areas of discretionary spending—such as footwear— are likely to see slower growth this year, at least according research by ConsumerWise.

I think margins will continue to expand a bit after taking a dip from their acquisition. It’s hard to assign a multiple because it’s hard to predict how fast the company will grow over the coming years but I’m assuming low growth (5% - 10%) and multiples no bigger than 15.

Final thoughts

I’m always tempted by low P/E ratios and high FCF yields because I love a good deal. I usually like to hold for the long term and with this company its very hard for me to discern whether they will be around in 10 years + growing their brand. A bull thesis for Crocs must necessarily include an argument defending their long term brand and I’m not confident in my ability to do that at this point.

It’s nice to own a company that is cheap and generating a lot of cash, but it’s even nicer to own a company that can generate high returns on capital for the long term. I’m not saying they aren’t capable of doing that, but as of right now don’t feel confident making that call. For now I’ll watch the company and continue learning about them.

Thanks for reading!