Dream Finders Homes. A dreamy company in a tough market.

$DFH

Company Information

Market cap: $2.9 billion

Revenue: $3.7 billion

Earnings: $296

P/E: 11x

Foreward P/E: 10x

ROE: 31%

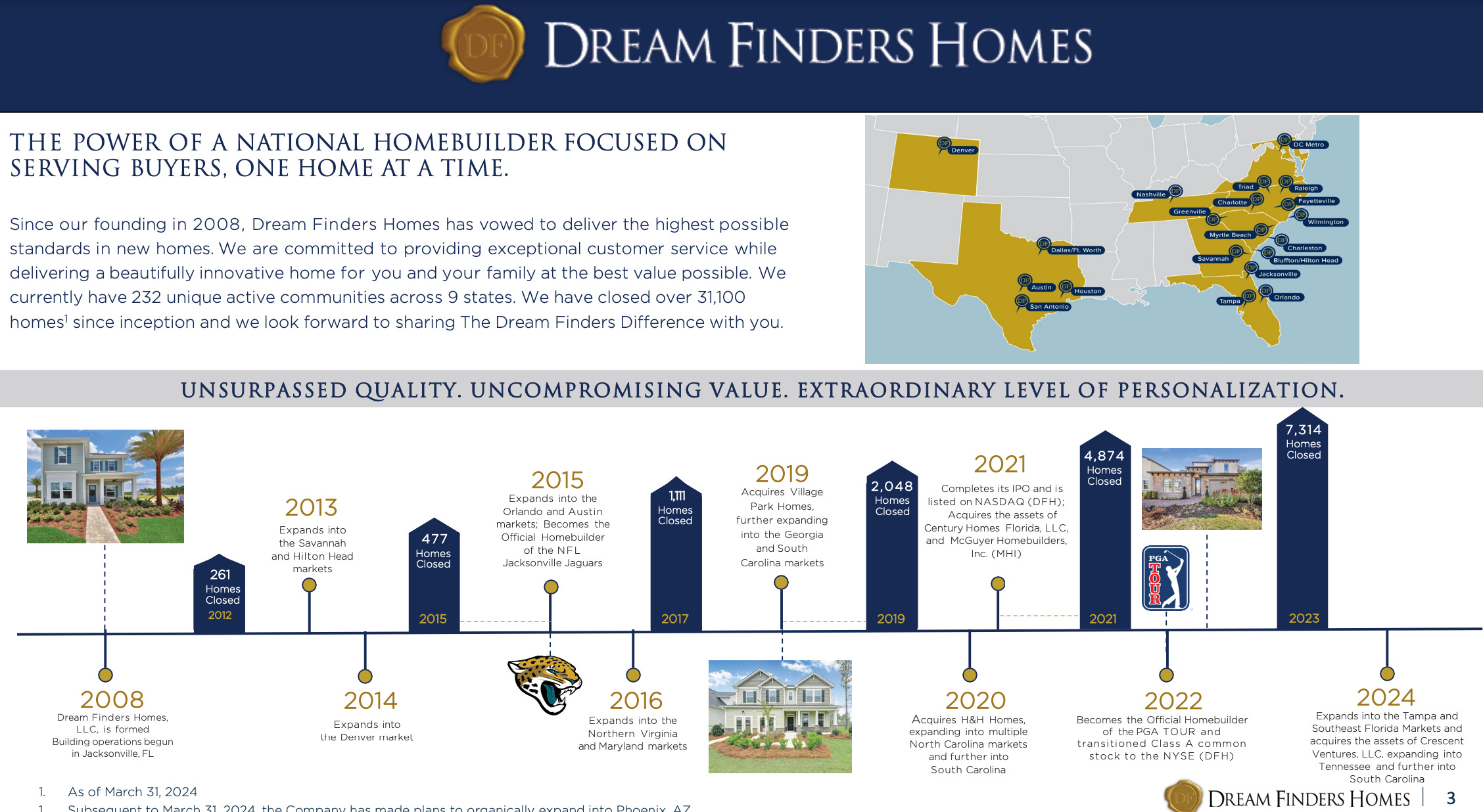

Dream Finders Homes

I’ve written about Dream Finders Homes a few time before, you can find my most recent article here. I opened a small position in $DFH at around $10 a share in 2022, then continued to add at various prices between $15-$33.

Dream Finders Homes operates a land light home building platform primarily in the southeast United states. Before I get into “land light” building and all the things I like about this company, I want to briefly go over the housing market.

Overview of the housing market

The 2 years following covid were abnormally good for the US housing market. Mortgage rates plummeted below 3% and people began moving and re-locating in what seemed like a frenzy. However, as the fed aggressively raised rates to tamper inflation, mortgage rates made their way up to around 7% in a very short time span. Many predicted carnage in the housing market, causing home builders to sell off. Although it’s true the housing market more broadly has slowed down for, judgment day hasn’t arrived for home builders…yet.

New housing starts (new homes being built) haven’t completely crashed but rather reverted back to a pre-pandemic trajectory. While housing prices have indeed fallen in certain cities around the country, they’ve also continued to climb in others. Here in San Diego where I live, prices have become unbearably high ($1,021,655 on average). Much of this simply has to do with supply demand dynamics.

In my last article on $DFH I explained the key forces at work that are causing this strange behavior.

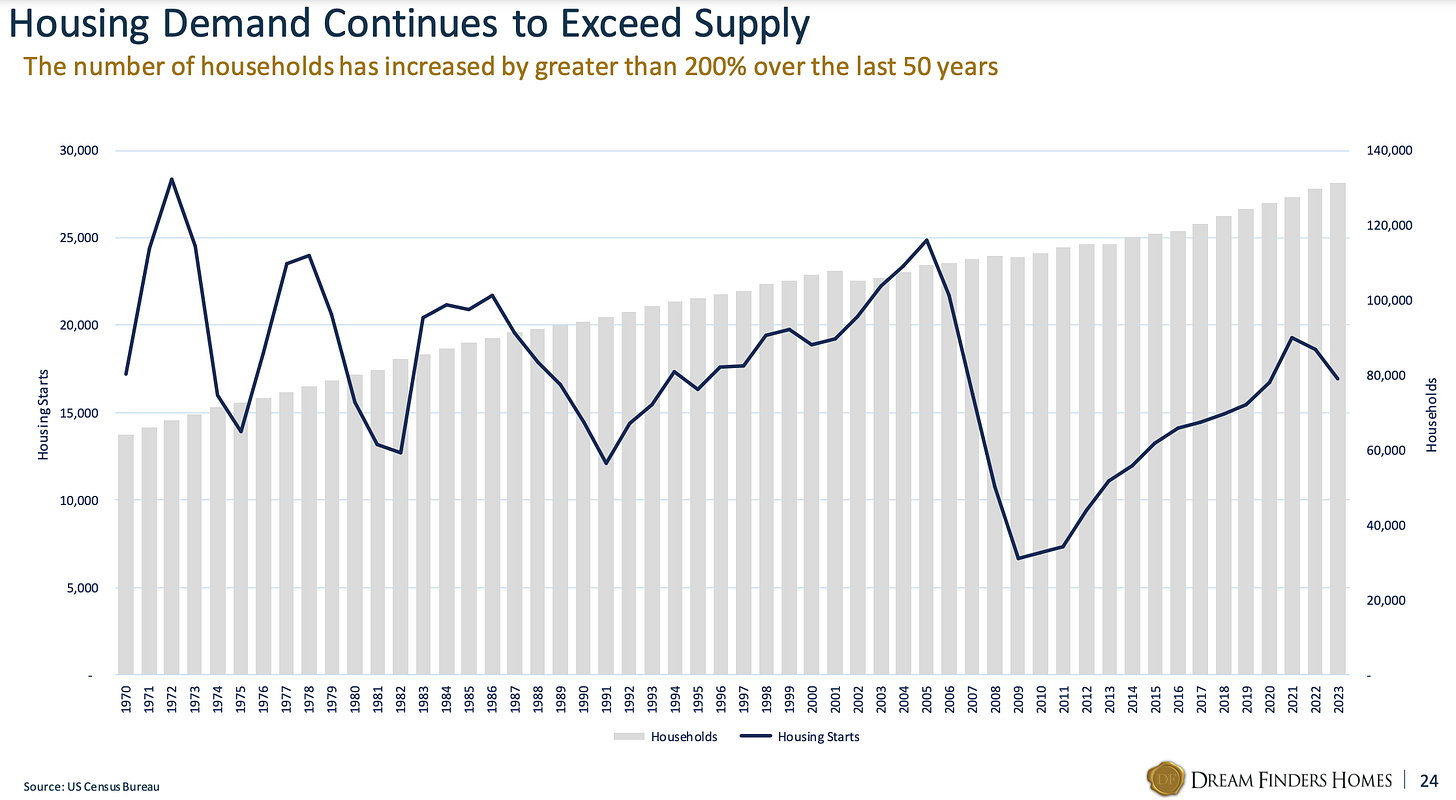

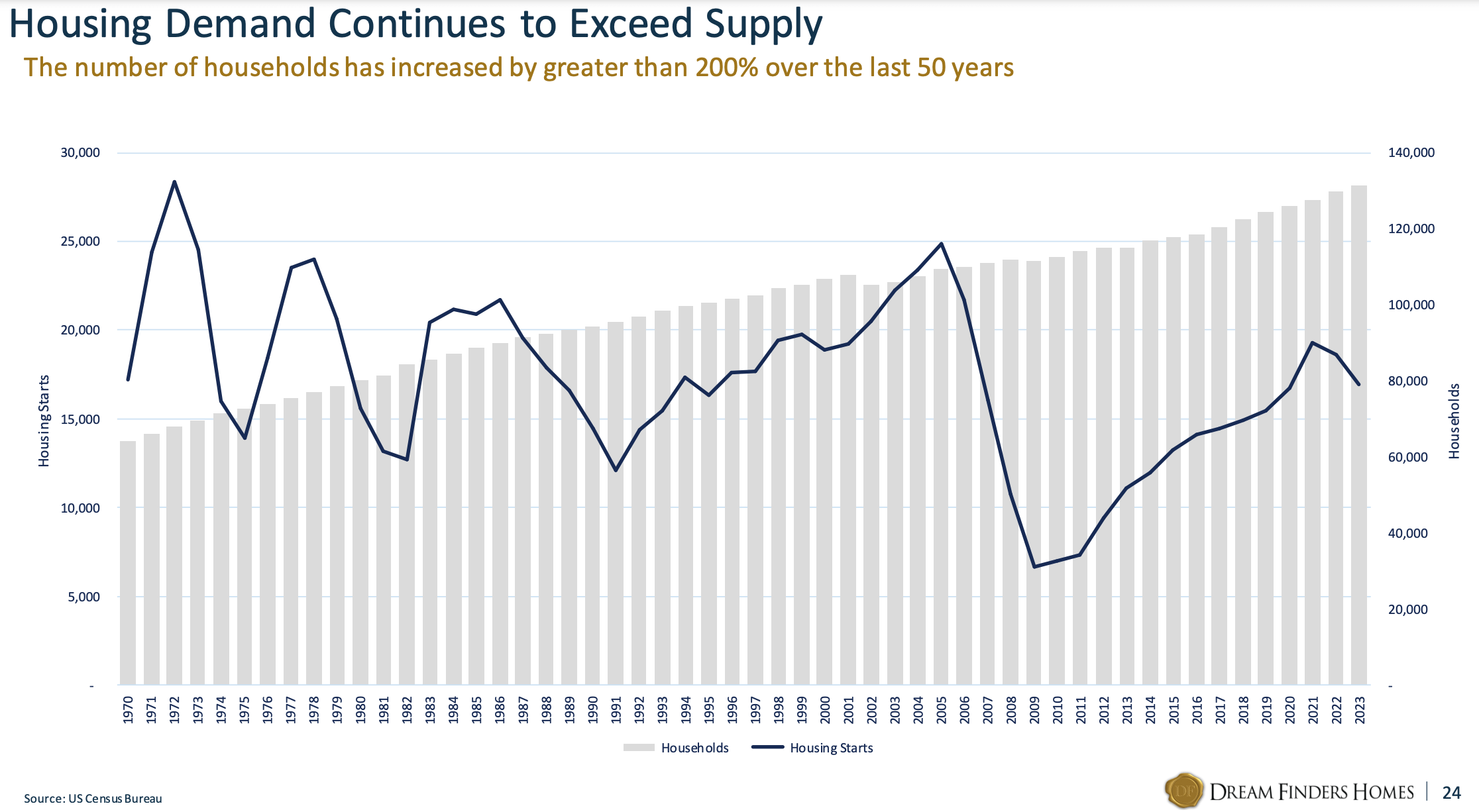

Under-built housing market: Since the great financial crisis the United States has not produced a sufficient supply of new homes to meet the new housing formations. We now have a housing shortage to the tune of a few million.

Lack of skilled labor: During the GFC a lot of companies went bankrupt or skilled laborers left the industry in search of more steady work. The lack of builders and laborers put pressure on production capacity and compounded the supply problems.

Low inventory: A lot of people have been the beneficiaries of very low rates, picking up favorable mortgage rates over the last 15 years. Moving would require them to part ways with those rates and pick up much higher rates. This has incentivized many people to stay where they are and its also decreased home inventories available for sale.

These have forced buyers into the new housing market as there really isn’t an alternative. I’m not sure how the inventory problem will play out but I imagine it will eventually normalize if rates go down. However, the housing supply problem is likely going to be long term, which should turn out to be good for home builders as home prices remain elevated and demand remains stable. The reason this is a long term problem is because of the massive skilled labor needed to solve it, skilled labor that isn’t necessarily there.

The lack of skilled labor is partially due to the false perception that construction is hard, low paying work for red necks and country blumkins. Trust me, as a contractor this is exactly what we prefer everyone to think this because it keeps people out of the trades and limits our competition. Regardless, it’s not true.

I suspect when men finally get over their obsession with air conditioning and Herman Miller office chairs, they may realize that licensed plumbers and electricians can get rich too, without the cubicle, bosses and student loans. Until then the skilled labor shortage will probably persist.

Dreamy returns

Historically home building has been a mediocre businesses because it’s capital intensive and front loaded with large variable costs. Not to mention, the combination of a recession, falling prices, leverage and land inventory have historically been a recipe for disaster. It wasn’t until after the great financial crisis that many builders really began to change the way they operate, increasingly modeling themselves after NVR, who pioneered the land light strategy.

Land light

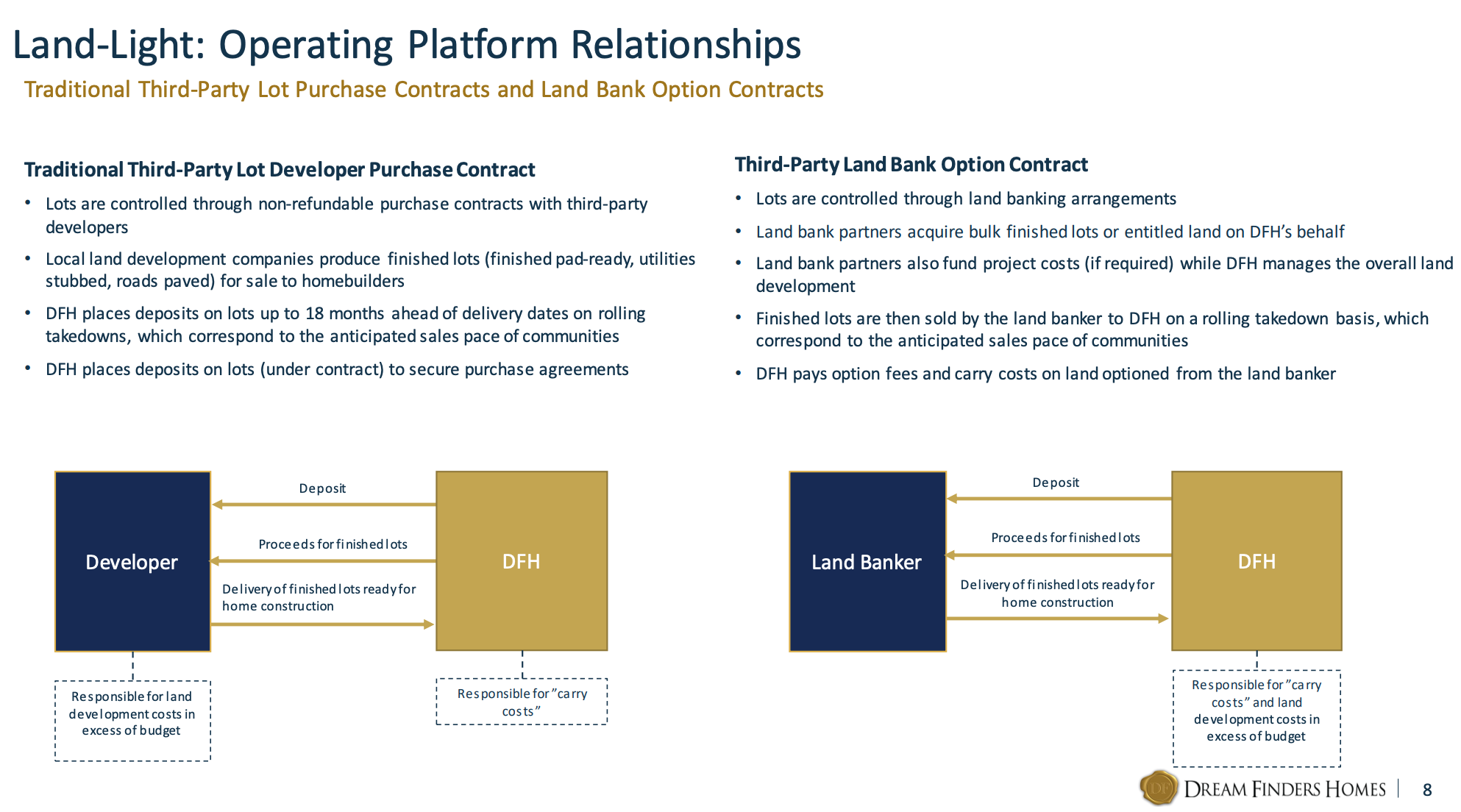

If you were a home builder, the traditional way to build homes would be to buy a large plot of land, develop it, build and then build your home on spec or sell them before building. Spec is simply where you build the home before selling it. Either scenario requires a large upfront investment in land of which you probably wouldn’t see a return for at least a few years.

The other way is to outsource the entire development process to a third party such as a land bank or land developer. The third party prepares or manages finished lots for you until you’re ready to build. This of course will cost you a small fee, but it also gives you the right to not purchase the land for any reason, which is beneficial in tough economic environments.

The tradeoff between the two strategies is one of sovereignty and flexibility. Direct land ownership affords you more sovereignty over the entire development process while land light afford you the flexibility of having more cash, less risk and higher returns on capital.

It’s a difficult trade off to juggle but ultimately the the land light model has proven to produce superior returns for shareholders and that’s the general direction of the entire industry.

The two ways that DFH goes about this is through purchase contracts with developers and option contracts with land banks. The main difference between the two is that the purchase contracts are more simplified and require less money and time on DFH’s part. They simply pay an option fee and the finished lots are delivered to them as they sell homes. On the other hand, when a land seller doesn’t want to deal with the land development process, DFH will enter into an agreement with land bank partners, who acquire land for them to be developed by a third party contractor, which is overseen and managed by DFH. In this case land is being acquired on behalf of DFH according to their budget, therefore they’re liable to pay any development costs that exceed that budget. Either way, both methods reduce the risks of land development and holding large quantities of land inventory.

Modeled after a king

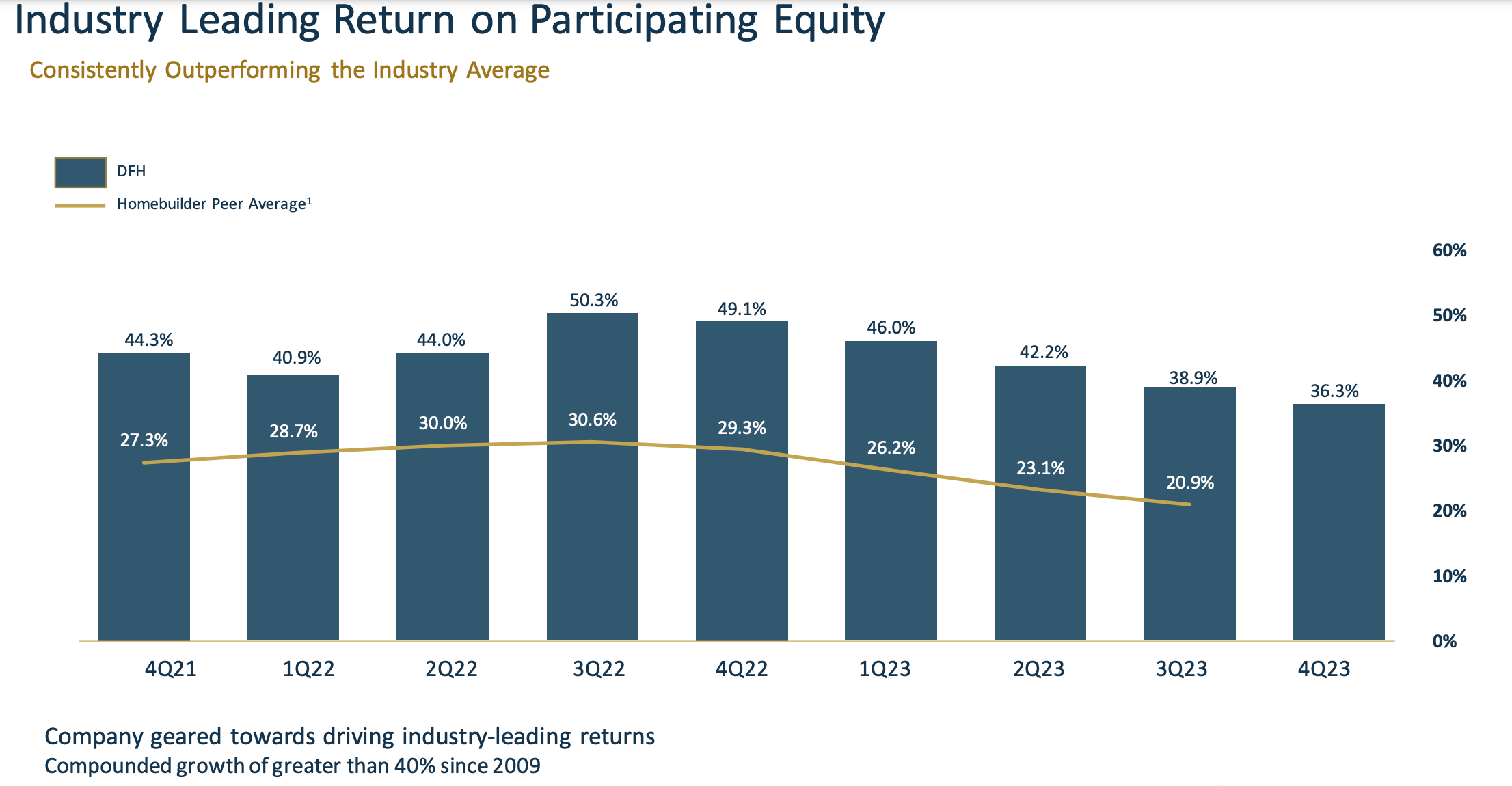

It’s no secret that NVR’s 100% land light model has proven to be superior as they’ve averaged a return on equity of about 38% over the last decade. Compare this to DR Horton at 17% and Pulte Group at 21%. Over time, NVR’s superior results have encouraged many others to follow suit. Home builders have increasingly controlled land via land options and lot purchase agreements rather than raw land acquisition. Dream Finders however has modeled itself after NVR, utilizing the land light model 100%— earning an industry leading ROE much higher than peers.

DFH’s Opportunity

Like I mentioned at the beginning of this post, part of Dream Finders opportunity lies in the supply demand imbalance in the market. On one hand, the demand for housing has been climbing as millennials reach the peak buying age. On the other hand there isn’t enough homes being built each year to service the new demand. This should continue to be bullish for home builders.

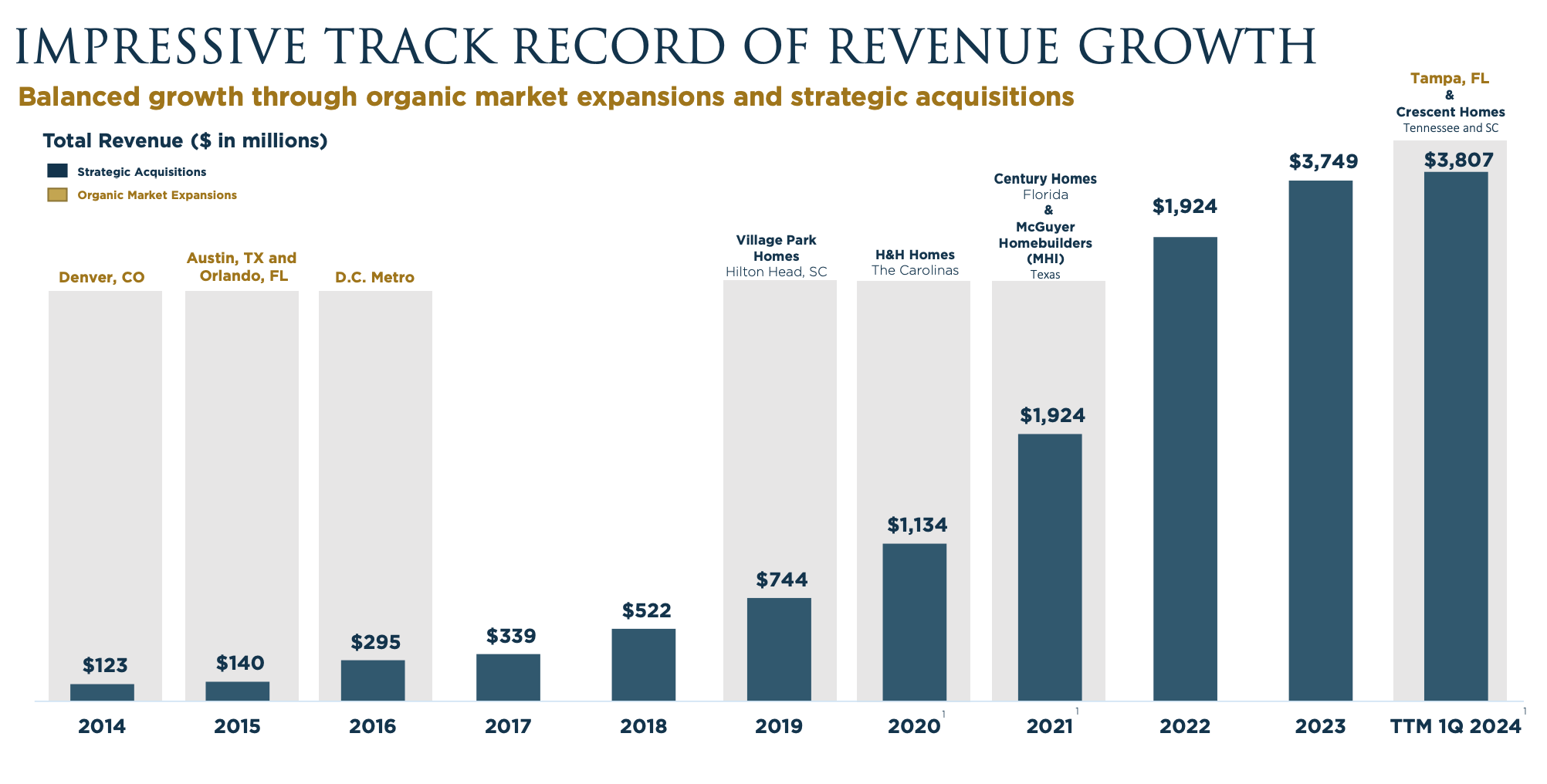

Acquisition

I also believe there could be a good opportunity for them to grow through acquisition. Which they’ve done quite well already.

For home builders acquisitions can be a great use of capital at the right price. They allow builders to acquire smaller firms who may not be as efficient, often times at very attractive multiples (5-10x earnings or less than 1x sales) as you’ll see in a minute in the capital allocation section.

Dream Finders has a knack for spotting good acquisition opportunities, particularly in growing markets. They’ve made a few acquisitions since they went public and they’ve worked out very well and rewarded shareholders.

I couldn’t get a precise figure, but in my estimation there are many dozens of builders that would fit the acquisition criteria for Dream Finders. Theres a few hundred thousand home builders in the US, most of which are in Florida and Texas, DFH biggest markets.

Here’s a list of the top 200 builders in Southern US. Obviously many of the top names such as DR Horton and Lennar are off the table, but there are plenty of smaller builders that could be acquired.

Skin in the game

I’m a huge fan of Patrick Zulupki’s and I recommend that everyone read his annual shareholder letters. They are clear, simple and provide insight into the business for shareholders. He writes as an owner to owners, some of whom also happen to be family and friends who have their money invested in DFH 0.00%↑ .

“We have a lot of friends and family that have entrusted us with their hard-earned dollars, who are not necessarily financial experts, and we want to make sure everyone understands what they own and why we believe we are uniquely positioned for long-term success.”

He also personally owns 65% of the company which essentially accounts for his entire net worth tied up in the stock. This is impressive to say the least and truly shows how committed he is to the long term health on the company.

There is no greater alignment of interests than the fact that your Founder, CEO and Chairman owns approximately 65% of outstanding shares. Over 99% of my net worth is invested directly in this company that I founded and have managed for 14 years.

Like I said in my previous post, the only way to hold a captain accountable to the rest of the ship is to make sure he shares in the successes or failures of that ship. A CEO with a large stake in the company will naturally consider the long term health of the company while navigating the markets. This is how incentives work, it’s human nature and nature remains undefeated.

Capital allocation

Dream Finders capital allocation program is fairly simple. They use cash flows primarily to secure finished lots for future operations and expand into new markets (organically or through targeted M&A). Then they pay down debts and consider buybacks.

I want to take a minute to zero in on their acquisition history.

Between 2019 and 2021 they acquired the following home builders and expanded into the correlated markets

2019 - Village Park Homes, LLC Hilton Head and Bluffton, South Carolina markets

2020 - H&H Constructors, Entered multiple markets in North Carolina (Charlotte, Fayetteville, Raleigh, Piedmont Triad Wilmington) and Myrtle Beach, South Carolina.

2021 - Century Homes Florida, LLC, Expanded market share in Orlando, Florida

2021 - McGuyer Homebuilders, Inc, Increased operations in Austin Texas and expanded into Houston, Dallas and San Antonio, Texas markets.

2024 - Crescent Homes, Charleston SC and Nashville Tennessee

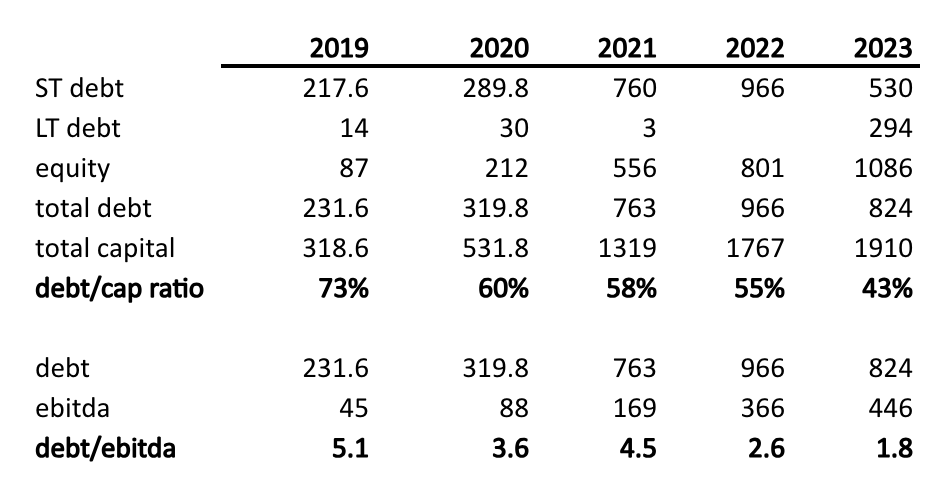

Dream Finders levered up heavily to acquire some of these companies and their assets. They experienced better than expected results and were able to pay down a substantial portion of their debt almost immediately. They were highly levered in 2019 and subsequently reduced their debt/capital ratio from 73% to 43% between 2019-2023 and saw their debt/EBITDA ratio plummet from 5.1 down to 1.8 in that same period. They did this while compounding their bottom line at 65% and authorizing a small buyback program ($25 million.)

The buyback program was small and immaterial but whats important is that they signified a sense of allocation discipline and stewardship to shareholders. It appears their priorities are in line with shareholders and so far I’m happy with their capital allocation. It’s obvious that Patrick runs the company like an owner.

Crescent Homes case study

In each acquisition there are certain things to consider. First, the companies inventory items such as construction in process (CIP), owned land, finished lots, and finished homes. The acquisition price will usually reflect some combination of the these, but the most important contributing factor is usually CIP and finished homes because they will produce cash flow in the near term. However finished lots and land is also valuable for future operations and will contribute to the over all price of the acquisition as well.

Dream Finders acquired Crescent Homes for $185 million and it came with some homes under construction and some sold homes.

“Assets acquired include 457 home sites in different stages of construction, and a backlog of approximately 460 sold homes valued in excess of $265 million. Additionally, the Company expects to control approximately 6,200 lots as a result of the transaction.”

So they acquired 457 homes under construction and 460 sold homes with a value of 265 million. From this we can deduce that Crescent Homes has an average selling price of somewhere around $576k ($265 million/460 = $576K). So for all 917 (457 CIP + 460 sold) I’m going to assume a conservative ASP of $550k. So from this we may be able to deduce that DFH acquired 917 homes with market value of about $504 million ($550k x 917 = $504 million). This represents a P/S of roughly 0.36x. Its hard to get data on acquisitions but from what I’ve researched it appears the average P/S for acquisitions is around 0.5x - 0.6x sales.

If we throw a conservative profit margin on there— say 5-7%— (most builders are 10% + right now) we get potential earnings of around $25-$35 million on a $185 million acquisition, which is a P/E of around 5-7x. Obviously these number could be a little different in reality but I feel confident that they’re at least somewhere in the ball park, which is great. On top of that they gained control over 6,200 lots! This is a great acquisition in my opinion.

Risks

The risk of owning DFH are similar to most any other home builders. I think theres a few things to consider, starting with the obvious.

Interest rates and cyclicality

It’s no secret that construction is cyclical and largely driven by employment levels, consumer confidence and interest rates. When the economy isn’t doing so well, home builders are the first to get squeezed. Land heavy builders typically carry inventory risks and incur larger inventory impairments during recessions. DR Horton for example, incurred almost $2.5 billion in inventory impairments and losses from land options fees in 2008.

Dream Finders on the other hand, wouldn’t theoretically incur such extreme impairments during a recession because they don’t own as much land on their balance sheet. However, regardless of this clear benefit, they would still have to forfeit the cost of the lot options they don’t exercise and suffer the inescapable revenue declines, margin compression and lower returns on capital that accompany recessions.

Competition

Home building is a competitive industry but not in the way you might first assume. Most most builders sell comparable homes with similar craftsmanship so they’re somewhat commoditized. What buyers really care about is the location. This inevitably means that builders are competing primarily for control over quality land (lots). Controlling quality land is the necessary precondition for selling homes. So their business will suffer if they don’t continue to successfully compete for an ever increasing quantity of land at reasonable prices.

They must also compete for skilled site management and labor. As I mentioned earlier, labor is in short supply and quality construction managers know their value and will go wherever they are treated best and sometimes bigger construction firms have the ability to offer more benefits. If DFH can’t retain quality subcontractors and project managers it could be a problem for DFH.

Valuation

Estimating the growth of a home builder in a macro environment like this is tough. A lot of us—including me— were wrong when we though higher rates would decimate the housing market and yet demand for new homes persisted. One could reasonably assume the housing market could potentially suffer temporarily. Dream Finders just reported slower growth in Q1 2024 of around 8% yoy which could confirm this assumption. However, I have more confidence that home builders will be very busy over the longer term.

I’m assigning modest growth over the next few years (7-12%) and a multiple between 10x-14x which is normal for land light builders like NVR 0.00%↑ and DFH 0.00%↑ . My base case is about 10% growth and a multiple around 11x.

Final thoughts

I really like Dream Finders Homes and admire the founder. I recently increased my DFH 0.00%↑ position around $33 and again at $31, but not significantly. It’s not quite within my sweet spot. I’d be far more excited to buy the stock around $25. At that point I’d consider making it a much larger position, but for now I’m not adding any more.

Thats it until next time, thanks for reading! Consider subscribing if you haven’t already!

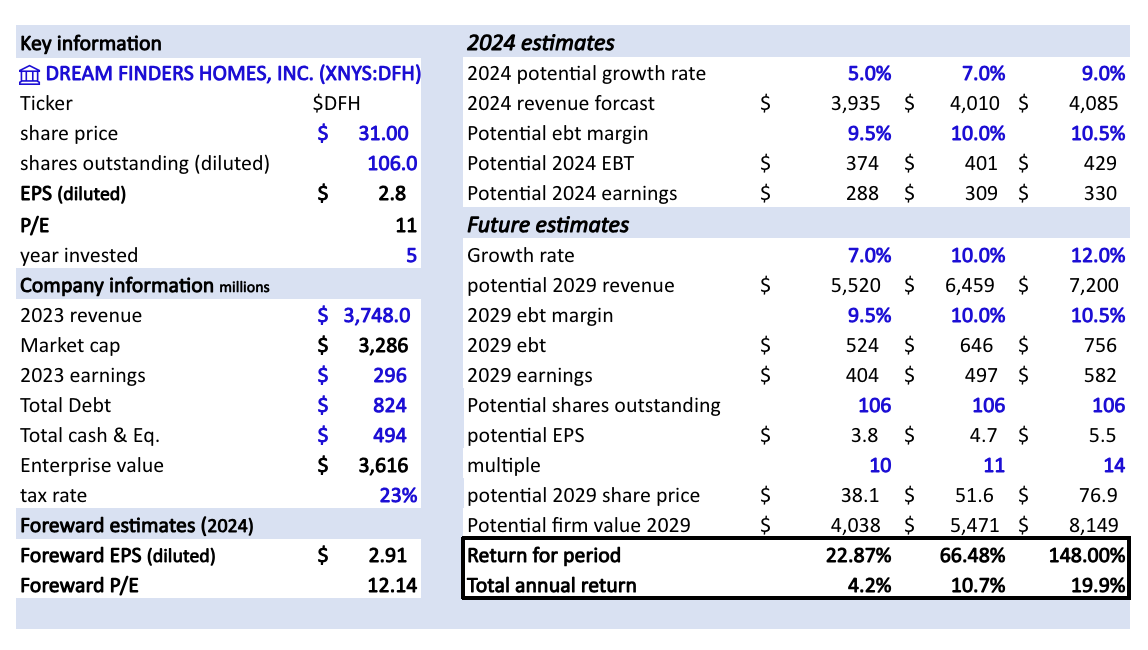

Hey there, thanks for the great writeup. I'm going over your numbers for your model and am not able to confirm you Forward PE of 12.14. Based on the cal for forward EPS, I'd assume you use 31/2.91 = 10.64 as opposed to 12.14 in your calculations.

I also tried to recreate your forecasted revenue, using either 2023 revenues as a base or 2024 forecast as a base and applying your growth rate. For example, if I start with $3,935 and grow this at 7% pa, I get $5,158.5 by year 5. If I use 2023's $3,748 as a base and grow that at 7% pa instead and ignore the 2024 forecast, I get $5,256.8 which is still below your 2029 forecast.

I'm also unable to reconcile your expected firm value in 2029. If I assume $38.1 sp and 106 s/o, and cash/debt are constant, I get $4,367.8

Please advise on where my calculations may be incorrect

Thank you for the clear writeup. A lot of things to like, but do you know why the Return on participating equite fall a lot this quarter?

Also, margins are not as good as NVRs. Do you expect that to change as they get bigger?

Thank you.