Quality companies like NVR 0.00%↑ have been a long time favorite of value investors for a long time. NVR is a home builder that’s in a league of its own, they generate high returns on capital, they don’t keep a bunch of risky land on their balance sheet, they buy back tons of stock, and they minimize leverage. What more could you want? At the end of the day they’ve been great capital allocators and shareholders have been rewarded because of it.

DFH 0.00%↑ is a newer home builder that claims to have studied NVR and modeled their business after them. So the questions is why has NVR done done so well? and is Dream Finders Homes really the next NVR? or just a wannabe copycat?

Dream Finders Homes

In their 2022 annual report DFH describe’s their business like this

“We design, build and sell homes in high-growth markets, including Charlotte, Raleigh, Jacksonville, Orlando, Denver, the Washington D.C. metropolitan area, Austin, Dallas and Houston. We sell homes under the Dream Finders Homes, DF Luxury, Craft Homes and Coventry Homes brands. We employ an asset-light land acquisition strategy with a focus on the design, construction and sale of single-family entry-level, first-time move-up and second-time move-up homes”

Before I explain asset light building, I think it’s important to understand the reasons it was pioneered in the first place. It was developed to solve some of the most common problems in home building

The difficulty of land acquisition and development.

Supply and demand fluctuations in the real estate market.

Having to take on large amounts of leverage.

At a basic level new home building is a commodity business. You are essentially building an asset and selling it on the free market. If you’re a builder your cost of land and labor needs to be sufficiently lower that your sale price in order to produce a profit. Now there are a few different ways to do this, and one very common way is to buy a bunch of land at a price that is low enough to allow you to, develop it, build and sell the homes at a profit. In order to do this large amounts of undeveloped land must be purchased at a discount, then rapidly developed into lots and homes to be sold.

Land development

Land development is the process of taking raw land and converting it into buildable land. This includes removal of brush, trees and rocks from the soil, drawing electricity and water into the buildable lots and finally grading (leveling) and compacting the soil to prevent finished homes from settling.

This is a time consuming and expensive process and if large builders want to keep operations running smoothly, they must buy large plots of land to supply them for multiple years into the future. In construction the key to success is finishing projects quickly and minimizing the time between the first and last day of a project. Land development makes this difficult and therefore risky.

Demand fluctuations and leverage

I’ll give you and example of some other problems you could run into if you were a home builder. Let’s say you borrowed some money, bought some land then you began to develop and build on it. Then the economy slows down and demand for housing plummets and housing prices begin to soften. There are basically two things you can do at this point

Sell off and write down your inventory (land & homes) at a discount just to get rid of it. Which could result in either a loss or low return on investment.

Attempt to hold your inventory until housing demand come’s back, which can be disastrous if you’re leveraged because you’ll still be making payments to the bank in the mean time. This is a recipe for bankruptcy.

The asset light model used by NVR and DFH is able to mitigate these risks through the use of land options. They essentially find the land and pass it off to a land bank who owns/develops for them. They enter into option agreements that give them the right to incrementally purchase the land on a set schedule, which they only do once they have sold a home and collected a down payment. So the entire process of buying land and building a home doesn’t happen until they have a committed customer. The goal of this entire process is to avoid borrowing large amounts of money to buy large amounts of land at any one time.

This means lower inventory risk because they don’t have a ton of land on their balance sheet, which means they have lower working capital requirements and more cash on their balance sheet. The end result is higher returns on tangible capital and higher returns on equity.

How does Dream Finders compare?

Comparing DFH and NVR is probably unfair because DFH is newer and a less mature business while NVR had decades to perfect its operating model. DFH on the other hand is the new kid on the block attempting to prove itself.

Regardless, one notable difference between the two builders, other than size, is the geographic location in which they operate. NVR is the dominant builder in Washington DC and derives 21% of its revenue from that market alone. They also operate in Maryland, Virginia, West Virginia, Delaware and Washington, D.C. New Jersey and Eastern Pennsylvania New York, Ohio, Western Pennsylvania, Indiana and Illinois North Carolina, South Carolina, Tennessee, Florida and Georgia

Although NVR is in some high growth markets, DFH is a lot more exposed to high growth markets such as Jacksonville Florida, Charlotte north Carolina, Austin Texas, Orlando Florida, Raleigh North Carolina, according to rocket mortgage these are some of the strongest growing markets right now. DFH biggest markets are currently Austin, Texas and Jacksonville Florida which are much stronger growth markets right now compared to NVR’s Washington D.C. This explains why NVR’s recent quarterly revenue was down almost 8% year over year

While DFH revenue is still cruising along growing revenue at 15.8%

Although DFH has seen a 26% cancelation rate and a lower backlog order, they are still projected to have a backlog of almost 2.7 billion and the average sale price of their homes have continued to increase due to large amounts of demand in the areas they operate.

In their most recent annual report they stated that demand in the housing market has stabilized regardless of rising mortgage rates. Another thing that’s surprising is they said that their current cancelation rates are now within pre-pandemic historical levels and that 2022 was actually an anomaly because of favorable economic conditions.

Management

Patrick O. Zalupski is the founder, president and CEO of Dream Finders Homes. He has a background in finance and he basically built the company from the ground up, closing just 27 homes in 2009 and currently closing over 22k homes. It’s impressive how quickly this company has scaled and I suspect its in large part due to his involvement in the founding and his financial background. However, In order to make any kind of judgment on his capital allocation skills it would be wise to look at the recent big acquisition.

In 2021 DFH acquired the Austin Texas based MHI McGuyer homes for $583 million. MHI McGuyer is one of the biggest private home builders in Texas. According to builderonline.com MHI McGuyers revenue was 931 million in in 2020, which was a year before DFH acquired them. I can only speculate what MHI McGuyers revenue was a year later when they were acquired but almost all home builders had a blowout year in 2021, most had revenue growth above 20%. Even though MHI McGuyer operates in one of the hottest real estate markets, I’m going to conservatively estimate they only grew revenue by 10% which would be just over a billion in revenue. I can only speculate their margins as well, but we can assume they are in the 6-12% range which is normal for home builders. Im going to assume 7% just. That would be $71 million in earnings, which means they could have paid 8x earnings for a dominant home builder in Texas. Im fairly confident MHI McGuyer had higher earnings and DFH ended up paying a lower multiple but even still, 8x earnings is an excellent price for a dominant builder in one of the hottest real estate markets in the U.S.

DFH also announced a share repurchase program of $25 million which is not very impressive at all considering their market cap is 2.4 billion but it’s a step in the right direction, showing their commitment to shareholder value. At the end of the day it’s not about earnings growth, it’s about earning per share growth.

Patrick also owns a massive position in the company. A whopping 84.8%

Needless to say his entire net worth is wrapped up in the performance of this company.

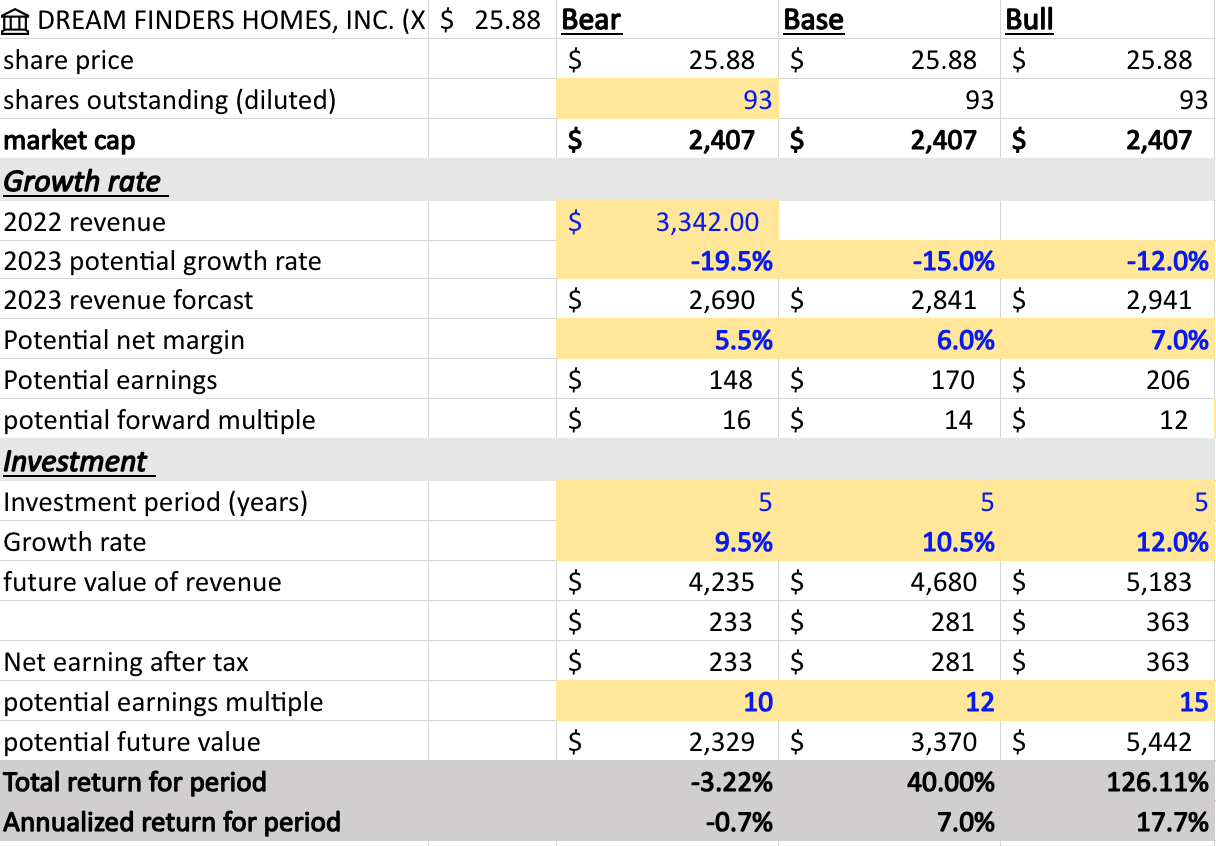

Valuation

In full disclosure I am a shareholder of DFH 0.00%↑ with and average of 11.63 per share. It’s been a good investment for me because I bought during the sell off. I originally got in at like 12-14$ and then bough more when it dipped down to 9$. They have certainly been on a rip this year.

The only guidance they give us is that they maintain they are on track to sell 6,000 homes. this year, in which they currently have 5,479 on backlog. Their average price of homes sold is $490k. So Im assuming they will sell between 5,470 and 6,000 homes this year and have revenue somewhere in the 2.6-2.9 billion range. Future growth rate is a little difficult to predict because it’s highly dependent on interest rates. I’m assuming rates will remain higher for at least another year and then rates will drop and growth will pick up. I think a 9-12% growth rate is reasonable for a home builder situated in high growth markets. I do think this company deserves a higher multiple especially if they can execute the asset light model like NVR has. I think an end multiple of 10-15x is appropriate seeing as how this is the multiple that NVR frequently has.

With that being said I really do want to own more of this company but I do think home builders are fully priced considering home sales are slowing down. Im hoping the home builders sell off because if DFH dips down below 20$ Im going to increase my position significantly. That would skew the return closer to 200% on my bull case.

Notes on the market

Im a general contractor and I can say there has been a slow down in the housing market and building in general, but not every area of construction has slowed down. New home construction is still upbeat and moving right along in some places. There is a limited supply of existing homes for sale because so many people locked in such low rates the last few years that they are not willing to part with them. This essentially shifted remaining demand over to the new housing market.

Could it last? I don’t know, if rate continues to go up people will eventually stop buying new homes. But time will tell. Regardless DFH is on my list of stocks to buy more of.