Tasmea

An industrial services compounder

Key details

Ticker: $TEA.AX

Share price: AUD $3.69

Market cap: AUD $957m (USD $662)

Net profit after tax(2026 guide): AUD $70m

Forward P/E: 13.7

Net debt: AUD $110m

2 minute summary

Tasmea is an Australian specialist services consolidator focused on keeping essential industrial assets running. Insiders own 60% of the company and management has demonstrated disciplined cash flow management and the ability to reinvest at high rates over the last few years. 94% of revenue is generated from repeat, blue-chip customers, and 80% is considered stable and resilient. Revenue has grown rapidly since 2021 (34% CAGR). Even more impressive is that earnings (NPAT) have grown at a 52% annually in that same period. Despite all this, the company is down 30% from the highs due to acquisition related risks and skepticism of the Australian resources sector.

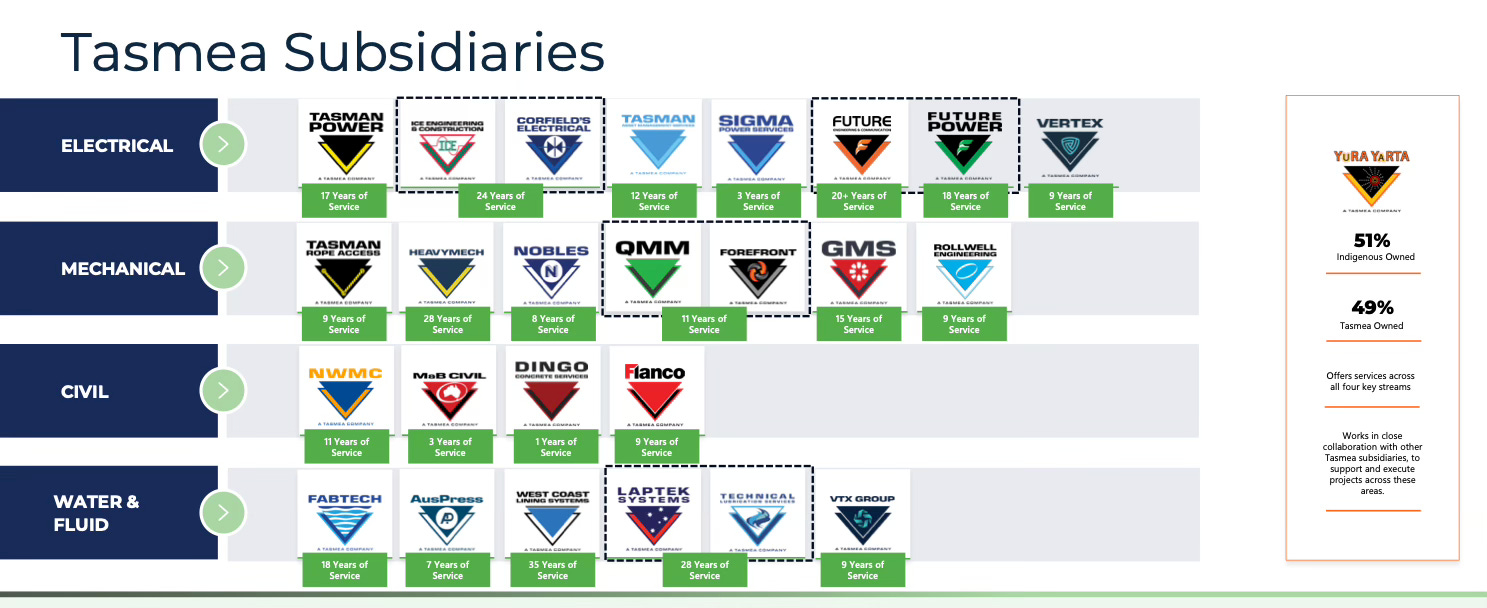

Tasmea currently owns 25+ specialist trade businesses that provide various essential services such as shutdowns and programmed maintenance, brownfield upgrades, and breakdown and repair. Tasmea’s end markets include mining, energy, and infrastructure. Although end markets can be somewhat cyclical, the company is less cyclical than one would expect and it is exposed to long duration tailwinds such as electrification and grid upgrades, renewable integration and transmission, aging infrastructure, and skilled labour shortages.

The company also scales much better than one would think as it’s able to cross-sell services and bundle electrical + mechanical + civil + labour. That means more wallet share per customer and higher margins as it grows. This explains why earnings have grown so much faster than revenue.

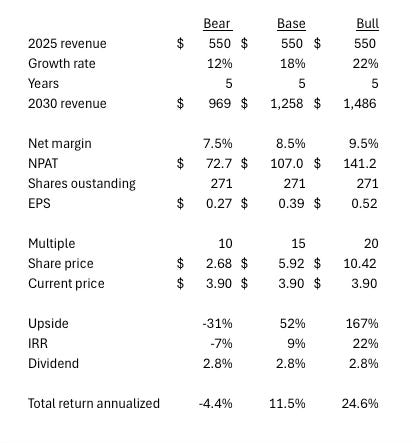

Upside over the next 5 years largely depends on management’s execution and industry dynamics, with a worst case scenario yielding a negative return and a bull case of scenario of around ~170%+.

Business model

The company is less cyclical for a few reasons. First, the model is oriented towards maintenance and uptime maximization, drawing much of its revenue from the operating expenditures rather than CapEx of its customers. Operations are largely centered around non-discretionary activities tied to safety and regulatory compliance, in other words, keeping the old assets running, which must be done even in down seasons.

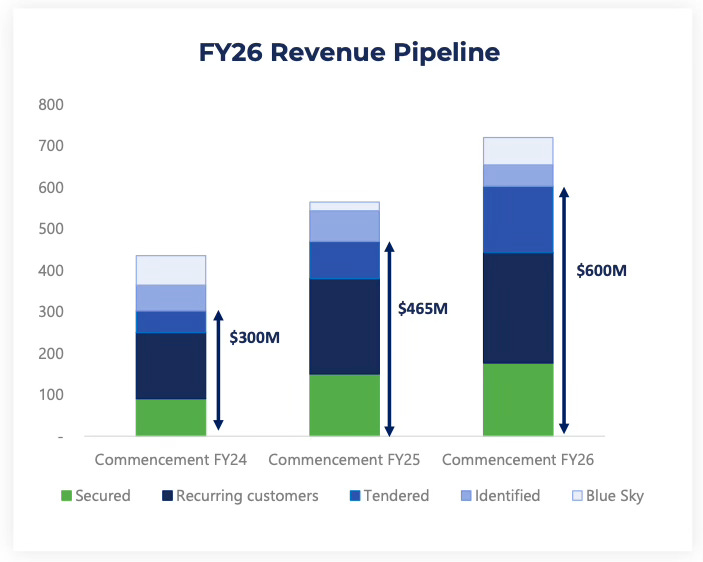

Second, a large proportion of work is secured under Master Service Agreements (MSA) and Facilities Management Agreements (FMA). FY26 opening order book is at ~$600m with strong visibility, providing a predictable pipeline of work.

Lastly, when prices fall, volumes can rise, which means assets run harder, and more maintenance intensity is necessary. Given al this, it’s reasonable to assumes that Tasmea behaves more like an industrial services compounder than a classic mining services cyclical.

The recent sell-off

There are a few reasons the stock is down 30%+ from the highs in November 2025.

Concerns about inevitable cyclicality in the Australian resources sector, with some saying 2026 and 2027 may see declines in export earnings.1

Share dilution and integration/complexity concerns over the WorkPac acquisition. Lets go through these one at a time;

The WorkPac acquisition made Tasmea strategically stronger but narratively messier, and markets don’t like messy. WorkPac is a scaled labour logistics platform embedded across mining, infrastructure, defense, and energy. Despite having good margins and ~96% repeat customers, the acquisition was received skeptically because it moved Tasmea from pure specialist services into labour platforms, a category many investors seemed to reflexively discount.

The rationale for the acquisition is primarily that control of labour removes the primary growth bottleneck. WorkPac allows Tasmea to bid on larger, more complex projects and shutdowns without being constrained by labour availability, while internalizing a critical input that was previously outsourced. Management also mentioned synergies and the addition of 15 master service agreements added to the portfolio.

Tasmea diluted shareholders in twice in short order. First a placement that diluted them ~4% in September to fund acquisition capacity, followed by ~2% issuance in December for the WorkPac deal. Total dilution was ~6%, but the back-to-back timing amplified market concern despite potential EPS accretion from the acquisition. If there’s one thing small cap investor don’t like its repeated equity financing.

Management

Stephen Elliott Young (founder/managing director) and Mark Vartuli (Executive Director) collectively own 60% of the company. Stephen alone owns almost 40%, worth almost ~$400 million. Interestingly, Stephen bought an addition al ~$1 million in late 2025 at $4.50 per share, signaling confidence even as the price pulled back.

Stephen and Mark have the same compensation structure;

Cash compensation

$850,000 base salary

Up to $300,000 p.a. in short term incentives.

Equity incentives

Large ownership

Long term incentive rights tied to EBIT growth and EBIT hurdle

Jason Pryde (Executive Director, Chief Operating Officer) is another key person, he owns 1.8% of equity and has a salary of $960k. He also 3 million options granted at an exercise price of $1.56 with vesting hurdle tied to EBIT growth and hurdles.

Overall, this is exactly the type of alignment and incentives I like to see. All the key directors and managers own multiple times their salary in stock, and they have long-term incentives tied to operating profit.

Risks

Cyclicality is likely the biggest risk here, although it’s hard to say exactly how this company will behave in a down season, we do know that ~40% of the groups revenue is tied to mining, and of that, ~25% is tied to iron ore mining. Management has stated that 80% of revenue is stable and resilient, but even if that is true, the other 20% is cyclical enough to put pressure on the company’s earnings in a down market. It’s worth noting, the workPac acquisition will dilute this concentration, but it still remains a real risk.

Valuation

Tasmea evaluates performance using statutory and normalized earnings (EBIT and NPAT). Management has a deliberate focus on per-share earnings and true profitability. One may notice free cash flow is lower than earnings, and while CapEx is not to blame, there are larger working capital adjustments because a portion of revenue is recognized before the cash is actually collected from the customer. This is normal for companies with long-term maintenance and infrastructure contracts where work is completed and recognized, but certain milestones must be completed in order to get paid, or in some instances an invoice is sent but customers have 30-90 days to pay. In either case, receivables and contracts assets reliably convert to cash, so the apparent cash flow drag reflects timing, not deterioration in earnings quality.

My bear case basically assumes we enter a down season and management does not execute as well as they have in the past. The bull case assumes the opposite scenario.

My assumptions are as follows

Revenue growth between 12-22% over the next five years, with a base case of 18%, which assumes maturation and less M&A intensity as the company grows. The company has grown revenue at 34% since 2021, but that’s very high for an industrial services business, and too high to sustain over the next five years, in my view.

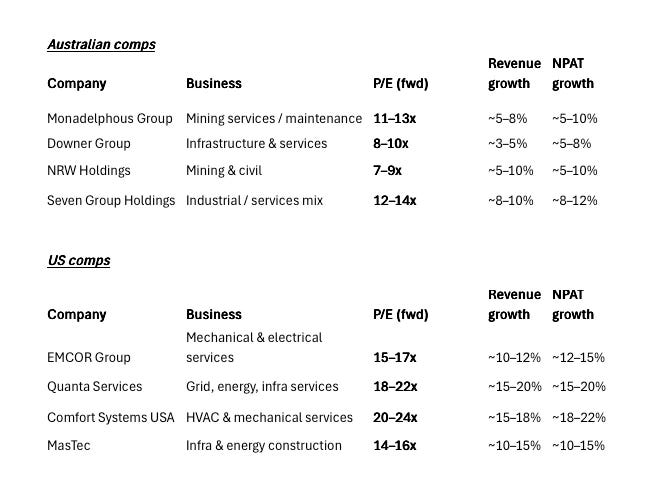

Net margin between 7.5 - 9.5%, with a base case of 8.5%. Historical margins sit within this range. Today net margin sits at 9.7%, but my base case (and Bull) assumes that today’s margins may be elevated for cyclical reasons and that 8.5% is more reasonable in a steady state, especially since the WorkPac acquisition will be margin dilutive. For more margin context, most comps have slightly lower margins but that’s because Tasmea does more specialized work that is maintenance oriented, rather than peers like Monadelphous or NRW Holdings, which take on large-scale construction (CapEx oriented) projects with thin margins. Therefore, higher Tasmea’s margins are justified in my view.

A multiple of 10-20x. Markets pay mid-teens to low-20s P/E for an industrial services company when growth is structural, and earnings compound reliably.2 The bull case could potentially be justified by continued operational execution and a slight re-rate. Base case is 15x.

Fully diluted shares of 271 million. This assumes an additional 10 million shares from equity financing, similar to those issued September 2025. Tasmea doesn’t have a pattern of habitual dilution, but I’ve baked in an additional equity raise similar to the September 2025 issue.

The base case is basically ~11% TSR if execution is solid and sentiment stays cautious, while the bull case is ~24%+ and represents a scenario where the company gets recognized as a quality compounder and execution is great. The bear case may be unreasonably pessimistic but it does represents a worst case.

Final thoughts

I don’t own this stock as of now. I am certainly interested because the growth is obvious and management is disciplined and aligned, but I have some reservations about potentially cyclical foreign stocks. Over the next few years, it will be proven whether Tasmea is truly resilient or not. For now Tasmea is on my watch list, unless it goes lower, at which time I may take a tracker position.

That’s it for this week, thank you for reading.

One thing to keep in mind is that they manage to keep original founders as CEOs for a long time. Part in due since they become co owners through dilutive acquisitions. Since all their business are in essence employment agencies (workers are not under permanent contracts) having those who ran them for years on board pays out. Also their organic growth is tied to them continuing to acquire. One of their strategies is to better utilize their employees across all their client base. On a negative side, their master service agreements do now guarantee work, but only shorten procurement when work is needed. So far they executed almost perfectly. Up to last acquisition they were just using their good working model. Let's see if they judged the latest acquisition nicely (my fear is that they have not)

Great write-up thank you.

I’m trying to better understand the extent to which Tasmea is exposed to underlying mining and energy production.

From what I can see, there seem to be two potential risk channels.

The first is lower commodity prices leading to margin pressure for producers. However, given the high fixed-cost nature of mining operations, do weaker prices materially reduce production levels?

The second risk relates to slower production growth over time due to weaker exploration activity — a point highlighted in the article you shared. That said, Tasmea’s historical growth does not appear to have been materially affected during the mining CAPEX slowdown around 2020–2021, which might suggest limited sensitivity to the investment cycle?

I’d be interested in your perspective on how meaningful both those risks are.