The science of buybacks

A primer on share repurchases

In my last article on compounding I talked about the importance of investing in companies that can produce high returns on capital. I also discussed the importance of paying a reasonable price for these companies.

In this article I want to carefully examine how share repurchases can affect a business and its shareholder returns.

Key takeaways

Share repurchases are an important part of capital allocation

Buybacks can boost intrinsic value per share

Buybacks affect financial statements in strange ways

Buybacks are only appropriate when there isn’t a better use of capital

Hypothetical 10 year analysis

An important part of capital allocation

Share repurchases can be a great use of capital but aren’t necessarily always the best use of capital, especially for companies early in their growth phase. For most companies that are trying to grow, if a dollar is earned, the ideal order of capital allocation should be as follows

Reinvest in operations and grow the core business organically

Acquire other businesses, if it creates value.

Repurchase shares

Pay dividend

If a company just went public and requires large capital investments to scale its business, share buybacks may not be the best use of capital because those dollars would find better use in simply expanding the companies operations and marketshare.

On the other hand if a more mature company has a surplus of cash and minimal organic growth ahead, It’s better to have that cash returned to owners in the form of dividends or buybacks, especially buybacks at opportune times. There’s a lot of evidence that this creates shareholder value over time.

Boosting EPS

Im assuming we all know the basic equation behind EPS. If you do hang with me for a second, If you don’t, it’s simple.

Earnings per share = (company earnings / average shares outstanding)

So increasing EPS requires either

1. Increasing the the numerator by increasing earnings or profit margins.

2. Decreasing the denominator by reducing the shares outstanding.

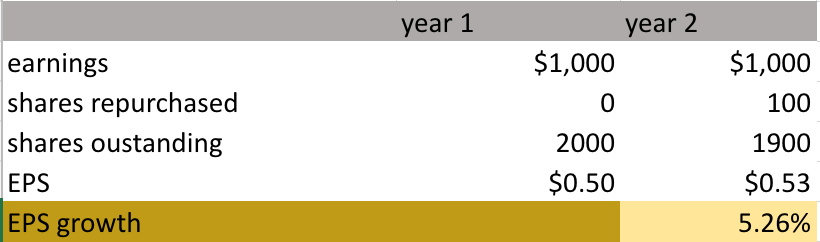

Share repurchases obviously do the latter and it does in fact increase the EPS. Below is the simplest example of EPS growth from share repurchases. Company xyz buys back 100 shares (5%) of their total shares outstanding and the result is a 5% increase in EPS. If the valuation remains the same the 5% is translated into a higher share price.

So the EPS is increased through share repurchases, but I don’t think that’s necessarily the best way to think about it. If you’re an a shareholder, your shares are essentially a claim on the future earnings from that business. Since there are less owners after the repurchase and the earnings remain the same, you as a shareholder are now entitled to a larger portion of those earnings. In other words the pie is the same size, but your slice just got bigger because it’s now cut into less, but bigger pieces. This is why Buffet loves his stake in AAPL 0.00%↑. Every year apple increases its earnings and simultaneously increases his claim on those earnings.

Affect on financial statements

I think there’s a misconception that buybacks increase the fundamental value of a business on a per share basis, but in reality it’s more complicated than that. It certainly does increases your claim on earnings and cash flows but it also potentially decreases book value of the business which isn’t necessarily good or bad in my opinion.

Let me explain.

When a business repurchases its own shares a few things happen on the balance sheet and income statement.

First and foremost there is an outflow of cash on the cash flow statement and a decrease to the cash account on the balance sheet (credit) and because of double entry accounting there must be another decrease to the equity portion of the balance sheet to keep it well…balanced. Share buybacks are recorded in a contra equity account called tresury stock which has a negative affect on equity. In simple terms, a stock buyback decreases cash, increases treasury stock, and decreases shareholders equity. This can result in lower book value and higher P/B

Secondly, shares outstanding are decreased on the bottom of income statement, resulting in higher EPS and potentially lower P/E ratio.

Heres an hypothetical example of a company with flat earnings, before and after the share repurchases are executed. This company repurchased 100 shares outstanding at $3 each for a total of $300. Obviously the EPS increased but its worth noting the book value per share decreases as the equity account shrinks.

And yet there was no fundamental change to the business besides technically shrinking shares outstanding. If you really think about what is happening here, cash is leaving the business and simply being transferred to shareholders in the form of larger corporate ownership.

But the thing to remember here is, if equity is lowered and earnings remain the same it results in a higher return on equity ROE and ROIC or depending on the calculation. The equity has been deflated allowing the earnings to catch up.

This could be suspicious if a company is intentionally trying to juice their ROE but then again, when a company has enough cash flow to buy back stock, it’s probably evidence they have a well run business that might deserve the higher ROE after all. It just depends on how you look at it.

Companies like HD 0.00%↑, DPZ 0.00%↑ and AZO 0.00%↑ come to mind. On one hand have very high ROIC and ROE partially because their equity base has been deflated. On the other hand they’re well run cash flowing machines that reward shareholders year after year.

Now, I don’t really think this is a big deal, it’s just a secondary effect of reducing the shares outstanding but it’s worth noting because it can distort certain metrics and ratios like book value per share, P/B, ROE and such.

Ok moving on before we get stuck in analysis paralysis.

When are buybacks appropriate? According to Buffet

“Unrestricted earnings should be retained only when there is a reasonable prospect, backed preferably by historical evidence or, when appropriate, by a thoughtful analysis of the future- that for every dollar retained by the corporation, at least one dollar of market value will be created for owners. This will happen only if the capital retained produces incremental earnings equal to, or above, those generally available to investors.”- Warren Buffet

“There is only one combination of facts that makes it advisable to for a company to repurchase its shares: First, the company has available funds- cash plus sensible borrowing capacity- beyond the near term needs of the business and second, finds its stock selling in the market below its intrinsic value.” -Warren Buffet

This is capital allocation in a few sentences. The first quote is actually in reference to dividends but the basic principal is relevant, earnings should be retained in the business only if the management thinks it can generate higher returns on capital than if it were paid out or used to buyback equity.

The second quote is making the ever so practical observation, as Buffet always does, that buybacks only make sense if the business has more than enough cash to satisfy its near term needs. He later defines “near term needs” more specifically as

1. Expenditures to maintain the businesses competitive position such as remodels and such.

2. Capital outlays that are expected to produce more than a dollar of value for each dollar spent. Which correlates nicely with the previous quote about retaining earnings.

So to sum up the lesson here, for every dollar a business earns they must ask these important questions.

‘Do we need this dollar to maintain the companies near term operations ?’

If not ‘can this dollar create more than a dollar if re-invested within the business ?’

or ‘will this dollar earn more in the hands of the shareholder ?’

or ‘is it more beneficial simply to increase the shareholders claim on existing earnings through buybacks’

If buybacks are chosen as the path forward then the company needs to give attention to the price of the shares being bought.

How price affects buyback returns

“When Berkshire buys stock in a company that repurchasing shares, we hope for two events: First, we have the nominal hope that the earnings of the business will increase, and second, we also hope that the stock underperforms in the market for a long time as well.”- Warren Buffet 2011 Berkshire Hathaway annual report

So repurchases are best when the stock is undervalued and the price is depressed, but the best possible scenario for shareholders, according to Buffet, is if the company’s earning grow while the stock price underperforms.

Let me explain.

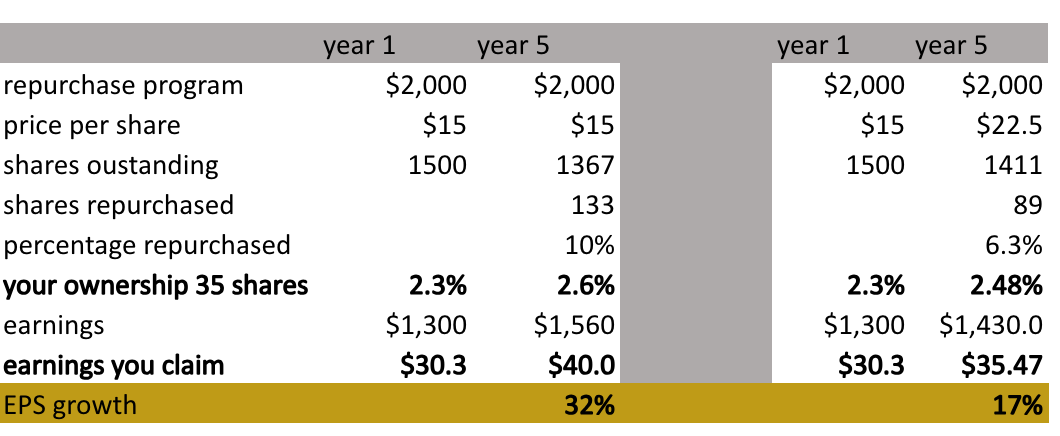

Imagine you invested in a company that just announced a stock repurchase program of $2,000 for the next 5 years. The company has 1,500 shares outstanding in year 1.

Below is two different scenarios. In the first scenario on the left, which is the favored scenario, the stock price basically stays flat at $15 and the earnings grow 20% between year 1 and 5. By the end of the 5th year 133 shares would have been repurchased, your ownership would have grown from 2.3% to 2.6% and your claim on the earnings would have grown from $30 to $40. An increase of almost 32%

In the second scenario on the right the stock price becomes overvalued due to irrational market behavior. The stock price rises 50%, the earnings would only grow about 10%, your gain in ownership would only grow from 2.3% to 2.48% while your claim on the earnings would only grow to $35.47, and increase of 17%.

The obvious difficulty is the suffering of holding an investment for 5 years while the stock stays flat. This is basically a superhuman strength that most people simply don’t have. But if you are committed to a stock and truly believe the business will ultimately prevail then the rewards could pay off.

I disagree with buffet that repurchases should only be done at the most opportune times. They should certainly be done at the most opportune times, and shouldn’t be done when stock is overvalued, but there are plenty of companies that have taken a slightly more systematic approach. They have repurchased shares in a more mechanical and predictable way, which is probably more justified anyways because they usually trade at lower valuations. Companies like AZO 0.00%↑ , LOW 0.00%↑ and NVR 0.00%↑ are a prime examples of this.

These types of companies are what Monish Pabrai would call “uber cannibals” because they consistently repurchase their own shares outstanding. They may do it more aggressively when the market dips and less when the market is up, but nevertheless they buyback shares every year because it’s the number one way they return capital to share holders. These companies have rightfully determined that buybacks are the most efficient and effective way to return cash to shareholders and they do it consistently.

Hypothetical 10 year buyback returns

Ok moving on the the meat and potatoes of the this article.

I want to discuss a hypothetical scenario where we pay a reasonable price for a stock in year 1 and by year 10 the company had grown earnings, repurchased shares and expanded its multiple all at a modest pace. I don’t want this to be an example of a company you’ll never come across but one that you could potentially find.

Lets assume a company is growing earnings at 10% a year and repurchasing 3% of its shares outstanding each year

The company would have compounded EPS at a rate of just over 13%. Now, imagine you bought $1,000 worth of stock in year 1 at three different P/E multiples, 15x,18x, and 20x and by year 10 the multiple would have expanded to 25x

The results would be as follows

So in the worst case scenario presented here, you would get a 16% annualized return from this company if you entered your investment at a P/E multiple of 20x and exited at 25x. This of course doesn’t account for dividends which I may have to do a separate article on.

16% over a long period of time is a great rate of return, don’t let any one tell you otherwise. All of us obviously want more, we all want to find the next Amazon or Netflix and I sincerely hope you do but you don’t need that to produce good returns over time.

Risks

There are a few scenarios to watch out for that could deter you from investing in a company that is engaged in a buyback strategy.

Too much leverage

Modest leverage can be used to boost returns and increase buybacks. This is often a preferred strategy compared to paying dividends because interest expenses are often tax deductible whereas paying a dividend is taxed twice, once at the corporate level and once at the shareholder level.

The problem is when a company begins taking on large amounts of debt in order to buy back large amounts of shares assuming they will always be able to generate sufficient cash flow to cover the interest expense. This can be especially risky in cyclical industries.

Over paying

This one is fairly simple, just like when you or I pay too much for an investment, a corporation can overpay and destroy shareholder value. Investing money in one thing when there is simply a better opportunity elsewhere is a big risk, and every time a company over pays for their shares, there is a better opportunity elsewhere.

Insider greed

Some times management likes to enrich themselves with buybacks. Some red flags could be large repurchases and huge insider ownership and or insiders who have the bulk of their compensation paid in stock options. Obviously if their compensation is connected to increasing EPS they can artificially boost the EPS and get a huge payout. Often times these companies are struggling because management is milking the company for their own benefit rather than growing it for the benefit of shareholders.

In summary

Buybacks are very important if there aren’t more useful ways to use capital

Buybacks can lift EPS and increase ROE,ROA and ROIC metrics, but they can also slow the growth of book value per share and deflate equity.

The price is important when repurchasing shares because it ultimately affects how much increased ownership you get.

A proper capital allocation strategy can produce high returns for shareholders even if earnings aren’t in hyper growth.

Hope you enjoyed thanks for reading!