Why I bought FTAI Aviation

Why I took a position

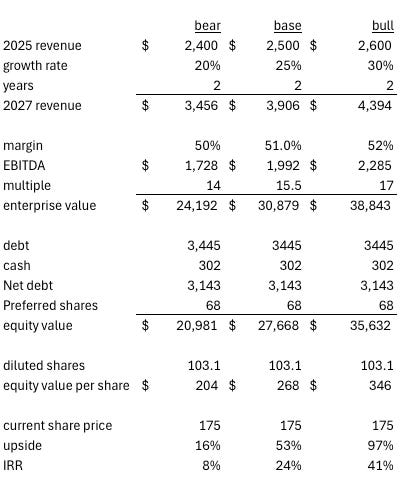

Key information

Ticker: FTAI 0.00%↑

Share price: $175

Investment type: Growth at reasonable price

EV/EBITDA: 16x

Estimated 2 year upside: 16% - 97%

I recently took a 5% position in FTAI Aviation. Admittedly, I am late to the party on this one, and some people may be wondering why I bought near all-time highs. It’s certainly true that this company has already inflected, and much of the multiple re-rate has already occurred as the narrative around the company has changed over the last few years.

However, FTAI still has a handful of growth levers and catalysts that may not be fully considered by the market. And the Muddy Waters short report released in January has cast skepticism on the story. I will cover the short report briefly near the end.

FTAI overview

At first blush, FTAI can be a bit difficult to understand, and this is partly because there isn’t another similar public company to compare it to. It’s very niche, and the way management has evolved the business is unique.

The company has undergone a transformation over the last few years, which includes a spin-off from its infrastructure business and aggressive expansion in its aircraft maintenance and repair business (MRO). FTAI Aviation FTAI 0.00%↑ separated from FTAI Infrastructure FIP 0.00%↑ in a spin-off in 2022. Prior to the spin-off, the company was an industrial conglomerate of sorts, a collection of energy terminals and other infrastructure/transportation assets, along with an aviation leasing business.

Today, FTAI Aviation has two segments, Aerospace Products and Leasing. Aerospace Products is an engine maintenance business and leasing is an aircraft and engine leasing business. So, airlines can essentially come to FTAI and both lease a plane and also have the maintenance and engine module swaps done in a very cost-effective manner. Aerospace Products is the bulk of the thesis and I will be focused on this fast growing segment in this article.

The easiest way to think about FTAI is as an outsourced engine maintenance business for the two most widely used commercial jet engines in the world, the CFM56 and the V2500. FTAI buys end-of-life engines and rebuilds/repairs them at their service facilities, and then either sells, exchanges, or leases them. Fundamentally, this is a spread business, where money is earned on the difference between acquiring/ repairing and selling/leasing engines.

The company is able to extract value from older engines and repurpose them to maximize their life and profitability. Through its partnership with Chromalloy, a parts manufacturer, FTAI is also able to acquire critical parts for repairs at cost, plus earn a portion of profits on parts sold to third parties.

The big differentiator between FTAI and competitors is that FTAI owns the engines they work on (600+ engines), which forces them to think like an owner who is incentivized to be as efficient as possible in repairing and extracting value out of the engines. This is contrasted with an traditional MRO shop which is incentivized to work slowly, add work and run up an invoice. Unlike other MRO specialists, FTAI is primarily in the business of exchanging engine modules and engines rather than traditional ‘diagnose and repair’ maintenance. I’ll explain this more in a bit.

The company has also begun a series of strategic initiatives that allow FTAI to build a leasing fleet off-balance sheet, which have been exclusively serviced by FTAI’s modules facilities.

All of this amounts to a vertically integrated aircraft maintenance, repair, and exchange (MRE) business that is able to take a lot of cost out of the engine maintenance and repair process.

PMA Chromalloy partnership

FTAI formed an exclusive perpetual partnership with Chromalloy in 2018. As art of that deal, FTAI is given access to 5 engine parts that Chromalloy will manufacture via PMA upon regulatory approval.

FTAI benefits in two ways;

FTAI gets a portion of the Chromalloy’s profits on parts sold.

FTAI gets 5 hot-section parts for their own MRO business at cost (up to 75% discount to OEM). Two parts have already been approved by the FAA; high-pressure turbines and low-pressure turbines. Three additional parts are currently awaiting approval and could be approved soon.

For those who aren’t familiar, PMA parts are regulated aftermarket parts that must be approved by the FAA. They are the aircraft equivalent of generic drugs. They don’t carry the brand name of the OEM and but they are typically more readily available and much cheaper, and sometimes better quality than the OEM equivalent.

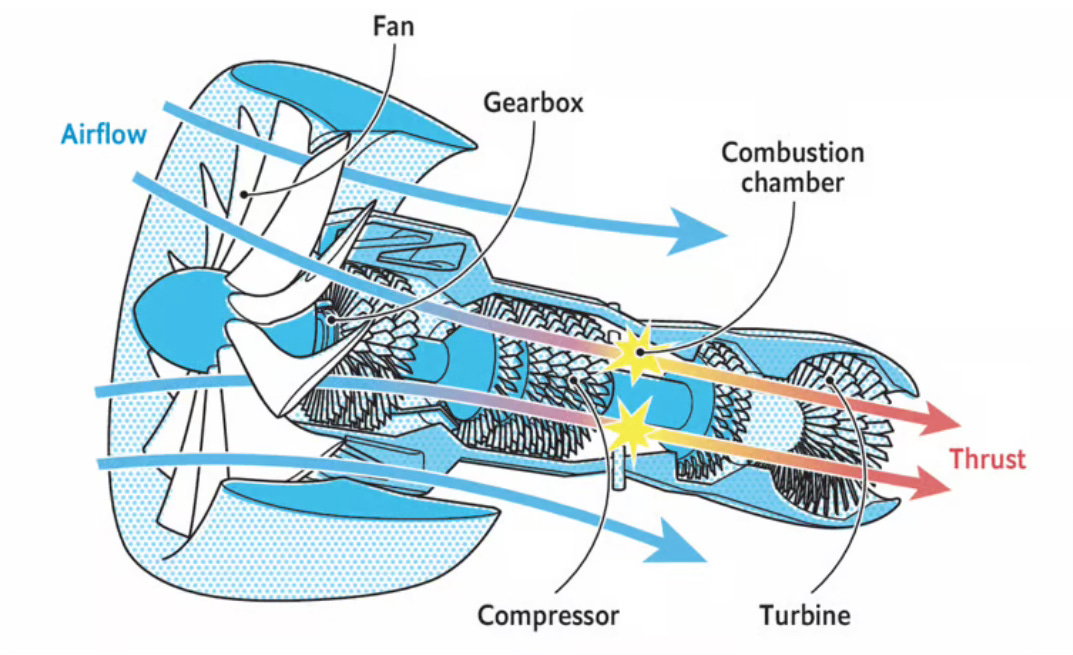

A jet propulsion primer

The basic operation of a jet engine is similar to any combustion engine. It consists of intake, compression, fuel injection, combustion, exhaust. The engine parts that are situated after the combustion chamber are considered the hot-section parts because they are exposed to extreme thermal stress. One part in particular, the High-Pressure Turbine (HPT), is both the most expensive and the fastest wearing component in this section due to its position nearest the combustion chamber and the mechanical stress exerted on it. A new set of HPT blades and vanes can cost up to a few million dollars and they wear out fairly often.

FTAI is given access to high pressure turbines (HPT) at cost, along with low pressure turbines (LPT). Chromalloy is uniquely focused on hot-section parts and the partnership allows FTAI to remove an incredible amount of cost from their rebuilds and repairs, making its profitability difficult to replicate. Given that FTAI is in the business of buying and repairing old engines and then selling them, the ability to get key hot-section parts at cost is quite the advantage, especially when others would have a lot of trouble doing the same.

FTAI will be able to save $2 million per shop visit with all five PMA parts across the engine approved. Not only is this an incredible deal for FTAI, but it's also a great deal for customers as they receive some of the cost benefit as well.

MRE

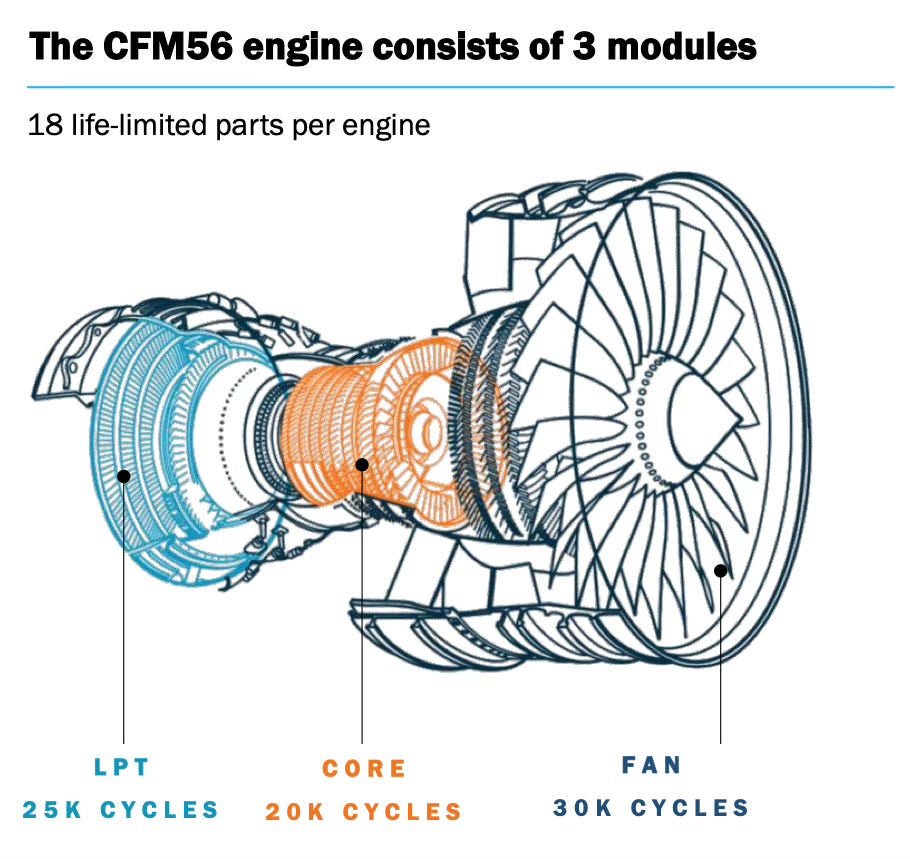

FTAI has exploited the modular design of the CFM56 and V2500 and created a maintince, repair and module exchange (MRE) business. The CFM56 in particular is widely regarded as the easiest engine to work on with its simple design. The anatomy of the CFM56 consists of the fan module, the core module, and the low-pressure turbine module.

Zero waste philosophy

Because FTAI owns 600+ engines and has maintenance capabilities, the company is able extract the maximum amount of life out of each engine. Zero waste is the policy at FTAI, and they have some optionality with how to achieve this. Engine modules can be pulled apart and paired with other modules with similar cycles remaining in order to maximize their life and value. These engines can then be leased, sold or exchanged for more than they would if they hadn’t been optimized. If engines or modules need to be rebuilt or repaired, FTAI has access to hot-section parts at a steep discount to OEM. Depending on the customers needs, FTAI may swap a single module or exchange an entire engine if all modules need to be replaced. Additionally, for modules or parts that FTAI does not use for its own engine builds, they are sold through a partnership with AAR, which provides a distribution network for a fee. Scrap engine parts are also recycled.

In Q4, the company did a demonstration with three unserviceable engines with varying cycles remaining. Engine modules were pulled apart and paired with others with similar life left. FTAI was able to take three unserviceable engines and make two serviceable ones and the remaining unserviceable engine was sold for $1.5 million. The total value created was $16 million on a $10 million capital outlay which includes engines + MRO work.

This ability to optimize “green-time” contributes greatly to Aerospace Products EBITDA margin, which is around 35%—well above the typical MRO shop profile around 15%. Management believes there is further margin to be had when the remaining 3 hot-section parts are approved, potentially pushing EBIDTA margin closer to 50%. The company also acquired Pacific Aerodynamic which focuses on highly specialized precision repairs of CFM56 compressor blades and vanes and is expected to contribute 1-2% in margin.

CFM56, V2500

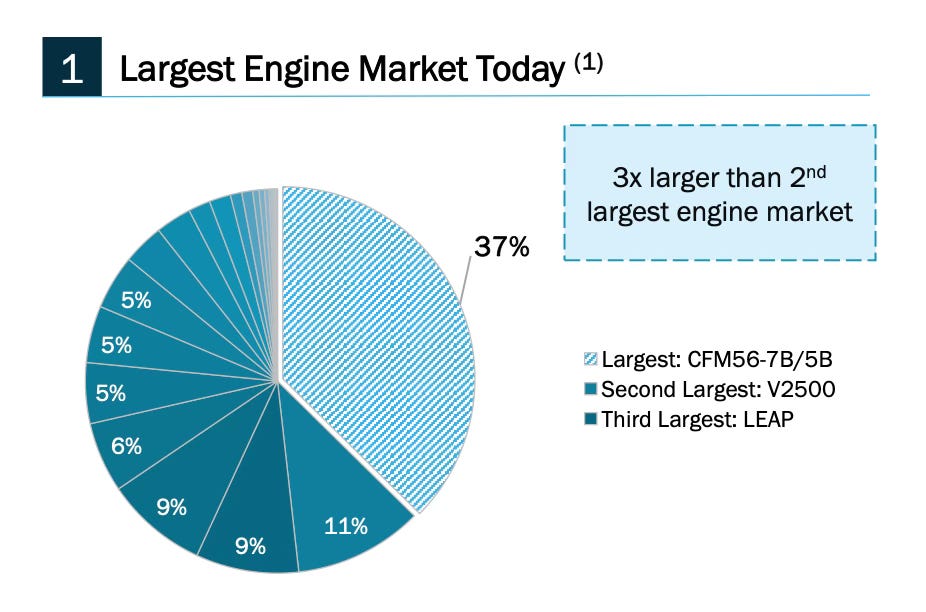

CFM56 engine is expected to remain as a dominant platform for another 25 years, and there are 21,00 engines still in operation, implying a long runway for FTAI. The CFM platform is about 47% of narrowbody jets, followed by the V2500 at 14%, which is the other engine FTAI provides care for. Collectively they account for 60% of narrow body jets worldwide. The graph below is from 2023.

Mod Shops

Shop visits are the single most expensive part of owning or leasing an engine, and they tend to be a big burden on airlines who already have razor thin margins to begin with. A new CFM56-7B engine in standard configuration (without extras or large discounts) is likely in the $12-20 million range, depending on variant and terms. The unfortunate part about owning an engine is that a few shop visits could cost the same amount as the engine cost. Thus, it’s easy to understand why FTAI would go all in on a maintenance solution that is more cost effective as this is a big value proposition for airlines and owners.

FTAI Acquired 3 maintenance and testing facilities that have the physical capacity to do 1,800 annual module shop visits. The company’s current capacity is around 600, with a goal of achieving 750 in 2025, 1,000 in 2026, and then expanding from there.

As I stated in the beginning, the key to understanding FTAI is to understand that it owns the engines, the maintenance shops, and the manufacturing, which uniquely positions it to rebuild/repair the engines in an efficient manner at a very low cost. Technicians are primarily rebuilding and repairing engines that FTAI owns and doing so in an assembly factory manner. When an airline comes in, FTAI offers a lower fixed price, less downtime and modules that are ready when needed. This is in contrast to the traditional model where a plane comes in for service and pays for a detailed diagnosis and repair, which often come with cost-overruns and unpredictable service times. According to management, traditional shop visit can be anywhere from 3-6 months depending on the severity and slot availability, FTAI’s module visits can be as short as 1-4 weeks.

The model appears to be working because FTAI is rapidly taking market share—growing from 0% - 9% market share in just 4 years, with a goal of taking 25% of the market. The total opportunity is $22 billion, implying $5.5 billion in revenue for the aerospace products segment, if management can pull it off.

FTAI’s MRE business is on track to do around $600 million in EBITDA in 2025, if they reach their goal of 750 module exchanges, this implies around $800k in EBITDA per shop visit. This factors in savings from 2 hot-section parts acquired at cost. Considering there are still 3 more parts awaiting approval, it's not hard to imagine a scenario where FTAI can do over $1 million in EBITDA per visit in the near future when PMA parts are approved.

Strategic capital initiative (SCI)

The strategic capital initiative (SCI) is the first of a series of growth initiatives. The idea was the logical conclusion of two key things.

Management wanted to grow in an asset-light manner.

FTAI was already providing significant value to its leasing customers and benefiting from it.

So, FTAI formed a capital vehicle with a fund‐style setup, which FTAI manages as a general partner with 20% ownership. This fund is the first of a series. The basic idea is that FTAI will create these partnerships with third-party capital to acquire aircraft off balance sheet. The fund then owns/leases the aircraft, and the engines are maintained exclusively through FTAI’s MRE business. So, FTAI gets a future stream of revenue from maintenance, but it also receives a fund management fee, and control over a portfolio of aircraft off balance sheet. This deal reflects a recurring theme with FTAI, they form exclusive partnerships with third parties that benefit the MRE business, while also providing an additional stream of income through a fee or cut of profits.

For 2025, the goal is to deploy $4 billion and acquire 250 aircraft. $2.5 billion in debt financing is already secured from Apollo and Deutsche Bank and $240 million in equity financing has been committed from FTAI. Management is targeting final closing in Q4 2025, and is announcing a second partnership (SCI 2) next year. Management also believes that after doing a new partnership each year they can ultimately get to $20 billion in assets under management and become the world’s largest owner of narrow-body aircraft.

Management

In 1998, Fortress Investment Group was founded in as a private-equity / alternative asset manager. FTAI’s current CEO, Joseph P. Adams, Jr, and the entire management team, were heavily involved within Fortress’s Private Equity group. Adams’ management behavior is almost certainly shaped by his Fortress PE lineage. He was able to take a somewhat boring infrastructure business and make a vertically integrated aviation platform with a strategic sourcing partnership and an intelligent side-car investment vehicle (SCI).

Adams holds 478,308 shares of FTAI 0.00%↑ worth $81 million, which is 81x his base salary of around $1 million. This certainly counts as shareholder alignment. Adams also has short term incentives (cash bonus) tied to Adjusted EBITDA and long term equity incentives tied to total shareholder return and diluted adjusted EPS.

Muddy waters short report

The short report is almost considered old news by now as it came out in January. It has already been refuted on X and defended by several Wall Street firms, including Citi, Deutsche Bank, and Barclays, which called the claims “largely baseless and unsubstantiated”. The company also did an internal audit and found no merit to the claims.

The basic argument is that FTAI is a glorified leasing business that manipulates its financials. One part I did find interesting and would like to briefly talk about is the over-depreciation claim.

Over-depreciation scheme

One of the big claims made by Muddy Waters is that FTAI allegedly inflates gross margins by transferring assets between segments and over-depreciating its assets.

The argument is that FTAI has an aggressive depreciation policy which allows FTAI to depreciate engines rapidly as leasing assets, then transfer them to Aerospace Products inventory for teardown or resale, where they realize a lower COGS and result in a higher gross margin. Muddy Waters has even gone so far as to say that management temporarily transfers engines from Aerospace Products to Leasing for a few months, then back to AP when they want to fluff the numbers.

In my view, the short report simply cannot prove misclassification when transfers actually do occur. FTAI is intentional about classifying assets and cash flows correctly and assets are only transferred when there is a legitimate change-in-use. Asset transfers are a result of FTAI’s integrated model where some leased engines eventually get retired, torn down, and sold, or leasing assets are being rebuilt and require parts from Aerospace Products. Management has also stated that they only depreciate leasing assets that are being leased. 1

Manipulating book values would require changes in depreciation lives or residual assumptions, which do not appear in the filings. FTAI’s fundamental depreciation policy for core aviation assets remained consistent with the standards established pre-2021, when Aerospace Products did not exist.

There could be some small margin benefit from transfers at times, but they flow from GAAP principals that are required in hybrid leasing-manufacturing operation, rather than some elaborate scheme.

Risks

There are a few keys risks besides the standard macroeconomic risks that are inherent in most companies.

Airplane lessors (FTAI’s customers) are highly leveraged and while they usually manage their debt well, it’s possible the default and cause problems for FTAI.

If FTAI is not able to secure SCI funding or agree with partners on the assets being acquired it could create problems and disrupt the flow of future MRE shop visits.

FTAI depends on other partnerships in order to keep their operation growing and running smoothly, if one of these moving parts should stop moving, it could spell trouble for the business.

Financials and Valuation

Total revenue has grown at a three year CAGR of 70%. This has undoubtedly been driven by Aerospace Products and the Contractual MRE segment growth. Contractual MRE is the revenue derived from the SCI partnership, Aerospace products is everything else connected to the maintenance and repair business. Together, these will contribute an estimated $1.7 billion in revenue in 2025 (72% of revenue) which is up from $1 billion in the prior year.

I expect revenue to come in at around $2.5 billion in 2025, implying 44% revenue growth. EBITDA in 2024 was depressed due to a restructuring fee paid to FTAI’s former manager Fortress, however trailing twelve months EBIDTA has grown significantly and sits around $1.1 billion. Although total revenue is growing rapidly, I expect it to moderate over the coming years to 20% - 30%.

Returns on capital will likely increase as the MRE business takes a larger share of revenue mix and requires much lower CapEx than the leasing business. FTAI has modest leverage with leverage ratio is 2.2x indicating fairly low leverage risk.

Going forward, I would expect EBITDA margins to expand from PMA part approvals. The next hot-section part, which supposedly is coming this year (possibly October), is one of the more significant parts. According to management, 80% of cost take-out will come from the first three PMA parts, which means that a good portion of it is already gone but this third part will still contribute to margin uplift in a meaningful way.

Here are my assumptions for the model

Revenue growth of 20% - 30% through to 2027, reflects a moderation but continued growth in Aerospace Parts.

Slight margin expansion in bull case, bear and bull represent similar margin. Im not betting on big margin improvements from PMA over the next two year because PMA approvals are not in FTAI’s control.

EBITDA multiple of 14x - 17x. It currently sits at around 16x, or 14.5x on a forward basis. It should be noted that the market doesn’t seem to know exactly how to value this company. It could be valued as either a leasing, MRO, or parts manufacturer, with the latter having an EBITDA multiple well above 20x and the former two being 10x - 15x. I personally think FTAI can be a 15x - 20x company if it can execute on its SCI and PMA’s are approved.

Diluted shares count remains.

Final thoughts

I really like this business, and it seems promising if SCI and PMA are successful. However, I do have some concerns about the complexity of the business and the many moving parts required to keep this business running smoothly. As such, I’ll continue to study this company I could grow more confident and increase my position beyond a 5-6% position. If the stock should fall significantly in a market sell-off I would likely add.

Feel free to leave a comment if you think I am missing something.

That’s it for this week thank you for reading.

Disclaimer: I am not a financial advisor. Nothing I say should be taken as financial advice. Some investments I discuss are very risky, so please do your own research and consult a financial advisor before buying or selling any securities.

Full disclosure: I am an FTAI 0.00%↑ shareholder at the time this was written.

https://www.tipranks.com/news/stay-long-and-strong-says-analyst-about-ftai-aviation-stock?utm_source=chatgpt.com

Thank you!!!

My largest holding. Think it will be a market outperformer for many years to come… best of luck.